Rebound Critics Misfire

A Response to Danny Cullenward and Jonathan Koomey

-

-

Share

-

Share via Twitter -

Share via Facebook -

Share via Email

-

In a recent duo of blog posts energy economists Danny Cullenward and Jonathan Koomey broadly challenge the notion that so-called rebound effects are likely substantial and should be dealt with as such. The basis for their claim is their recently published peer-reviewed article, which challenges my 2013 analysis finding consistently large long-term rebound effects across 30 sectors of the US economy between 1980 and 2000.

Cullenwald and Koomey argue that due to fundamental issues in the dataset used there, the large rebound magnitudes reported by Saunders are “wholly without support” and from this, suggest that a 2011 survey of the rebound literature by The Breakthrough Institute, in which my research was first referenced, should not be taken seriously.

Before addressing the specific criticisms of my 2013 analysis, it is important to note that Cullenwald and Koomey greatly exaggerate the importance of my analysis. The Breakthrough Institute review cited over 100 peer-reviewed articles which all pointed to rebound magnitudes significantly larger than that which most energy efficiency advocates have been willing to acknowledge. A range of further literature reviews, conducted by groups ranging from the International Energy Agency, the Intergovernmental Panel on Climate Change, the European Commission, and the United Kingdom Energy Research Center have conducted similar reviews reaching similar conclusions.

Notably, Cullenward and Koomey do not actually demonstrate that the issues they find with the dataset I used significantly affect the reported rebound magnitudes in my paper. Their only claim is that, were these data issues somehow corrected, the reported magnitudes would likely be different, and indeed they are agnostic as to whether rebounds would be systematically larger or smaller, let alone by what magnitude.

Absent any analysis suggesting that the problems they have identified systematically overstate rebound magnitudes in my analysis, Cullenwald and Koomey simply complain that they raised concerns about problems with my data set at a Carnegie Mellon workshop in 2011. This is indeed the case. I subsequently published my analysis, and it passed peer-reviewed muster, because, as I will demonstrate below, there is no evidence that those concerns are particularly material to the conclusions of my analysis.

Theory Misapplied

To their credit, Cullenward and Koomey take a deep dive into the dataset (which was developed by Harvard professor Dale Jorgenson) and methods used in my 2013 analysis. Regrettably, they misunderstand them. While the theory-based objections that Cullenwald and Koomey raise against my analysis – and to the underlying Jorgenson et al. dataset and analyses – might appear to rest on sound microeconomic principles, they turn out to rest on the wrong microeconomic principles.

At bottom, Cullenwald and Koomey’s criticism rests upon the supposition that because regional differences in absolute levels of energy prices vary substantially, national averages in those prices cannot be used to accurately estimate rebound. Energy prices in, let’s say, Texas are different from energy prices in California, and hence, national average prices cannot be used to estimate how individual firms will respond to changes in prices.

This problem may appear to be of serious concern intuitively but is actually of minor consequence analytically. What Cullenward and Koomey misapprehend in their critique is that the rebound magnitudes reported in Saunders – and the energy and other economic forecasts put forward by Jorgenson et al. – all rely at their foundation on measurements of so-called substitution elasticities, which in turn depend for their measurement on observed changes in input prices. What matters to rebound estimates is not the absolute level of energy prices in any given locality but the variation in those levels across the time series.

The physical intuition for why variations rather than absolute magnitudes dominate in measuring rebound magnitudes is this: a producer contemplating changing her production technology in the face of an energy price increase will look to the incremental value of the energy quantity reductions to be had from deploying the technology – the difference in her profits at the new energy price were she to stick with today’s energy quantity compared to her profits at the new energy price when moving to the new quantity resulting from the different technology. “Do my profit gains from reduced energy use outweigh the cost of changing the technology?” will be her decision criterion. Her “substitution response” is then related to how much her energy quantity changes given the change in energy price. Notably, her behavior depends not on the absolute energy price, but on how much it changes over time. The same holds true for her competitors in other locations who may face somewhat higher or lower absolute energy prices.

The same dynamic works for energy efficiency gains in the absence of a price movement, but in reverse. Even with no change in energy price, it may make sense to invest in new energy efficiency technology that becomes available. But such a gain acts just like an energy price reduction, reducing the effective price of energy services (thereby invoking rebound in physical energy use). Again, there is a substitution response that depends not on the absolute price of energy, but the change in the effective price of energy.

While this shows that differences in absolute energy prices seen by producers matter little to the measurement of rebound, note also that the possible difference between average and marginal price that Cullenward and Koomey worry about is likewise of little or no consequence. In a microeconomic sense, it is true that producer decisions depend on marginal prices rather than average prices, and that marginal prices tend to be higher than average prices (though they can be lower), but – whether higher or lower – we have seen that the absolute price levels matter little: it is differences in the prices over time, whether average or marginal, that matter.

Empirical Evidence

To highlight the distinction elucidated above, we can look at regional differences in natural gas prices as reported by the EIA, shown below:

As can be seen, while commercial enterprises in different areas of the US paid different absolute prices for their natural gas supply, the price changes they experienced are highly comparable. Energy being a fungible commodity, energy prices generally are locked together across locales by the underlying movement of energy prices at reference locations, so changes are likewise linked.

Technically, the role of energy prices in measuring rebound magnitudes is somewhat subtler than this intuitive picture. The econometric measurement relies on four equations whose form indicates that what matters to the econometric measurement is variation over time in the natural logarithm of the energy price and, related to this, variation over time in the relative change in energy price. These are the proper comparisons to be made when asking whether regional differences in energy price might significantly affect rebound measurements.

Without regional Input-Output data, one cannot run this kind of rebound analysis regionally. But we can look at variations in the natural logarithm of regional gas prices to ascertain whether those changes are likely to significantly alter rebound estimates based on national averages. To illustrate, we can create a historical plot of the natural logarithm of the national average commercial natural gas price vs. the natural logarithm of the California commercial gas price, using EIA data (available for the years 1967-2014):

As seen, over 48 years there has been an extremely tight correlation between (the log of) the national average price of natural gas delivered to commercial customers and (the log of) the gas price delivered to California commercial customers. What matters to econometric measurement is the variation. Variations in one translate directly into variations in the other. The correlation is 0.98 – one rarely encounters an R-squared coefficient this high. This dynamic applies to the first three econometric equations referenced above, which carry the greatest weight in the analysis.

The fourth econometric equation fits variations in relative (percentage) price changes over the horizon of the data series. The relevant plot is shown below:

Again, annual relative (percentage) price changes for California are highly correlated with national averages, and the deviations appear to show little consistent bias. Furthermore, when analyzed across several states (two reported in this post), the errors are not systematically biased one way or the other.

Importantly, the deviations that matter to the econometric analysis are small in percentage terms – a very far cry from the large absolute magnitude deviations (hundreds of percentages) Cullenward and Koomey would have us believe discredit the econometric measurements.

To be complete about it, account must be taken of the other energy sources beyond natural gas. And while it would be sufficient to undercut the Cullenward/Koomey claims to establish that regional price differences in one state make little difference in measuring rebound (if rebound magnitudes in California are as estimated in Saunders using national averages, such rebound magnitudes become generally credible), we add Texas for comparison. The table below shows the relative energy use by fuel type and sector for the two states (the electric power sector is excluded, so coal is not included).

Table 1. Fuel use by fuel type

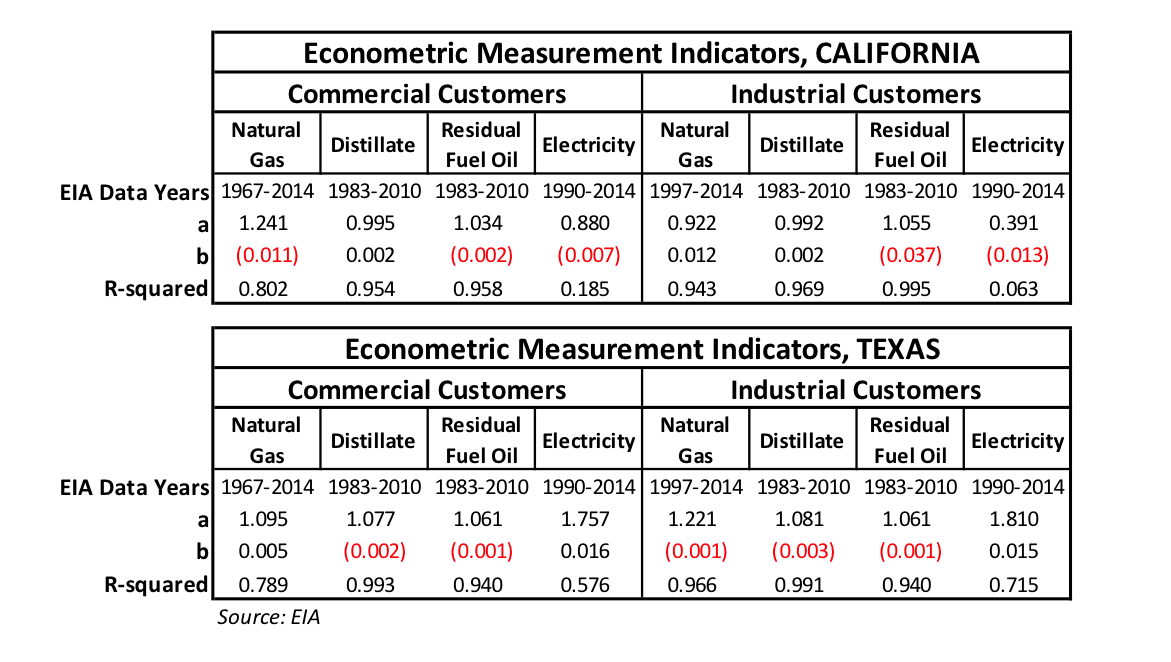

With this in mind, we can summarize the true impact of regional energy price differences on the econometric measurements of rebound magnitudes in Saunders (where a and b are the coefficients in the regression equation state price = a*ln(national average price) + b):

Table 2. Econometric indicators for the log(price) equations

For California, the coefficient “a” of the log(price) equations is very close to unity across all fuel types for Commercial customers, and across all fuel types for Industrial customers with the exception of electricity. This means variations in California prices track very closely variations in national average prices over the domain of the national data, certainly not enough to substantially affect an econometric measurement. The fit is tight, with high correlation coefficients. We see small variations in the “b” parameter showing no systematic bias. Texas prices likewise trend closely with the national average.

While it is true that electricity prices for the industrial sectors are not so closely aligned with national averages, from the previous table it is apparent that electricity forms a small portion of industrial energy use (less than 20% for both states), meaning its impact is significantly attenuated.

Table 3 below reports comparable results relating to the fourth econometric equation (where a and b are the coefficients in the regression equation state relative price variation = a*ln(national relative price variation) + b):.

Table 3. Econometric indicators for the relative price equation

Again, we see close correlations between national and regional relative price changes over long periods and large variations in magnitude, with the exception of electricity. But this applies to only one of the four econometric equations (and so carries less weight in the measurement) and again industrial electricity consumption in both California and Texas was less than 20% of consumption.

From these results it is evident that national and regional energy price dynamics that matter to the econometric measurement of rebound are in close alignment. Commercial customers in both California and Texas experienced energy price dynamics remarkably similar to that of national average energy prices. Likewise, industrial customers in both states experienced energy price dynamics remarkably similar to that of national average energy prices. And what differences remain are a huge departure from the large absolute energy price differences Cullenward and Koomey claim as determinative in their critique.

It takes some experience running hundreds of econometric analyses to develop a sense of what matters and what does not (experience neither Cullenward nor Koomey can claim). That, and the above analysis tell this analyst that regional differences in absolute energy price levels are of little consequence, when analyzed correctly with empirical evidence, and such differences in no way undermine the estimates of rebound magnitudes in my 2013 analysis.

Broader Implications

The logic used by Cullenwald and Koomey, were it valid, would invalidate much more than my 2013 analysis of rebound magnitudes in production sectors of the US economy. The models relied on by the IPCC to forecast future energy use (and associated emissions) suffer from the same ostensible shortcomings alleged by Cullenward and Koomey to afflict my rebound analysis, but in far greater measure. That is, these global models aggregate energy efficiency dynamics not only at sectoral levels (a few) as with Saunders, but at national, regional and ultimately, global levels. Models used in the latest IPCC report are not reported to be calibrated with econometric measurement but rather assume values for key parameters (such as the central-to-energy forecasting substitution elasticities); and to the extent the models are otherwise calibrated to approximate observed data, these are data aggregated to a high level – in other words, national, regional and sometimes global averages.

The logic offered by Cullenward and Koomey then leads to the necessary conclusion that these analyses are “wholly without support.” In other words, in such a world one cannot claim finding a pathway toward a 2oC world constitutes an urgent task, since we can draw from these models no trustworthy conclusion about the future path of energy use globally. In this light, how can Cullenward and Koomey even know the task is urgent?

Rebound, of course, makes the situation even more urgent than depicted in their scenarios of projected energy use. As shown elsewhere, a review of 25 models designed to inform climate change mitigation policy, including those relied on by the IPCC, reveals methodological limitations among virtually all of them preventing proper accounting for rebound effects and delivering systematic understatements of their magnitude. The presence of large rebound effects means we have less time than is commonly believed to devise climate change mitigation solutions – less time than one would infer from IPCC forecasts.

Rebound means greater urgency, not less. Provided, of course, one does not follow the line of reasoning explicit in the Cullenward and Koomey critique, which would provide ample reason to reject the IPCC forecasts altogether.

Conclusions

In many ways, the Cullenward/Koomey critique of the Saunders article is reassuring. They have plainly taken a deep look at the analysis and, finding no methodological issues to criticize, were reduced to challenging the Jorgenson et al. dataset used in the rebound analysis. But we see that their critique dissolves under careful examination owing to their misapplication of microeconomic theory to the data in question. One can only feel gratitude in knowing that the Saunders analysis is robust enough to weather such a determined assault on its findings.

It has been known for over 20 years that rebound effects are welfare-enhancing. The greater the flexibility of the productive economy to respond to energy price movements and new energy efficiency technologies, the greater will be this economic welfare gain – and rebound.

Perhaps the time has finally come to, rather than devote concerted effort to finding supposed flaws in studies showing large rebound effects, instead face the issue squarely and direct effort to finding ways to take advantage of rebound’s welfare-enhancing aspects while limiting its impact on energy savings. Researchers such as Karen Turner at the University of Glasgow are leading the way in this.

My 2013 analysis is not perfect, as indicated by what Steve Sorrell points out are “3 pages devoted to listing 'cautions and limitations'” offered in that article. The Cullenward/Koomey critique can be added as an item to that list, but it does not rise to the level of being anything resembling a fatal flaw.

Much work remains to be done to measure rebound magnitudes on the productive side of the economy. Far too little attention has been paid this topic, which is puzzling as the vast majority of energy is consumed in this sector globally. Along the way, it would undoubtedly be useful to upgrade the models used by the IPCC and other organizations to properly account for rebound and so enhance the credibility of global energy use forecasts relied on by policy makers.

References

Cullenward/Koomey posts: http://www.koomey.com/post/136611184100; http://www.koomey.com/post/137309412653

Cullenward/Koomey article: http://www.sciencedirect.com/science/article/pii/S0040162515002541

H.D. Saunders, “Recent Evidence for Large Rebound: Elucidating the Drivers and their Implications for Climate Change Models,” The Energy Journal, 36(1), 2015.

H.D. Saunders, “The Khazzoom-Brookes Postulate and Neoclassical Growth,” The Energy Journal, 13(4), 1992.

H.D. Saunders, “A View from the Macro Side: Rebound, Backfire and Khazzoom-Brookes,” Energy Policy, 28(6-7), 2000.