Confronting the Solar Manufacturing Industry's Human Rights Problem

New report, "Sins of a Solar Empire," calls for solar industry to address unethical solar photovoltaic manufacturing in Xinjiang.

-

-

Share

-

Share via Twitter -

Share via Facebook -

Share via Email

-

Executive Summary

Over the past decade, much of the global silicon-based solar photovoltaic industry has slipped slowly into the path of a major human rights crisis. International actors have generally overlooked early warning signs of Chinese government oppression in the Xinjiang Uyghur Autonomous Region (XUAR; 新疆维吾尔自治区) while concentrating investment and business partnerships into solar manufacturing supply chains linked to the region. Now, extensive evidence of government-organized forced labor programs and numerous other crimes against humanity in the XUAR has come to light,United Nations, Human Rights Council, Contemporary Forms of Slavery Affecting Persons Belonging to Ethnic, Religious and Linguistic Minority Communities, Report of the Special Rapporteur on Contemporary Forms of Slavery, Including Its Causes and Consequences, July 19, 2022, https://undocs.org/Home/Mobile?FinalSymbol=A%2FHRC%2F51%2F26&Language=E&DeviceType=Desktop&LangRequested=False.United Nations, Office of the High Commissioner, Human Rights, OHCHR Assessment of Human Rights Concerns in the Xinjiang Uyghur Autonomous Region, People’s Republic of China, August 31, 2022, https://www.ohchr.org/sites/default/files/documents/countries/2022-08-31/22-08-31-final-assesment.pdf. yet downstream solar photovoltaic companies remain hesitant to quickly and fully distance themselves from low-cost suppliers with operations in the region.

In addition to major advantages such as its modularity and near-zero variable and operating costs, much of the promise of clean solar energy stems from its affordability. The future of solar photovoltaic (PV) power looks bright precisely because it has attained stunning cost improvements over a relatively short period of time. To be clear, the lion’s share of this progress has occurred thanks to legitimate technological advances and innovation in manufacturing. Chinese firms invested heavily in large, modern factories that have achieved high efficiencies of scale, aided by substantial regional then national government support in the form of direct subsidies, cheap land, and subsidized, affordable electricity.

But solar manufacturing plants that began operating in Xinjiang over a decade ago were attracted to industrial parks and coal mines established under regional political oppression that left Uyghur, Kazakh, and Kyrgyz peoples uniquely powerless—even by the political standards of authoritarian China—to object to local environmental and socioeconomic impacts. And in subsequent years, as regional authorities have intensified repressive policies targeting minoritized peoples, solar PV manufacturers have continued to expand in the region while directly participating in state-sponsored forced labor programs.

The Xinjiang region produces a significant quantity of some solar PV commodities, particularly solar-grade polysilicon. As such, the availability and price of solar PV products are currently quite sensitive to the region’s manufacturing output, elevating the risk that efforts to truly divest the solar industry from dependence on Xinjiang could disrupt solar supply chains, at least until new, ethical production capacity is established elsewhere.

However, tackling this hurdle head-on is exactly the right choice for promoting a better, more innovative, and more socially responsible future for solar PV technology. An ethical and sustainable solar supply chain clearly cannot continue over the long term to rely upon current Xinjiang-dependent, coal-dependent manufacturing norms. Nor is this choice entirely up to solar industry actors alone. With the Uyghur Forced Labor Prevention Act having entered into effect in the United StatesH.R. 6256, 117th Congress (2021-2022), “To Ensure That Goods Made with Forced Labor in the Xinjiang Uyghur Autonomous Region of the People’s Republic of China Do Not Enter the United States Market, and for Other Purposes," December 23, 2021, http://www.congress.gov/bill/117th-congress/house-bill/6256. and with the European Union considering similar policies to prohibit imports produced using forced labor,European Parliament, “Forced Labour and the Situation of the Uyghurs in the Xinjiang Uyghur Autonomous Region,” adopted December 17, 2020, https://www.europarl.europa.eu/doceo/document/TA-9-2020-0375_EN.html. a failure to transition away from problematic solar equipment suppliers could hamper the industry’s development. Having underprepared for addressing supply chain concerns over much of the past decade, solar PV companies, renewable energy developers, and investors would be well advised to rectify that error starting today.

Downstream manufacturers, solar installers, and project developers should move aggressively and unambiguously to avoid solar PV suppliers with any industrial capacity in Xinjiang. Companies that source solar PV commodities from firms with Xinjiang operations should face broad pressure to adopt similar measures—or face market exclusion as well. Upstream investors, suppliers, and researchers should likewise move to terminate business relationships with Xinjiang-based manufacturers. To accelerate and facilitate this process of supply chain diversification and support the important solar PV sector, policymakers globally must enact major public sector initiatives to help establish new large-scale manufacturing capacity outside of China.

This shift requires a more stringent standard than current ethical sourcing guidelines,U.S. Customs and Border Protection, “Uyghur Forced Labor Prevention Act: U.S. Customs and Border Protection Operational Guidance for Importers,” July 13, 2022, https://www.cbp.gov/sites/default/files/assets/documents/2022-Jun/CBP_Guidance_for_Importers_for_UFLPA_13_June_2022.pdf. which have sought only to trace and exclude specific shipments of goods produced in the Xinjiang region.Solar Energy Industries Association, Solar Supply Chain Traceability Protocol 1.0: Industry Guidance, April 2021, https://www.seia.org/sites/default/files/2021-04/SEIA-Supply-Chain-Traceability-Protocol-v1.0-April2021.pdf. Tracing allows companies operating factories in Xinjiang to sell sanitized streams of “Xinjiang-free” solar PV products on global markets while continuing to benefit separately from Xinjiang-based production. Furthermore, such tracing and certification protocols will likely prove ineffective due to lack of corporate and government transparency in China including in Xinjiang.

But what if supply chain reorganization threatens solar power’s forward march and the speed of the global clean energy transition at large? This report explains how the current affordability of solar PV modules has historically resulted from technological advances, public-private investment, and industrial policy that can be replicated elsewhere. It is likely that enterprising companies with government support can establish new manufacturing pipelines outside of China at comparably low costs.

The door nevertheless remains open for Chinese firms and policymakers to address crimes against humanity in Xinjiang and assist in responsible solar PV sourcing by ending forced labor programs, restoring freedoms to persecuted minoritized groups, and adopting fair labor and environmental standards, among other necessary remedies and actions.

Responsible diversification of global solar PV manufacturing will benefit both the solar PV industry and the climate. Avoiding the reputational costs associated with companies operating in Xinjiang may well be worth a marginal and likely transient increase in the price of solar PV products. At the same time, alleviating the current overconcentration of the solar industry in China can help ensure a more stable and reliable supply of solar PV commodities, mitigating long-term risks to the solar industry in the event of supply chain disruptions. Alternative low-carbon solar PV manufacturing methods will also help displace the higher carbon and environmental costs of solar manufacturing inputs produced in Xinjiang, helping the solar PV industry improve its environmental record in a manner consistent with the spirit of long-term climate progress.

Ignoring the challenge at hand will only perpetuate the intertwining of solar supply chains with Chinese government repression, authoritarianism, and environmental injustice. At the same time, procrastination on supply chain reorganizations will suppress and postpone necessary evolutions in solar manufacturing that solar technologies need to truly—and justly—achieve global scale.

__________

Reviewers: Dustin Mulvaney, Lauri Myllyvirta, Yaqiu Wang, Maya Anthony, Gregory Nemet

Acknowledgments: Laura Murphy, Dustin Mulvaney, Nyrola Elimä, Lauri Myllyvirta, Adam Stein, Nathan Ruser, Alan Crawford

__________

The current global solar manufacturing landscape

It is common knowledge that Chinese manufacturers dominate international solar supply chains and that dependence on Chinese suppliers is currently projected to grow. Suffice it to say that Chinese firms operate the overwhelming majority of manufacturing capacity at each step in the solar manufacturing supply chain, from solar-grade polysilicon feedstock to polysilicon ingots and wafers to solar cells and solar PV modules (Figure 1). The market share of Chinese manufacturers is largest for the production of monocrystalline silicon ingots and the slicing of those ingots into wafers for use in solar cells, with companies in China possessing essentially all existing industrial capacity (>95%) for these processes globally.Paul Basore and David Feldman, Solar Photovoltaics: Supply Chain Deep Dive Assessment, U.S. Department of Energy, February 24, 2022,https://www.energy.gov/sites/default/files/2022-02/Solar%20Energy%20Supply%20Chain%20Report%20-%20Final.pdf.

These companies also possess significant advantages in expertise and technology, utilizing some of the world’s most cutting-edge equipment for solar cell manufacturing.

At the key initial upstream steps in the current solar supply chain, manufacturing capacity has become highly concentrated in the Xinjiang region. In particular, the XUAR contains significant quartzite rock mining, metallurgical-grade silicon smelting, and solar-grade polysilicon production. This latter step—solar-grade polysilicon manufacturing—is the solar supply chain’s most significant exposure to the Xinjiang region, with Chinese production based in Xinjiang operating a full 42% of global solar-grade polysilicon factory capacity in 2021.International Energy Agency, Solar PV Global Supply Chains: An IEA Special Report, July 2022, https://www.iea.org/reports/solar-pv-global-supply-chains.

Chinese firms also dominate the subsequent steps in solar manufacturing: monocrystalline silicon ingot production, silicon wafer slicing, solar PV cell production, and solar PV module assembly (Figure 2). The Chinese solar sector’s Xinjiang operations are much less extensive at these later steps of the supply chain, with a single known ingot and wafer factory owned by JinkoSolar Holdings Company (晶科能源控股有限公司) operating in the region.Laura T. Murphy and Nyrola Elimä, In Broad Daylight: Uyghur Forced Labour in Global Solar Supply Chains, Sheffield Hallam University, May 2021, https://www.shu.ac.uk/helena-kennedy-centre-international-justice/research-and-projects/all-projects/in-broad-daylight. Thus, the large majority of this production occurs in other provinces. For instance, over half (~180 GW) of Chinese ingot and wafer manufacturing capacity is located in Jiangsu, Yunnan, and Inner Mongolia,Basore and Feldman, Solar Photovoltaics.compared with <4 GW capacity at JinkoSolar’s Xinjiang facility.Cooper Chen, “Xinjiang Sanctions and the PV Supply Chain,” pv magazine, January 26, 2021, https://www.pv-magazine.com/2021/01/26/xinjiang-sanctions-and-the-pv-supply-chain/.Nevertheless, due to the large fraction of upstream solar manufacturing that takes place in the XUAR, many downstream operations are significantly exposed to Xinjiang production through their suppliers.

In addition to the solar manufacturing industry’s high degree of geographic concentration in China, solar manufacturing is also highly concentrated in terms of manufacturing infrastructure, with individual large factories often representing a sizeable fraction of global production. This concentration of production in a few large-scale facilities is most evident in early steps of the solar supply chain such as solar-grade polysilicon. A recent special report from the International Energy Agency warned about the potential risks posed by such infrastructure overconcentration: “one out of every seven panels produced worldwide is manufactured by a single facility. This level of concentration in any global supply chain would represent a considerable vulnerability; solar PV is no exception.”International Energy Agency, Solar PV Global Supply Chains: An IEA Special Report.

Overall, prospects for solar electricity today and in the foreseeable future—and the fate of much of current climate mitigation efforts—are currently sensitive to trends, policies, and events affecting the Chinese solar PV manufacturing industry.

Links to oppression in Xinjiang

At the same time, strong and intensifying human rights and environmental justice concerns associated with repressive Chinese government policies in Xinjiang carry significant ethical implications for solar industry activities in the region.

As discussed in this report, there is evidence that solar PV manufacturing companies and upstream raw material suppliers with operations in Xinjiang are complicit in the Chinese Communist Party’s wider systematic campaign of oppression against Uyghurs, Kazakhs, Kyrgyz, and other minoritized peoples in the Xinjiang region. International corporations and investors outside China arguably share much of the blame for this crisis, having tacitly prioritized reductions in manufacturing costs at the expense of adequate moral accountability in light of increasingly alarming reporting from Xinjiang.

In 2014, under President Xi Jinping’s administration, the ruling Chinese Communist Party commenced implementation of the “Strike Hard” campaign in the XUAR with the ostensible goal of curbing religious extremism throughout the Xinjiang region.Human Rights Watch, “‘Break Their Lineage, Break Their Roots’: China’s Crimes Against Humanity Targeting Uyghurs and Other Turkic Muslims,” April 19, 2021, https://www.hrw.org/report/2021/04/19/break-their-lineage-break-their-roots/chinas-crimes-against-humanity-targeting. Under this campaign, Chinese authorities have dramatically intensified targeted persecution of Uyghurs and other Turkic Muslim peoples, seeking to suppress traditional cultural and religious expression while forcing minoritized peoples into alignment with the government’s political and ideological agenda for the region.Austin Ramzy and Chris Buckley, “‘Absolutely No Mercy’: Leaked Files Expose How China Organized Mass Detentions of Muslims,” New York Times, November 16, 2019, https://www.nytimes.com/interactive/2019/11/16/world/asia/china-xinjiang-documents.html. Targeted Muslim groups have lost much of their freedom to travel within and outside ChinaUN, OHCHR Assessment of Human Rights Concerns. and now live under intense, sweeping surveillance.Chris Buckley and Paul Mozur, “How China Uses High-Tech Surveillance to Subdue Minorities,” New York Times, May 22, 2019, https://www.nytimes.com/2019/05/22/world/asia/china-surveillance-xinjiang.html. Meanwhile, the Chinese government has arbitrarily detained or imprisoned a shockingly high proportion of the XUAR’s Uyghur population within a vast, brutal prison camp system. Detainees are often held or imprisoned for years for arbitrary reasons including minor expressions of religious faith,Ivan Watson and Ben Westcott, “China’s Xinjiang Records Revealed: Uyghurs Thrown into Detention for Growing Beards or Bearing Too Many Children, Leaked Chinese Document Shows,” CNN, February 2020, https://www.cnn.com/interactiv.... experiencing physical and mental torture while living under abjectly inhumane conditions in detention or prison facilities.UN, OHCHR Assessment of Human Rights Concerns. Leaked government documents reveal standing orders that armed guards should shoot to kill if detainees attempt to escape.John Sudworth, “The Faces from China’s Uyghur Detention Camps,” BBC News, accessed October 20, 2022, https://bbc.co.uk/news/extra/85qihtvw6e/the-faces-from-chinas-uyghur-detention-camps.

Within this broader landscape of intense oppression throughout Xinjiang, a major human rights issue associated with solar manufacturing is exposure to forced labor through state-sponsored labor transfer programs.Murphy and Elimä, In Broad Daylight. Numerous international organizations including labor and human rights groups,Worker Rights Consortium, “Forced Labor,” accessed October 24, 2022, https://www.workersrights.org/issues/forced-labor/.Human Rights Watch, “‘Break Their Lineage, Break Their Roots.’” academic researchers,Murphy and Elimä, In Broad Daylight. United Nations agencies,UN, Contemporary Forms of Slavery; and UN, OHCHR Assessment of Human Rights Concerns. and the European UnionEuropean Parliament, "Forced Labour and the Situation of the Uyghurs.” have raised alarms about how such labor programs exhibit unacceptable patterns of discrimination and coercion. These initiatives enroll citizens from minoritized groups under the implicit threat of arrest and imprisonmentVicky Xiuzhong Xu et al., "Uyghurs for Sale: ‘Re-education,’ Forced Labour and Surveillance Beyond Xinjiang," Australian Strategic Policy Institute, March 1, 2020, https://www.aspi.org.au/report/uyghurs-sale. and employ them at farms, mines, workshops, and factories,Laura T. Murphy, Kendyl Salcito, and Nyrola Elimä, Financing & Genocide: Development Finance and the Crisis in the Uyghur Region, Atlantic Council, February 2022, https://www.shu.ac.uk/helena-kennedy-centre-international-justice/research-and-projects/all-projects/financing-and-genocide. not only throughout the Xinjiang region but across China.Xu et al., "Uyghurs for Sale.” Often, laborers are separated from their families and children, relocated many hundreds of kilometers away from their hometowns, and denied the freedom to travel, to see or contact loved ones, or to terminate their work arrangements.Murphy and Elimä, In Broad Daylight. Transferred workers receive low, discriminatory pay, sometimes with living expenses deducted,Darren Byler, “How Companies Profit from Forced Labor in Xinjiang,” The China Project, September 4, 2019, https://thechinaproject.com/2019/09/04/how-companies-profit-from-forced-labor-in-xinjiang/. undergo mandatory political indoctrination, and work long hours under potentially hazardous conditions.Murphy, Salcito, and Elimä, Financing & Genocide. In many cases, Chinese authorities transfer detainees of the XUAR’s prison camp system to labor programs after release as the next stage in their “re-education” process.Adrian Zenz, “Coercive Labor and Forced Displacement in Xinjiang’s Cross-Regional Labor Transfer Program: A Process-Oriented Evaluation,” The Jamestown Foundation, March 2021, https://jamestown.org/wp-content/uploads/2021/03/Coercive-Labor-and-Forced-Displacement-in-Xinjiangs-Cross-Regional-Labor-Transfers-A-Process-Oriented-Evaluation.pdf?x20357.

Evidence of extensive participation in labor transfer programs throughout the upstream solar supply chain has already been widely and independently documented by researchers and journalists, including but not limited to analysts at Horizon AdvisoryHorizon Advisory, “The CCP’s Forced Labor Program: Overview of Risks in Polysilicon and Solar Supply Chains,” 2020. and S&P Global Market Intelligence,Michael Copley, “Human Rights Allegations in Xinjiang Could Jeopardize Solar Supply Chain,” S&P Global, October 21, 2020, https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/human-rights-allegations-in-xinjiang-could-jeopardize-solar-supply-chain-60829945. as well as Bloomberg reportersDan Murtaugh, Colum Murphy, and James Mayger, “Secrecy and Abuse Claims Haunt China’s Solar Factories in Xinjiang,” Bloomberg, April 13, 2021, https://www.bloomberg.com/graphics/2021-xinjiang-solar/. and human rights scholars Adrian Zenz[34] and Nyrola Elimä and Laura Murphy (see Table 1).Murphy and Elimä, In Broad Daylight. Forced labor risks are sufficiently serious that the United States has passed legislation to restrict imports of solar PV goods produced in Xinjiang,H.R. 6256, 117th Congress (2021-2022), “To Ensure That Goods Made with Forced Labor.” while the European UnionPhilip Blenkinsop, “EU Proposes Banning Products Made with Forced Labour,” Reuters, September 14, 2022, https://www.reuters.com/markets/europe/eu-proposes-banning-products-made-with-forced-labour-2022-09-14/. and other countries like AustraliaHuman Rights Watch, “Australia: Act on China’s Abuses in Xinjiang,” September 13, 2022, https://www.hrw.org/news/2022/09/13/australia-act-chinas-abuses-xinjiang. are now contemplating similar measures. Solar manufacturing is primarily exposed to forced labor risks at three key points: raw material production, coal mining and power, and solar-grade polysilicon manufacturing.

Table 1: Selected evidence of potential links to labor exchange programs by Xinjiang-based companies and entities within or adjacent to the solar PV manufacturing chain. This table is not a comprehensive accounting of companies with Xinjiang-based operations implicated in labor transfer initiatives or of the open-source documentation catalogued to date. Readers should refer to the In Broad Daylight report by Murphy and Elimä for more extensive records.工人时报, “转移就业保障南疆贫困劳动力脱贫致富,” Weixin, 2020, https://archive.ph/8uOPQ. 京连, 张昌升, 王永鹏, 马淑珍. “荒原创伟业 匠心铸辉煌.” 人民网, 2018, https://archive.ph/2CZvH.国际能源网, “张新:科技创新是企业生存发展的不二法宝 (两会声音),” 2020, https://archive.ph/BJrps (originally at https://m.in-en.com/article/html/energy-2291443.shtml). 新疆访惠聚, “天山早春图——最美的是你们追梦的模样,” Weixin, 2019, https://archive.ph/qm4AI (originally at https://mp.weixin.qq.com/s?src...*gG50Anr8CGCTFVlX2xFv4mE064tAmy2jIBGsBJ698IrymRClAG2X7*gmLciUsA4IC&new=1).中金公司, “新疆大全新能源股份有限公司: 首次公开发行股票并在科创板上市招股说明书,” 2020, http://pdf.dfcfw.com/pdf/H2_AN202009111411081991_1.pdf.Colum Murphy, Tom Mackenzie, and Allen Wan. “A Xinjiang Solar Giant Breaks Ranks to Try and Woo the West,” Bloomberg News, 2021, https://www.bloomberg.com/news/features/2021-05-16/xinjiang-s-daqo-factory-opens-doors-to-counter-forced-labor-claims.Murphy and Elimä, In Broad Daylight.策勒县人民政府, “策勒县举办95名城乡富余劳动力赴乌鲁木齐、昌吉企业就业欢送仪式,” 2017, https://archive.ph/4T0aK (originally at http://www.xjcl.gov.cn/info/1071/42636.htm). 平安准东, “准东开发区党工委委员、公安分局局长刘肖文一行对彩南社区的喀什、和田地区富余劳动力转移就业人员进行走访慰问,” Weixin, 2017, https://archive.ph/g4pTL.胡洁, “714名和田贫困劳动力赴昌转移就业,” 昌吉市人民政府, 昌吉日报, 2020, https://archive.ph/fIEw2 (originally at http://www.cjs.gov.cn/xwzx/cjzyw/881995.htm).新疆访惠聚, “天山早春图——最美的是你们追梦的模样,” Weixin, 2019, https://archive.ph/qm4AI准东开发区零距离, “准东开发区转移乌恰县25名农村 富余劳动力来准东就业,” Weixin, 2020, https://archive.ph/f1KS4. “鄯善县合盛硅业系列项目开工建设,” 吐鲁番新闻, Weixin, 2017, https://archive.ph/ylFj8.神奇的迪坎, “迪坎乡组织富余劳动力到合盛硅业观摩并参加招聘会,” Weixin, 2017, https://archive.ph/VQb0h.最远一家人, “五个暖男和他们的’暖心账’,” Weixin, 2018, https://archive.ph/4VXBf.艾太强, “工作队帮居民实现就业增收梦,” 吐鲁番人民广播电台, 2018, https://archive.ph/kwq2V (originally at https://www.sohu.com/a/255710048_99910015).“关于新源县2020年新疆晶科能源有限公司一次性吸纳就业补贴的公示,” https://archive.ph/xVLlk (originally at http://www.xinyuan.gov.cn/info/1023/38491.htm).“关于新源县2020年第二批企业招用新疆籍人员享受社会保险补贴的公示,”https://archive.ph/IigEP (originally at http://www.xinyuan.gov.cn/info/1183/42352.htm).

Quartzite stone mining and metals companies in the XUAR utilize forced labor programs,“Chinese Solar Billionaire Doubles Fortune Despite US Sanctions,” Bloomberg News, August 11, 2022, https://www.bloomberg.com/news/articles/2022-08-11/china-solar-billionaire-gets-richer-after-us-sanctions-hoshine. supplying solar-grade polysilicon factories in Xinjiang with metallurgical-grade silicon, the key raw material for solar polysilicon production. A 2021 report by researchers at Sheffield Hallam University found that three of the major solar-grade polysilicon producers with significant XUAR operations—GCL Technology Holdings Limited (协鑫科技控股有限公司; formerly GCL-Poly Energy Holdings Company, 保利协鑫能源控股有限公司), Xinte Energy Company (新特能源公司), and East Hope Group (东方希望)—themselves participate in forced labor exchange programs, while the fourth major producer, Daqo New Energy Corporation (大全新能源股份有限公司), is directly exposed to forced labor through its raw material suppliers.Murphy and Elimä, In Broad Daylight. Other materials of concern include quartz for use in solar cover glass and aluminum,Horizon Advisory, “Forced Labor Risks in China’s Aluminum Sector,” April 2022, https://www.horizonadvisory.org/backtobasics. a common key input in solar module frames and in metallization employed in solar cell manufacture.Woodhouse et al., Crystalline Silicon Photovoltaic Module Manufacturing Costs and Sustainable Pricing.

Solar-grade polysilicon producers and other solar manufacturing activities in Xinjiang are additionally exposed to forced labor through the XUAR’s coal energy network. Much of the Xinjiang region’s coal mining and power generation takes place in vast state-sponsored industrial parks that extensively leverage labor transfer programs, with some solar-grade polysilicon factories located directly within these same industrial zones.Murphy and Elimä, In Broad Daylight.

Xinjiang’s role in China’s solar comparative advantage

The per-watt cost of a silicon-based solar PV module has plummeted rapidly over the past decade. The majority of this cost decline throughout the 2010s occurred thanks to genuine industry-wide technical progress, including technological standardization and improvements in manufacturing efficiency. Such real improvements are evidenced by how producers outside of China have achieved comparable cost declines over the same period. This is good news, as this history suggests that solar technology will largely remain as cheap as it is today even if the industry transitions away from unethical production in Xinjiang.

Likewise, many of China’s cost advantages in solar manufacturing are relatively real. However, state industrial policies such as heavy state subsidies for industrial parks and special electricity discounts for solar manufacturing firms may still intersect with human rights and environmental justice issues, as they impact minoritized peoples in the XUAR who have no voice in the government’s land use and environmental decision-making.

At the same time, even as the cost of solar modules has fallen, the relative importance of the cost advantages that unethical practices impart to Chinese firms has grown. This unethical component of the comparative advantages enjoyed by Chinese producers has helped drive international competitors out of solar manufacturing, contributing to current overconcentration of the global solar PV supply chain.

Electricity, energy, and polysilicon production

Cheap electricity is key to the competitive advantage of Xinjiang-based Chinese firms in solar-grade polysilicon production. Electricity represents more than 40% of the cost of manufacturing a unit of solar-grade polysilicon, an important input for a product with narrow profit margins.IEA, Solar PV Global Supply Chains.

In the XUAR, solar-grade polysilicon factories benefit from low-cost coal-fired electricity. Across the province, coal power plants provide 70% of the region’s electricity.International Energy Agency, “Power Generation, Export and Electricity Demand in Xinjiang Province, 2019: Charts, Data & Statistics,” accessed October 21, 2022, https://www.iea.org/data-and-statistics/charts/power-generation-export-and-electricity-demand-in-xinjiang-province-2019. Xinjiang contains as much as 40% of China’s total current coal reserves.Edward Wong, “China Invests in Region Rich in Oil, Coal and Also Strife,” New York Times, December 20, 2014, https://www.nytimes.com/2014/12/21/world/asia/china-invests-in-xinjiang-region-rich-in-oil-coal-and-also-strife.html. A recent IEA report on the solar manufacturing sector assessed electricity prices in the XUAR to be around $70/MWh, almost 30% lower than the global average industrial electricity price (Figure 3).IEA, Solar PV Global Supply Chains. Relative to electricity prices prior to Russia’s invasion of Ukraine, the IEA determined Xinjiang’s electricity rates were approximately one-third that of rates in Germany, where the German firm Wacker Chemie is one of the only major international solar-grade polysilicon manufacturers outside of China (ranked fourth in production capacity in 2022).Johannes Bernreuter, “The Top Ten: Ranking of the World’s Largest Polysilicon Manufacturers,” Bernreuter Research, updated September 26, 2022, https://www.bernreuter.com/polysilicon/manufacturers/#the-top-ten-ranking-of-the-world-s-largest-polysilicon-manufacturers.

However, the IEA’s assessment of XUAR electricity prices of $70/MWh is likely a significant overestimate. Recently published regulated pricing for large industrial customers in the XUAR lists rates that average $48-$58/MWh for time-of-day electricity sales.“Xinjiang Power Grid Announced a New Version of the Electricity Price List: The Same Price for the Sale of Electricity in the Large Industrial Electricity Catalog” (in Chinese), December 12, 2020, https://m.bjx.com.cn/mnews/20201209/1121142.shtml. Most solar-grade polysilicon production and metallurgical-grade silicon production also rely primarily upon dedicated on-site coal-fired power plants that directly serve the industrial facilities, as opposed to electricity purchased from the grid. These may offer functionally cheaper power. Additionally, posted electricity rates may not account for additional targeted direct subsidies.

Such use of coal-fired electricity to manufacture solar-grade polysilicon is the rule, not the exception. All four of the major facilities operated by polysilicon producers in Xinjiang either possess direct on-site coal power units or are located within 1-2 kilometers of large coal-fired power plants (Figures 4-7).

GCL Tech operates a large facility northeast of Ürümqi in the Zhundong Economic and Technological Development Zone (准东经济技术开发区) with an annual capacity of 40,000 tons/yrChen, “Xinjiang Sanctions and the PV Supply Chain.” representing a full 8.4% of China’s total solar-grade polysilicon capacity.Basore and Feldman, Solar Photovoltaics. This factory operates five on-site coal-fired generators in the northwest corner of the plant, while sitting just 4 kilometers from the lip of vast open-pit coal mines (Figure 4). To the southwest of GCL Tech’s factory, the Xinte Energy Company’s polysilicon plant is similarly conjoined with on-site coal power plants with six units (Figure 5). While Xinte’s facility also operates two small solar PV farms along the western edges of the factory, this generation capacity is marginal relative to the plant’s total energy demand. Daqo New Energy Corp. operates a large polysilicon plant north of the city of Shihezi, linked to several coal power plants a few kilometers to the north (Figure 6). Finally, East Hope Group’s factory in the Zhundong Zone sources electricity from as many as 16 coal-fired generators scattered throughout the plant (Figure 7), with apparent preparations for on-site factory expansion underway as of February 2022.See Maxar satellite imagery at 44.68N, 86.08E (Image ID: 1040010072CCDB00, captured February 24, 2022), accessed August 23, 2022, https://discover.maxar.com/.

Certainly, the use of coal energy in industrial applications is commonplace globally. However, coal-fired electricity in Xinjiang is strongly implicated in the region’s record of human rights abuses. State media publications and industry documentation provide direct evidence that coal-fired power plants in the XUAR employ forced labor.Murphy and Elimä, In Broad Daylight, reference 71 (https://archive.ph/qm4AI#selection-511.0-511.120). The Zhundong Economic and Technological Development Zone in particular makes extensive use of forced labor transfer programs,胡洁, “714名和田贫困劳动力赴昌转移就业,” 昌吉市人民政府, 昌吉日报, 2020, https://archive.ph/fIEw2 (originally at http://www.cjs.gov.cn/xwzx/cjzyw/881995.htm).新疆访惠聚, “天山早春图——最美的是你们追梦的模样,” Weixin, 2019, https://archive.ph/qm4AI. while hosting GCL Tech and East Hope Group’s large-scale solar-grade polysilicon plants within the same zone. As such, both coal mining activities and coal power facilities directly upstream of polysilicon production are likely taking advantage of unethical practices.

Public records suggest that power plants discriminate by employing Uyghurs and other minority workers in menial, undesirable roles such as cleaning accumulated coal dust from coal-fired boilers, while white-collar administrative roles are only open to Han Chinese.Shohret Hoshur, “Low Pay, Long Hours for Uyghurs in Chinese-Owned Plant in Xinjiang,” Radio Free Asia, September 1, 2022, https://www.rfa.org/english/news/uyghur/qinghua-energy-09012022134727.html. Personal testimony also documents that Uyghurs employed via forced labor programs may be forced to pay for their own company-provided food and transportation, further reducing the low wage they purportedly receive.Byler, “How Companies Profit from Forced Labor in Xinjiang.” Photographic evidence from other XUAR industrial facilities shows that workers often lack personal protective equipment required to shield them from injury and occupational exposure to harmful hazards.Murphy, Salcito, and Elimä, Financing & Genocide.

The region’s four major solar-grade polysilicon producers—GCL Tech, Xinte, East Hope, and Daqo—also have their own suspected links to forced labor programs (Table 1).Murphy and Elimä, In Broad Daylight.Copley, “Human Rights Allegations in Xinjiang.”Horizon Advisory, “CCP’s Forced Labor Program.” Labor represents a small fraction of per-unit polysilicon production costs,Woodhouse et al., Crystalline Silicon Photovoltaic Module Manufacturing Costs and Sustainable Pricing. and the overall proportion of coerced labor within the larger workforce at XUAR solar-grade polysilicon plants is unclear. Official incentive programs may reward companies with subsidies for participating in labor transfer initiatives, suggesting that the economic appeal of low-cost labor alone may be insufficient to incentivize corporate participation.UN, Contemporary Forms of Slavery. At the same time, if the compounded effects of forced labor at upstream supply chain steps and relatively unrestricted exploitation of environmentally impactful coal energy are considered, solar-grade polysilicon production in Xinjiang arguably does enjoy some unethical economic advantages from repressive government policies in the region.

In summary, for the reasons discussed above, there is evidence that the solar manufacturing sector in Xinjiang exploits forced labor and benefits considerably from intensive vertical integration of dirty, cheap coal-fired energy with polysilicon production. Evidence also implicates the coal value chain in Xinjiang itself in forced labor abuses. Coal mining and power generation are admittedly machinery- and capital-intensive activities as opposed to labor-intensive industries, limiting the direct economic advantage obtained from exploited labor. However, the intense prioritization of industrial efficiency in Xinjiang’s coal energy landscape results in part from political disenfranchisement of minoritized peoples throughout the region. The resulting sizable electricity cost advantages in turn help Chinese polysilicon producers maintain a lead over international competitors.

Raw materials sourcing

The solar manufacturing sector in Xinjiang also benefits from regional supply chains that provide important raw materials at low cost. These upstream inputs are heavily implicated in forced labor transfer programs, are promoted by repressive state-directed industrial policies, and depend upon the same coal mining and electricity generation activities mentioned above.

The chief input raw materials of concern are quartz rock and metallurgical-grade silicon (MGS), which are required upstream inputs for solar-grade polysilicon. Quarries mine quartz rock, while smelters crush this quartz and feed it into an electrode arc furnace where the silicon dioxide is reduced, yielding high-purity MGS.Basore and Feldman, Solar Photovoltaics. Other materials of concern include aluminum, used in solar module frames and in minor quantities for metallization pastes used in solar cell production.Woodhouse et al., Crystalline Silicon Photovoltaic Module Manufacturing Costs and Sustainable Pricing. With a recently announced large-scale investment in a PV cover glass factory to be built in Xinjiang, a future risk is also emerging that the supply chain for solar cover glass could become increasingly linked to XUAR production.Vincent Shaw and Max Hall, “Hoshine Expands PV Glass Output, Tongwei Raises Cell Prices,” Chinese PV Industry Brief, pv magazine, April 19, 2022, https://www.pv-magazine.com/2022/04/19/chinese-pv-industry-brief-hoshine-expands-pv-glass-output-tongwei-raises-cell-prices/.

Open job listings discovered by researchers at Sheffield Hallam University indicate that, as of 2019-2020, MGS plants employ manual laborers to crush quartz rock and feed it into furnaces to be smelted. Hiring advertisements hint at systematic discrimination, specifying no ethnicity restrictions for manual work but requiring that office and laboratory workers be Han Chinese. Open-source analysis of publicly available industry documentation and news reporting shows that the region’s largest MGS suppliers including Xinjiang Western Hoshine Silicon Industry Co., Ltd. (新疆西部合盛硅业有限公司), and Changji Jisheng New Building Materials Company (昌吉吉盛新型建材有限公司) participate in forced labor transfers.Murphy and Elimä, In Broad Daylight. As MGS production in electrode arc furnaces is highly electricity-intensive, the XUAR coal energy sector again plays a crucial role in upstream raw material production.Basore and Feldman, Solar Photovoltaics. Finally, quartz rock quarries and MGS smelters are themselves often located within industrial parks affiliated with the Xinjiang Production and Construction Corps (新疆生产建设兵团), a unique state military-economic entity that helps operate the region’s repressive detention camp system and labor transfer programs.Laura T. Murphy, Nyrola Elimä, and David Tobin, Until Nothing Is Left: China’s Settler Corporation and Its Human Rights Violations in the Uyghur Region, A Report on the Xinjiang Production and Construction Corps, Sheffield Hallam University, July 2022, https://www.shu.ac.uk/helena-kennedy-centre-international-justice/research-and-projects/all-projects/until-nothing-is-left.

Besides upstream solar-grade polysilicon inputs, XUAR industries also account for a sizeable fraction of other raw materials that may be employed in Chinese solar manufacturing. Primary aluminum factory capacity in Xinjiang represents 17% of total Chinese primary aluminum production and 11% of worldwide primary production.Horizon Advisory, “Forced Labor Risks in China’s Aluminum Sector.” As shown in Figures 5-7, large-scale aluminum smelters are often directly co-located adjacent to solar-grade polysilicon production in the region’s industrial parks, exposing such operations to the same forced labor risks present in the solar PV polysilicon and coal energy value chains. One of the region’s largest aluminum producers, Xinjiang East Hope Nonferrous Metals Co., Ltd., is also one of the top solar-grade polysilicon producers in the XUAR.Murphy and Elimä, In Broad Daylight. Indeed, a spring 2022 report by the consulting firm Horizon Advisory found evidence of forced labor program participation across numerous major aluminum companies in Xinjiang.Horizon Advisory, “Forced Labor Risks in China’s Aluminum Sector.” Aluminum produced in Xinjiang represents a sizable portion of domestic supply within China, and may consequently be incorporated into solar PV frames assembled by manufacturers across the country.

The extent to which quartz materials mined in Xinjiang currently support the solar PV cover glass industry is unknown. However, Hoshine Silicon Industry Co., Ltd., recently announced plans to expand its solar PV cover glass production capacity with a major new facility in Xinjiang that is coming online in summer 2023 with an annual manufacturing capacity of 3 million metric tons a year.Shaw and Hall, “Hoshine Expands PV Glass Output.” This quantity of solar PV cover glass is sufficient for ~43 GW/yr of finished monocrystalline silicon PV modules,IRENA, “Renewable energy benefits: Leveraging local capacity for solar PV,” IRENA, 2017, https://www.irena.org/-/ or approximately one-fourth of global solar deployment in 2021.Basore and Feldman, Solar Photovoltaics. Hoshine Silicon was directly sanctioned in 2021 by the U.S. government, which banned all imports of silica-based products in response to forced labor concerns.Thomas Kaplan, Chris Buckley, and Brad Plumer, “U.S. Bans Imports of Some Chinese Solar Materials Tied to Forced Labor,” New York Times, June 24, 2021, https://www.nytimes.com/2021/06/24/business/economy/china-forced-labor-solar.html?_ga=2.257386571.1740933571.1662073081-488683305.1642013884. With a known supplier of concern imminently and significantly expanding Xinjiang-based solar cover glass production, human rights risks may soon extend to this component of the solar PV supply chain.

Downstream risks

Due to the prominent market share of Xinjiang-based suppliers at the upstream steps in the solar manufacturing chain, cost advantages and ethical risks associated with Xinjiang MGS, aluminum, and polysilicon production are subsequently passed onto solar manufacturing companies across China and the world. These highly uniform commodities may be blended or comingled with materials sourced from factories outside Xinjiang, complicating efforts to accurately trace relationships between customers and suppliers. With raw materials representing a sizable fraction of costs at each step in the solar supply chain,Woodhouse et al., Crystalline Silicon Photovoltaic Module Manufacturing Costs and Sustainable Pricing. cheap and unethical manufacturing of key inputs may confer an important competitive advantage to companies sourcing such materials.

While small relative to the scale of ingot, wafer, cell, and module production elsewhere in China, some ingot and wafer manufacturing capacity exists in Xinjiang. Researchers at the Australian Strategic Policy Institute have identified two suspected prison facilities within 1.5 miles of the monocrystalline silicon ingot and wafer factory operated by JinkoSolar Holdings Company in Xinjiang at 43.46°N, 83.25°E.Nathan Ruser, “Exploring Xinjiang's Detention System: The World's Most Comprehensive Database, 380+ Facilities,” Australian Strategic Policy Institute, September 2020, https://xjdp.aspi.org.au/explainers/exploring-xinjiangs-detention-facilities/. Open-source investigation has also uncovered evidence that JinkoSolar’s Xinjiang operations have accepted workers via labor transfer programs.Murphy and Elimä, In Broad Daylight. This facility represented 42% of JinkoSolar’s 8 GW ingot manufacturing capacity as of 2021,Chen, “Xinjiang Sanctions and the PV Supply Chain.” with JinkoSolar as a whole ranking second among global solar PV module manufacturers and expecting to operate around 65 GW of PV module manufacturing capacity by the end of 2022.JinkoSolar, “JinkoSolar Announces Second Quarter 2022 Financial Results,” August 26, 2022, https://ir.jinkosolar.com/news-releases/news-release-details/jinkosolar-announces-second-quarter-2022-financial-results.

Finally, many other industries outside the solar sector may utilize MGS, aluminum, and high-purity polysilicon produced in Xinjiang factories. These multipurpose commodities are highly versatile and present in a dizzyingly wide range of products. For instance, media articles have touted the role of the XUAR’s polysilicon industry in supplying the consumer electronics sector.Liu Xiang, “Xinjiang: Accelerate the Extension of the Chain, Strengthen the Chain, and Promote the Development of Industrial Clusters” (in Chinese), Xinjiang Daily, August 25, 2021, https://archive.ph/f2wiW. MGS and aluminum from Xinjiang may also be present in aluminum alloys used in car manufacturing.Lily Kuo, Pei Lin Wu, and Jeanne Whalen, “Solar Industry’s Ties to China’s Xinjiang Region Raise Specter of Forced Labor,” Washington Post, June 24, 2021, https://www.washingtonpost.com/world/asia_pacific/solar-china-climate-xinjiang-labor/2021/06/24/810abbd6-c903-11eb-8708-64991f2acf28_story.html. Ultimately, these products represent just a portion of a larger crisis of unethical manufacturing across Xinjiang, with strong evidence of pervasive human rights and environmental abuses across numerous large-scale, globally traded supply chains from cotton and tomatoes to garments, pharmaceuticals, magnesium, batteries, and more.Murphy, Salcito, and Elimä, Financing & Genocide.

Examining past progress in solar manufacturing

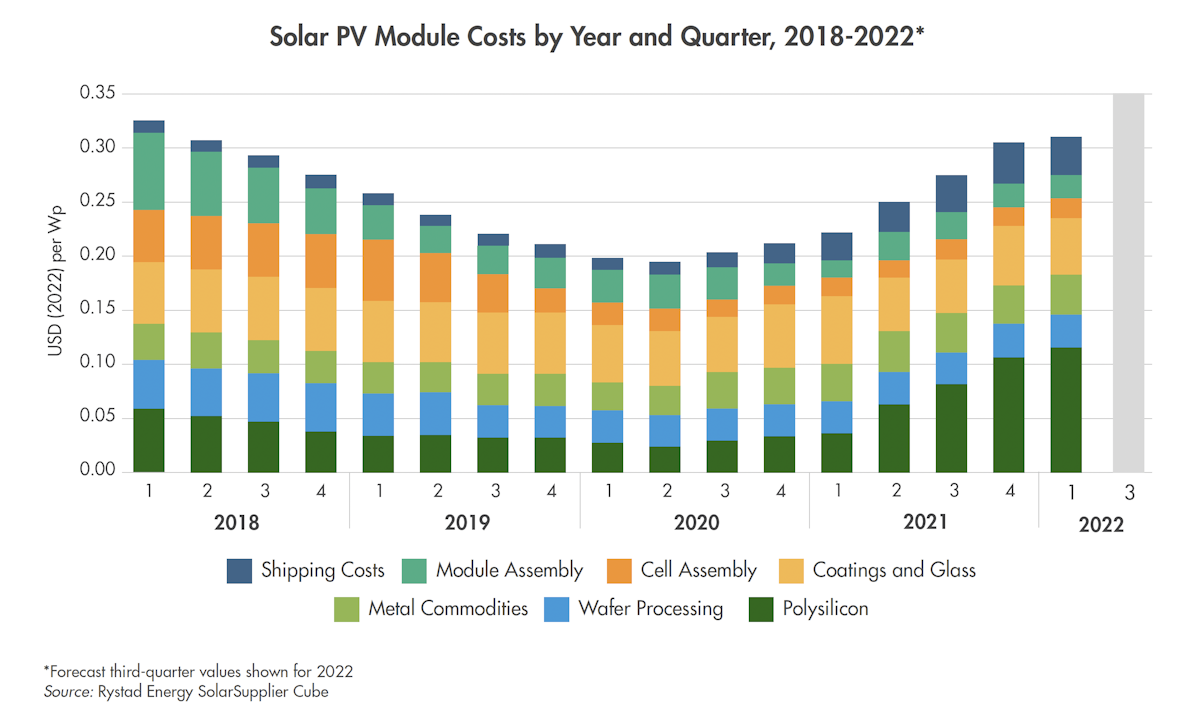

It is nevertheless important not to overexaggerate the degree to which unethical practices and foul play have contributed to Chinese firms’ overwhelming control over the global solar supply chain. Inflating the influence of such factors is to neglect real lessons from the historic improvement in solar technology costs and the rise of solar manufacturing in China. Unethical manufacturing may help solar companies keep solar commodity and module costs low today. However, the reduction in per-unit solar PV module costs over the last decade (Figure 8) also results from genuine technological improvements, large-scale targeted investments, and efficiencies of scale. This is welcome news, as the historical narrative demonstrates that the solar industry can likely reproduce many of these past cost improvements even while taking decisive steps to shun, pressure, and replace suppliers associated with human rights abuses.

Some commentators have attributed Chinese dominance in solar manufacturing largely to protectionist trade policies and market manipulation.E&E News, “Articles Archive” January 26, 2015, https://www.eenews.net/articles/page/1463/. Eric Wesoff, “SolarWorld Wins Again: Big Anti-Dumping Tariffs in US-China Solar Panel Trade Case,” Greentech Media, July 25, 2014, https://www.greentechmedia.com/articles/read/solarworld-wins-again-big-anti-dumping-tariffs-in-us-china-solar-panel-tra. Matt Sussis, “Not Everyone Convinced China to Blame for U.S. Solar Woes,” The Street, January 25, 2018, https://www.thestreet.com/politics/china-s-responsibility-for-solar-shutdowns-14463014.According to this narrative, the Chinese government propped up its domestic solar industry with favorable state subsidies while subjecting foreign competitors to heavy trade tariffs. At various times, policymakers“President Donald J. Trump Is Confronting China’s Unfair Trade Policies,” May 29, 2018, https://trumpwhitehouse.archives.gov/briefings-statements/president-donald-j-trump-confronting-chinas-unfair-trade-policies/. and industry figuresJames O’Toole, “U.S. to Investigate Chinese Solar ‘Dumping’ Claims,” CNNMoney, November 9, 2011, https://money.cnn.com/2011/11/09/technology/china_solar_investigation/index.htm. have alleged that Chinese firms conspire to dump manufactured products on international markets at prices lower than their cost of production.Evan Halper and Jeff Stein, “White House Alarmed That Commerce Probe Is ‘Smothering’ Solar Industry,” Washington Post, May 7, 2022, https://www.washingtonpost.com/business/2022/05/07/auxin-solar-projects-frozen/. These explanations are largely insufficient, inaccurate, or both.

The foundations for China’s dominance in solar manufacturing predate the solar PV trade disputes that began in 2012 as well as the Chinese government’s crackdown on the 2009 Ürümqi protests and its launch of the “Strike Hard” campaign of oppression starting in 2014. Rather, the nascent Chinese solar manufacturing industry emerged thanks to a combination of entrepreneurial initiative, public investment, international collaboration, and rapid nurturing of industry expertise throughout the late 1990s and early 2000s, accompanied by increasing international demand for solar products, particularly from Germany.Gregory Nemet, “How Solar Became Cheap: A Model for Low-Carbon Innovation,” accessed October 24, 2022, https://www.howsolargotcheap.com/china.

In 1983, researchers led by Professor Martin Green at the University of New South Wales (UNSW) in Australia engineered the passivated emitter rear contact (PERC) solar cell, setting a new world record in the conversion efficiency of solar energy to electricity.Andrew Blakers, “Development of the PERC Solar Cell,” IEEE Journal of Photovoltaics 9, no. 3 (May 2019): 629-35, https://ieeexplore.ieee.org/document/8653319. This and subsequent successes attracted a growing group of Chinese doctoral students and researchers to the Australian research group, many of whom would become executives and chief technical officers across the future Chinese solar industry.Martin Green, "How Did Solar Cells Get So Cheap?," Joule 3, no. 3 (2019): 631-33. UNSW researchers would expand collaboration with the nascent global solar industry and continue to pioneer record-breaking improvements to solar cell design over the next two decades.

Dr. Shi Zhengrong (施正荣), an alumnus of the UNSW group, returned to China in 2001 with the goal of establishing a solar manufacturing base in his home country.Martin Green, “Shi Zhengrong: Heroes of the Environment,” Time, October 17, 2007, https://content.time.com/time/...,28804,1663317_1663322_1669932,00.html. With financial support from the local Wuxi municipal government and assistance in equipment procurement and workforce training from Australian colleagues, Shi Zhengrong founded Suntech Power (尚德电力控股有限公司) and opened its first 10 MW manufacturing plant in 2002 in the vicinity of Shanghai. Suntech’s wildly successful IPO in 2005 raised 400 million in U.S. dollars,“Sun Sets on Suntech’s U.S. Listing,” Wall Street Journal, November 7, 2013, https://www.wsj.com/articles/BL-CJB-19454. igniting a fierce surge of interest in solar manufacturing among Chinese companies and international venture capitalists, and triggering successive waves of investment and market entry over the next several years.

Thus, Chinese firms and local policymakers perceived solar’s market potential early on and rapidly placed a high priority on solar technology and manufacturing. At the same time, in 2000 the German government boosted global demand for solar PV by enacting a feed-in tariff subsidizing new solar PV projects, a program that would ultimately incentivize approximately 7.6 GW of solar PV installations nationwide in around a decade.Martin Green, “How Did Silicon Solar Cells Get So Cheap?,” Lecture, University of New South Wales, Australia, November 9, 2016,Beijing would enact its own Renewable Energy Law in 2005, implementing a feed-in tariff in 2011 that would fortuitously cushion the domestic industry following the 2008 global financial crisis.Gregory F. Nemet, How Solar Energy Became Cheap: A Model for Low-Carbon Innovation (New York: Routledge, 2019). As such, the establishment of a vibrant solar manufacturing sector in China occurred in large part thanks to close professional networks, fast and decisive industry development, and fortunate timing with supportive global, national, and local policy drivers.Green, "How Did Solar Cells Get So Cheap?"

After rising PV startups in China established a successful business model and attracted growing investments in global capital markets, the national Chinese government began offering significant capital support in 2009, allowing for even more rapid expansion of the domestic industry.Green, “How Did Silicon Solar Cells Get So Cheap?,” Lecture. This coincided near-perfectly with increasing global demand for solar PV modules. While competing governments similarly recognized the solar sector’s future potential, they invested in new manufacturing capacity to a dramatically lesser magnitude.

By the early 2010s, many countries sought to support domestic solar manufacturing through tax incentives, public R&D support, or industrial policy, including the United States,Varun Sivaram, "The American Recovery & Reinvestment Act and the Rise of Utility-Scale Solar Photovoltaics: How US Public Policy During the Great Recession Launched a Decade-Long Solar Boom," American Energy Innovation Council and Bipartisan Policy Center, June 2020, https://bipartisanpolicy.org/download/?file=/wp-content/uploads/2020/06/The-Successful-Demonstration-of-Utility-Scale-PV.pdf. Taiwan,John A. Mathews, Mei-Chih Hu, and Ching-Yan Wu, "Fast-Follower Industrial Dynamics: The Case of Taiwan's Emergent Solar Photovoltaic Industry," Industry and Innovation 18, no. 2 (2011): 177-202. and Japan.Edgar Hahn, The Japanese Solar PV Market and Industry, EU-Japan Centre for Industrial Cooperation, November 2014, https://www.eu-japan.eu/sites/eu-japan.eu/files/PVinJapan.pdf. As of 2011, East Hope and GCL-Poly had begun constructing new factory capacity in Xinjiang. However, expanding large-scale production across the solar supply chain was simultaneously driving a growing oversupply crisis. Solar module average selling prices, for instance, plummeted between the start of 2011 and the start of 2013 from $1.75 to less than $0.70/watt, while solar-grade polysilicon spot prices fell from $75/kg to $16/kg—all relative to a February 2008 peak of $475/kg just a few years prior.Green, “How Did Silicon Solar Cells Get So Cheap?,” Lecture. While international competitors struggled to sell product and remain profitable, Chinese companies benefited from domestic experience competing in cheap manufacturing of globally traded goods with razor-thin profit margins. During this oversupply period, Chinese firms likely engaged in some dumping of solar PV commodities below cost to empty product inventories, keeping them in business while higher-cost firms abroad exited the market. Fierce domestic and international competition during this period drove aggressive further efforts to cut manufacturing costs, positioning the solar PV industry for a decade of cost improvements that would defy all expectations.

In terms of mercantilist policies, the United States was actually the first country to enact tariffs on imported solar products from China, levying an anti-dumping duty in May 2012 that ranged from 18.3% to 249.96%.Doug Palmer, “U.S. Sets Steep Final Duties on Chinese Solar Panels,” Reuters, October 10, 2012, https://www.reuters.com/article/us-usa-china-solar/u-s-sets-steep-final-duties-on-chinese-solar-panels-idUSBRE8991NR20121010. Beijing policymakers responded in kind by imposing duties on imported solar goods from South Korea and the U.S.Reuters Staff, “China Hits U.S., South Korea with Solar Material Duties, Skirts EU Decision,” Reuters, July 18, 2013, https://www.reuters.com/article/us-china-dumping/china-hits-u-s-south-korea-with-solar-material-duties-skirts-eu-decision-idUKBRE96H0F520130718. and eventually implementing retaliatory tariffs on EU goods in other sectors.Yu Chen, “EU-China Solar Panels Trade Dispute: Settlement and Challenges to the EU,” European Institute for Asian Studies, June 2015, https://eias.org/wp-content/uploads/2016/02/EU-Asia-at-a-glance-EU-China-Solar-Panels-Dispute-Yu-Chen.pdf. European manufacturers ultimately negotiated to reduce these tariffs.Chen, “EU-China Solar Panels Trade Dispute.” Yet the Chinese government has extended tariffs on American- and Korean-made polysilicon for the foreseeable future.“New Chinese Polysilicon Duties Are Slap in the Face to Trade Deal,” Polysilicon News, Bernreuter Research, January 19, 2020, https://www.bernreuter.com/newsroom/polysilicon-news/article/new-chinese-polysilicon-duties-are-slap-in-the-face-to-u-s-trade-deal/.

In that period of the early 2010s, however, Chinese firms were already capturing global market share at a rapid pace, adding new factory capacity at scales that dwarfed competing efforts abroad.IEA, Solar PV Global Supply Chains. Large-scale manufacturing capacity helped the Chinese industry attain substantial economies of scale. Simultaneously, solar PV industry standardization and optimization efforts in China and internationally gravitated toward selection of the monocrystalline silicon PERC solar cell, which offered high performance while also simplifying production.Basore and Feldman, Solar Photovoltaics.

Solar photovoltaics have thus achieved the large majority of their cost declines over the past decade thanks to real technological innovations in manufacturing efficiency and module design. As a result of these factors, the cost per watt of a solar PV module fell by 75% between the start of 2013 and the start of 2020 (Figure 8),David Feldman et al., US Solar Photovoltaic System and Energy Storage Cost Benchmark (Q1 2020), NREL/TP-6A20-77324, National Renewable Energy Lab, January 2021, https://www.nrel.gov/docs/fy21osti/77324.pdf. while the global solar manufacturing sector continued to consolidate within China.

But while the Chinese solar manufacturing sector’s birth and initial growth had little connection to Xinjiang, this same period saw the industry becoming increasingly tied to the region and to the Chinese government’s oppressive policies. Labor transfer programs were already operating in the XUAR as solar-grade polysilicon factories first began local development around 2010.Li Xiaoxia, “新疆少数民族产业工人队伍发展及现状分析,” 北方民族大学学报(哲学社会科学版), 2015. http://www.shehui.pku.edu.cn/u... Since 2014, when the Chinese Communist Party launched its “Strike Hard” campaign, and especially after 2017 when initial reports began to emerge of mass incarceration of Uyghurs and Kazakhs, successive waves of growth in the region’s solar manufacturing sector have chronologically coincided with intensifying state repression of its minoritized peoples.

From its foundation of progress over the last 10 years, the solar industry now seems poised for a new explosive growth period on top of a decade of market performance that well exceeded most expectations. Yet like previous expansions of solar manufacturing capacity, this imminent growth phase threatens to tie the future of the global solar sector even more inextricably to unethical production in Xinjiang.

An industry sensitive to Xinjiang-based production

Recently, solar PV module costs have stopped falling. Since the start of the COVID-19 pandemic in early 2020, module costs increased by 50% between the second quarter of 2020 and the first quarter of 2022 (Figure 9).Jonathan Gifford, “Higher PV Module Prices May Point to Stable Demand and More Sustainable Pricing Trends,” pv magazine, January 4, 2022, https://www.pv-magazine.com/2022/01/04/higher-pv-module-prices-may-point-to-stable-demand-and-more-sustainable-pricing-trends/. A combination of increasing demand, global supply chain shocks, production pauses,Jules Scully, “‘Ceaseless’ Polysilicon Price Rises in China as Production Falls Below Forecasts,” PV Tech, June 23, 2022, https://www.pv-tech.org/ceaseless-polysilicon-price-rises-in-china-as-production-falls-below-forecasts/.Max Hall and Vincent Shaw, “Tongwei Temporarily Halts Polysilicon Output in Sichuan,” Chinese PV Industry Brief, pv magazine, August 16, 2022, https://www.pv-magazine.com/2022/08/16/chinese-pv-industry-brief-tongwei-temporarily-halts-polysilicon-output-in-sichuan/. and industrial accidents“Fire Halts Polysilicon Production at East Hope for One Month,” Polysilicon News, Bernreuter Research, June 28, 2022, https://www.bernreuter.com/newsroom/polysilicon-news/article/fire-halts-polysilicon-production-at-east-hope-for-one-month/. at polysilicon plants in ChinaBloomberg News, “Polysilicon Makers Shares Soar After Blast at Chinese Plant,” Bloomberg, July 20, 2020, https://www.bloomberg.com/news/articles/2020-07-21/gcl-poly-shuts-major-polysilicon-plant-after-xinjiang-explosions. have brought solar module costs back to levels last seen in early 2018.

As a result, the global solar sector is more sensitive to PV module prices now than it has been for years. Commodity price increases have driven rising costs, with PV module costs today tied almost directly to the cost and availability of solar-grade polysilicon. Industry experts now look more intently than ever to news and announcements from Chinese firms that dominate polysilicon production as an indicator of near-term future market trends.Jules Scully, “Solar Module and Polysilicon Prices to Decline from 2023, Report Finds,” PV Tech, August 29, 2022, https://www.pv-tech.org/solar-module-and-polysilicon-prices-to-decline-from-2023-report-finds/.

While these recent fluctuations still leave solar as one of the most affordable unit-level electricity generation options in existence,U.S. Energy Information Administration, “Cost and Performance Characteristics of New Generating Technologies, Annual Energy Outlook 2022,” March 2022, https://www.eia.gov/outlooks/aeo/assumptions/pdf/table_8.2.pdf. the rapidly changing economics of solar project development are subjecting the industry to some turmoil. Recent U.S. solar industry surveys conducted by the Solar Energy Industries Association suggest that many developers have postponed or shelved new projects due to heightened costs and shortages of solar PV components in addition to supply chain delays, COVID-19 disruptions, and the threat of import tariffs.Kavya Balaraman, “California Solar, Storage Projects Hit Hard by Department of Commerce Investigation, Supply Chain Issues,” Utility Dive, May 23, 2022, https://www.utilitydive.com/news/california-solar-storage-department-commerce-investigation/624222/. The U.S. solar sector’s intense, organized opposition“Commerce Department Decision Imperils U.S. Clean Energy Progress,” Solar Energy Industries Association, March 28, 2022, https://www.seia.org/news/commerce-department-decision-imperils-us-clean-energy-progress. to the Department of Commerce’s investigation into allegations of industry circumvention of solar import tariffs demonstrates this general apprehension around supply chain sourcing. These organized efforts ultimately convinced the Biden administration to grant a two-year grace period protecting the U.S. solar sector from new tariffs.“President Biden Takes Bold Executive Action to Spur Domestic Clean Energy Manufacturing,” The White House, Fact Sheet, June 6, 2022, https://www.whitehouse.gov/briefing-room/statements-releases/2022/06/06/fact-sheet-president-biden-takes-bold-executive-action-to-spur-domestic-clean-energy-manufacturing/.

Yet the solar industry’s fundamentals remain strong. Upstream manufacturers, particularly in China, are making large-scale new investments in industrial plant capacity as they prepare to meet anticipated future demand. It is reasonable to expect that, under the status quo, the solar sector’s current supply chain anxieties will be transient, and the imminent future will produce a return to year-on-year solar PV module cost declines. But should the solar industry proceed blindly along a business-as-usual path, the next few years will only further deepen the solar sector’s reliance on Chinese manufacturers.

As for the near future, a diverse array of projections anticipates sizable records in new solar power deployments in 2022 and beyond. This year, 190 GW of new solar capacity may be installed globally,International Energy Agency, Renewable Energy Market Update: Outlook for 2022 and 2023, May 2022, 7, https://iea.blob.core.windows.net/assets/d6a7300d-7919-4136-b73a-3541c33f8bd7/RenewableEnergyMarketUpdate2022.pdf. a 25% improvement over installed capacity in 2021. Worldwide deployment rates might grow to 250-266 GW per year by mid-decade.Sadhana Shenvekar, “Global Solar Installations Will Reach 2 TW by 2025: Global Market Outlook,” SolarQuarter, July 22, 2021, https://solarquarter.com/2021/...; and Basore and Feldman, Solar Photovoltaics. At an assumed 2,930 tons of polysilicon per 1 GW of monocrystalline silicon solar capacity, that implies global production of 780,000 tons of polysilicon per year, with total global solar capacity reaching up to 2,500 GW by 2030.“Solar Energy Could Power 13% of the World by 2030,” IRENA, June 22, 2016, https://www.irena.org/newsroom/articles/2016/Jun/Solar-Energy-Could-Power-13-of-the-World-by-2030. Under a highly ambitious future scenario such as the IEA’s net-zero emissions by 2050 pathway, solar capacity installed annually reaches 630 GW by 2030, implying annual manufacturing capacity in excess of 800 GW.International Energy Agency, Net Zero by 2050: A Roadmap for the Global Energy Sector, May 2021, https://www.iea.org/reports/net-zero-by-2050. The IEA’s 2050 net-zero pathway models a cumulative global installed capacity of 5,000 GW by 2030.

To meet this demand, Chinese firms have begun to rapidly expand solar manufacturing capacity at a record pace,Sandra Enkhardt, “BloombergNEF Says Global Solar Will Cross 200 GW Mark for First Time This Year, Expects Lower Panel Prices,” pv magazine, February 1, 2022, https://www.pv-magazine.com/2022/02/01/bloombergnef-says-global-solar-will-cross-200-gw-mark-for-first-time-this-year-expects-lower-panel-prices/. targeting multiple steps in the supply chain. The module manufacturer Longi is set to invest over $2 billion for a new facility in Erdos City, Inner Mongolia, with annual production capacity for 20 GW of ingots and wafers, 30 GW of solar cells, and 5 GW of modules.Vincent Shaw and Max Hall, “Xinte Wants to Add Another 200,000 Tons of Polysilicon Capacity,” Chinese PV Industry Brief, pv magazine, March 15, 2022, https://www.pv-magazine.com/2022/03/15/chinese-pv-industry-brief-xinte-wants-to-add-another-200000-tons-of-polysilicon-capacity/. Longi also has plans to build a 20 GW module factory in Wuhu, Anhui province.Vincent Shaw, “Longi to Build 20 GW Solar Module Plant,” Chinese PV Industry Brief, pv magazine, May 17, 2022, https://www.pv-magazine.com/2022/05/17/chinese-pv-industry-brief-longi-to-build-20-gw-solar-module-plant/. Xinte Energy will be investing $2.8 billion to expand its polysilicon manufacturing capacity in Xinjiang by 200,000 tons/yr with a new factory to be built near Changji in two 100,000 ton/yr stages.Shaw and Hall, “Xinte Wants to Add Another 200,000 Tons.” / Risen Energy is investing $7 billion for a new PV manufacturing facility in Inner Mongolia.“Risen Energy Plans to Build $7bn Solar PV Manufacturing Plant in China,” Power Technology, updated July 20, 2022, https://www.power-technology.com/news/risen-solar-manufacturing-china/. These are just a few of the massive expansion projects underway.

In total, as of a July 2021 survey, China has at least 300,000 tons of new annual polysilicon manufacturing capacity under construction and another 300,000 tons of new capacity announced.Basore and Feldman, Solar Photovoltaics. Chinese firms have 100 GW of ingot and wafer factory capacity under construction, with a further 100 GW of capacity announced (Figure 10). Cell manufacturers in China are expanding production by at least 50 GW, with over 125 GW of additional capacity announced. Finally, factories conducting solar PV module assembly in China will grow by 50 GW in the near term, with over 125 GW of announced projects to follow.Basore and Feldman, Solar Photovoltaics. These values are already a substantial undercounting, as many large new projects have been announced in the intervening year including several of the factory announcements detailed above. Recent research by Bloomberg analysts suggests that existing and announced polysilicon manufacturing capacity may attain 940 GW worth of annual production by 2025.David Fickling, “The Supply Chain to Beat Climate Change Is Already Being Built,” Bloomberg, September 6, 2022, https://www.bloomberg.com/opinion/articles/2022-09-06/solar-industry-supply-chain-that-will-beat-climate-change-is-already-being-built?srnd=opinion.

Given increasing scrutiny and criticism of Chinese solar manufacturing in Xinjiang, such developments threaten to entangle the global solar industry in a culture where supply chain human rights and environmental concerns are too painful and inconvenient to confront. Further hesitancy will only intensify this challenge.

Without immediate action, not only may the future of solar energy become locked into complicity with the Chinese government’s crimes against humanity, but inaction may prolong the solar industry’s dependence on low-cost products that stifle innovation, contribute excessively to climate and environmental impacts, and increase long-term supply chain risks for the industry as a whole. In the following sections, we elaborate upon the moral and societal risks such dynamics pose to the solar sector and to the world community at large.

Moral complicity in forced labor

Outside of China, the environmental movement has rightly fought to ensure that climate change mitigation efforts do not inflict unjust, disproportionate harm on vulnerable peoples in the name of the greater global good. Whether advocating for the protection of communities in lithium mining regions of Chile, Bolivia, and ArgentinaThea Riofrancos, “Shifting Mining from the Global South Misses the Point of Climate Justice,” Foreign Policy, February 7, 2022, https://foreignpolicy.com/2022/02/07/renewable-energy-transition-critical-minerals-mining-onshoring-lithium-evs-climate-justice/. or when demanding strong policies to support coal miners through the clean energy transition,Jeff Turrentine, “We Need a Just Transition—Because We Should Abandon Coal, Not Coal Workers,” NRDC, October 18, 2019, https://www.nrdc.org/onearth/we-need-just-transition-because-we-should-abandon-coal-not-coal-workers. policymakers and environmental advocates strive to protect groups that could bear unfair costs as the world seeks to reduce carbon emissions. Yet as evidence of the solar manufacturing sector’s ties to crimes against humanity in Xinjiang continues to accumulate, activists, policymakers, and the clean energy industry have remained unusually silent.

A recent special report on the global solar PV supply chain by the International Energy Agency, for instance, conspicuously makes no mention of forced labor risks associated with Xinjiang-based manufacturers. And when a reporter at the COP26 international climate conference asked U.S. Special Climate Envoy John Kerry about solar energy, forced labor, and the Xinjiang region, he evasively replied that such concerns were “not my lane.”Callie Patteson, “John Kerry Sidesteps China’s Human Rights Violations, Says It’s ‘Not My Lane,’” New York Post, November 11, 2021, https://nypost.com/2021/11/11/john-kerry-china-human-rights-violations-not-my-lane/. Numerous major international environmental advocacy organizations including the Natural Resources Defense Council, Greenpeace, and Friends of the Earth lack any mention of environmental or human rights issues in Xinjiang on their websites, with many of these groups declining to speak with reporters on such questions.Nithin Coca, “COP26 Is Silent on Human Rights in China,” Foreign Policy, November 9, 2021, https://foreignpolicy.com/2021/11/09/china-human-rights-cop26-climate-change-uyghurs-tibet-hong-kong-xinjiang/.

Such silence and evasions are unconscionable. Environmental justice efforts should not stop at the borders claimed by the Chinese Communist Party, lest the climate movement wish to signal its willingness to tolerate inequitable sacrifice zones (geographic areas permanently impaired by heavy environmental damage) so long as they only affect Muslim or Asian peoples living under Chinese government authority. If the world is to truly prioritize climate justice, then the global community must take all necessary measures to eliminate forced labor risks throughout clean energy supply chains, no matter where such risks exist.

Some may counter that the true extent of forced labor and environmental injustice in the Xinjiang solar manufacturing chain is not only unknown, but likely small, while the Xinjiang industry is itself only a fraction of larger Chinese production.Jules Scully, “US Solar Facing Fresh Shipment Delays as UFLPA Enforcement Raises Quartzite Queries,” PV Tech, June 29, 2022, https://www.pv-tech.org/us-solar-facing-fresh-shipment-delays-as-uflpa-enforcement-raises-quartzite-queries/; and Sean Rai-Roche, “Uyghur Forced Labor Prevention Act Comes into Force in the US,” PV Tech, June 21, 2022, https://www.pv-tech.org/us-uyghur-forced-labor-prevention-act-uflpa-starts-today-relating-solar-pv-products-chinas-xinjiang-region/. For instance, the world’s largest polysilicon producer is Tongwei Solar Company, which has no XUAR-based operations.Murphy and Elimä, In Broad Daylight. Many solar manufacturing activities such as solar-grade polysilicon production, ingot manufacturing, and wafer slicing are capital- and machinery-intensive as opposed to labor-intensive and likely rely heavily upon skilled and specialized workers to operate production lines. As such, use of forced labor in such facilities may not be as intensive and pervasive as it is in the XUAR’s cotton, tomato, or garment industries.Ana Swanson, “U.S. Bans All Cotton and Tomatoes from Xinjiang Region of China,” New York Times, January 13, 2021, https://www.nytimes.com/2021/01/13/business/economy/xinjiang-cotton-tomato-ban.html. Furthermore, labor represents a relatively small fraction of per-unit polysilicon costs.Woodhouse et al., Crystalline Silicon Photovoltaic Module Manufacturing Costs and Sustainable Pricing.

However, forced labor risks and any associated cost advantages for solar-grade polysilicon manufacturers are compounded thanks to upstream forced labor exploitation for inputs like coal energy and minerals. Upstream industries like quartzite rock mining and metallurgical-grade silicon smelting are likely to be more labor-intensive, with corporate and press documentation indicating regular use of manual labor at such sites in Xinjiang.Murphy and Elimä, In Broad Daylight. Even at polysilicon plants themselves, numerous supporting worker roles may not require skilled training or advanced technical expertise. The International Renewable Energy Agency assesses that, across the solar supply chain, 60% of the workforce requires only minimal training.International Renewable Energy Agency (IRENA), Renewable Energy and Jobs: Annual Review 2021, 2021, https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2021/Oct/IRENA_RE_Jobs_2021.pdf. Indeed, records of Uyghur workers transferred to JinkoSolar in spring 2020 listed educational levels that ranged from junior high to undergraduate college.Murphy and Elimä, In Broad Daylight, reference 233. Meanwhile, downstream customers that purchase a blended mix of commodities from XUAR- and non-XUAR-based facilities may indirectly benefit from XUAR-based production even if they do not directly operate in the region.

Given the tight profit margins under which the polysilicon industry operates, small changes in manufacturing and input commodity costs could deliver disproportionate benefits. Furthermore, direct labor force considerations may not reflect beneficial subsidies and treatment that manufacturers receive from official programs in consideration of their participation in state-sponsored labor transfer initiatives. At the same time, the existence of such subsidy programs may suggest that the competitive advantage of low-cost labor alone is insufficient to incentivize corporate involvement in labor transfer programs.

Initial efforts by solar industry actors to trace solar supply chains in response to forced labor concerns are disappointing. The Solar Energy Industries Association’s guidance protocol for solar supply chain tracing, for instance, is focused on tracking and excluding specific batches of product manufactured with a risk of forced labor, instead of seeking to exclude upstream suppliers whose operations wholly or partially exploit forced labor programs.Solar Energy Industries Association, Solar Supply Chain Traceability Protocol 1.0. SEIA’s traceability protocol only covers the commodity chain between metallurgical-grade silicon and completed solar PV modules, omitting upstream sourcing of quartz rock as well as inputs like aluminum and solar PV cover glass. Even though unexpectedly strict enforcement of the Uyghur Forced Labor Prevention Act in the United States has, in particular, mandated documentation of quartz rock sourcing that solar PV importers did not anticipate,Scully, “US Solar Facing Fresh Shipment Delays.” SEIA’s protocol has not been revised since its initial version was published in April 2021.

Current industry efforts, to the extent that they exist, are thus narrowly focused on avoiding individual shipments from Xinjiang-based factories. Such initiatives would permit purchase of “Xinjiang-free” material manufactured outside of the XUAR, even if the parent manufacturer is simultaneously operating factories within the XUAR. This narrow policy raises the risk of bifurcation, by allowing suppliers to cultivate a separate Xinjiang-free supply chain for more conscientious customers even while continuing to profit from Xinjiang-manufactured products sold separately.James Cockayne, Edgar Rodríguez-Huerta, and Oana Burcu, “Solar Energy, Modern Slavery and the Just Transition,” University of Nottingham, March 2022, https://www.nottingham.ac.uk/research/beacons-of-excellence/rights-lab/research-projects/solar-energy-modern-slavery-and-the-just-transition.aspx. Chinese manufacturers may already be shifting toward providing sanitized products to foreign markets while reserving forced-labor products for domestic or unscrupulous buyers.Emma Foehringer Merchant, “Is US Solar Ready to Prove Its Panels Aren’t Made with Uyghur Forced Labor?,” Canary Media, June 21, 2022, https://www.canarymedia.com/articles/solar/is-us-solar-ready-to-prove-its-panels-arent-made-with-forced-labor.