Could Geothermal Solve Latin America and the Caribbean's Energy Woes?

The case for pushing forward on this firm, clean source of energy

-

-

Share

-

Share via Twitter -

Share via Facebook -

Share via Email

-

Geothermal energy, which utilizes heat originating in the Earth’s core, provides a steady, non-intermittent source of renewable energy.

The intense heat comes from decaying radioactive particles, and it permeates up through the layers of the Earth’s mantle and crust. Geothermal power plants access this energy deep underground, through geothermal wells typically starting at 300℉ (149℃) as the lowest required high-temperature, harnessing it for electricity and heat applications.

Around the world, nations are more interested in geothermal energy than ever. Across Europe, for example, Denmark, France, Germany, and Italy are expanding geothermal capacity to replace natural gas for electricity and heating. Advanced geothermal technology companies are multiplying, with new players like Fervo, Quaise, and GreenFire Energy pursuing commercial-scale projects.

Although advanced geothermal is mostly progressing in wealthier countries, it is promising for low and middle-income ones as well. As these nations seek to industrialize while also meeting net-zero goals, geothermal energy could offer a valuable—and largely untapped—clean energy resource. Geothermal potential varies globally, but in particular, two regions have particularly high untapped potential: Latin America and the Caribbean.

The geological characteristics of both regions are favorable. The Eastern Caribbean islands are largely volcanic, while many parts of Central America and the western rim of South America border tectonic fault lines, including the “Ring of Fire” along the Pacific Coast of South America. The Ring of Fire is one of the most active geothermal regions in the world.

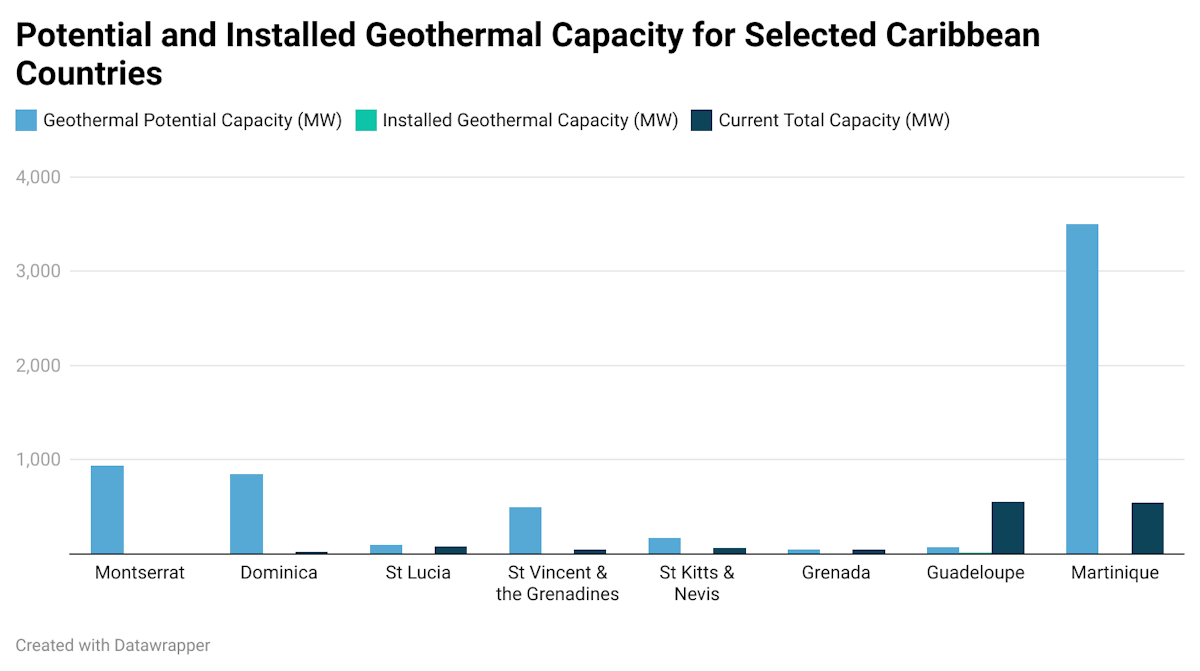

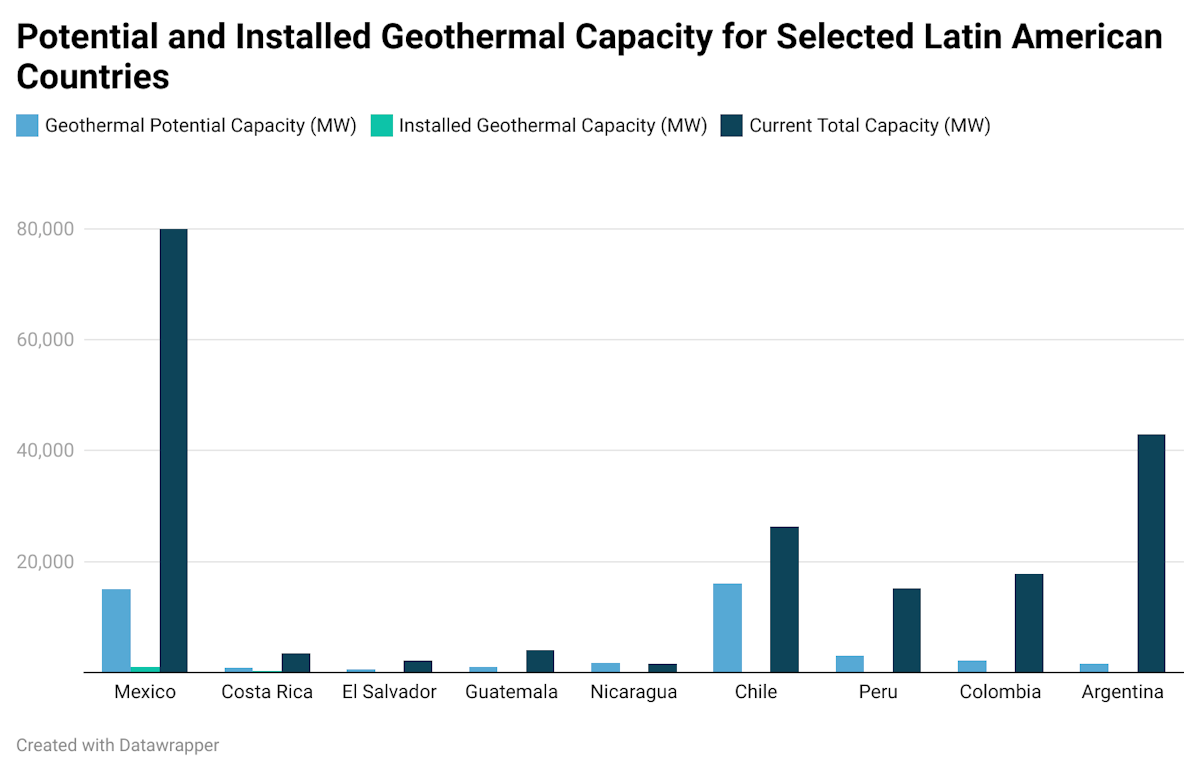

Across Latin America and the Caribbean, there are already numerous geothermal projects underway or completed. In total, about1716 MW of installed geothermal power operates there today. Mexico possesses the bulk of Latin America’s geothermal capacity, with a total of 1005 MW. In sharp contrast, the Caribbean possesses only 15 MW of installed capacity. Both regions’ untapped geothermal potential—between 55 GW and 70 GW—dwarfs geothermal capacity online today. In some Caribbean countries, particularly volcanic islands in the Eastern Caribbean, geothermal energy may be able to single-handedly supply existing local energy demands, which are currently met overwhelmingly with fossil fuels.

Adding more reliable clean energy to the mix is urgent. Together, by 2040, these regions’ total primary energy demand is expected to be at least 80% higher than it is today as these countries strive for continued economic development. At the same time, many countries across both regions have committed to becoming net zero by 2050. Geothermal energy—which is firm, clean energy that can support renewables while efficiently utilizing scarce land—could help make both goals possible.

An Asset for Energy Security and Affordability

Energy security circumstances vary from country to country across both Latin America and the Caribbean. Oil-rich countries like Venezuela and Trinidad and Tobago enjoy good energy security, while countries like Jamaica and Cuba without domestic fossil fuel resources typically rely on expensive energy imports to meet most or all of their energy needs. About 90% of the Caribbean’s energy supplies are imported, resulting in some of the world’s highest energy prices. Market fluctuations, such as those caused by Russia’s war on Ukraine, further exacerbate such costs, and have heavily raised expenses for import-dependent nations like the Caribbean islands. Transforming these nations’ energy systems could deliver increased energy security and affordability.

And even oil-rich nations like Trinidad and Tobago must begin seeking alternative energy resources as global decarbonization threatens the competitiveness of fossil fuel dependent economies. While hydro-rich countries of Central and Latin America like Brazil experience fewer energy security vulnerabilities, they too exhibit growing energy needs that geothermal energy could help support, particularly given ongoing regional expansion of hard-to-decarbonize industrial sectors like cement and steel production. Hydro-rich nations must also consider potential energy system disruptions from extreme weather events, which will become more likely with climate change. Across Latin America and the Caribbean, geothermal energy could thus prove valuable for ensuring energy system reliability while positioning these regions for continued economic growth.

Geothermal power is more expensive to install than other renewables like wind and solar. But wind and solar only will not make a resilient energy future for Latin America and the Caribbean.

Much of the Caribbean has year-round sunshine and wind that are well-suited for intermittent renewables. But there is much more variation in Latin America, with some countries like Chile and Argentina having much greater seasonality in their weather. Latin American countries do tend to have good renewable resources with considerable hydropower potential alongside large reserves of oil and gas.

But even in the places where wind and solar are fairly reliable, it will need to be supplemented with firm energy sources that can keep the lights on when the sun isn’t shining or when the wind isn’t blowing. Geothermal can do that. Even hydro-rich countries like Chile already experience periods of lower generation during drought events. Geothermal can thus support continued production of emissions-free energy during environmental and seasonal fluctuations that batteries may not be able to cost-effectively compensate for.

As an added benefit, geothermal is less vulnerable to weather-related disasters, which is important in a region that regularly experiences hurricanes, floods, and other natural disasters.

In turn, although solar and wind energy technologies are cheaper to deploy on a per-unit basis, installing a few geothermal plants could both buttress the overall system against disaster while also lowering overall system costs compared to installing large volumes of solar, wind and battery storage systems, and their supporting transmission and ancillary services infrastructure. Indeed, research shows that firm energy sources can also lower the overall costs of deep decarbonized energy systems. And lower energy costs can drive further economic growth.

Due to geographic differences, not all countries can access abundant geothermal power. But this is no different from how some nations lack the characteristics to reliably and affordably use solar, wind or hydropower to meet demand all-year round. One consideration particularly important for Caribbean small island nations is that renewable energy performance is less reliable for countries with small land space because there is less spatial variance in solar and wind performance to cushion periods of low generation. The latest energy systems research shows that electricity grid performance is more resilient and reliable when renewables are supported by firm, clean, dispatchable energy sources like geothermal. Firm energy sources can also lower the overall costs of deep decarbonized energy systems. Lower energy costs in Latin America and the Caribbean, thanks in part to efficient and reliable grid operation, can in turn drive further economic growth.

Especially for the Caribbean, which suffers from some of the highest energy prices in the world, the cost savings potential of geothermal energy offers attractive advantages. Geothermal boasts the same high capacity factor as oil or gas generators without relying on fuel, which makes the generated electricity cheaper over time. Despite higher initial capital costs, geothermal energy plants’ longevity, long-term affordability, and reliability could ease the Caribbean’s dependence on imported, expensive fossil fuels.

Fully harnessing geothermal energy could also bring co-benefits in the form of usable heat. Geothermal systems can support commercial and district heating, which is particularly valuable in Argentina, Bolivia, and Chile, which have significant winter heating needs. Chile is currently implementing district heating systems in its Patagonian region, where average year-round temperatures are as low as 6°C. There are health benefits to consider as well. Geothermal domestic heating is far better than burning firewood as in South-West Chile.

Latin America’s variety of industrial actors could also potentially harness geothermal heat. For instance, Costa Rica seeks to emerge as a key player in electrical component manufacturing, for which cheap electricity will help domestic producers compete with overseas manufacturers. Mexico similarly aspires to expand its automotive manufacturing industry. Despite their smaller size, Caribbean nations could also establish more manufacturing capacity and foster more domestic economic activity by adopting the right policies to lower regional electricity rates.

Ongoing geothermal energy efforts in Latin America and the Caribbean

Despite their massive geothermal potential, both regions have made relatively small progress deploying it to date.

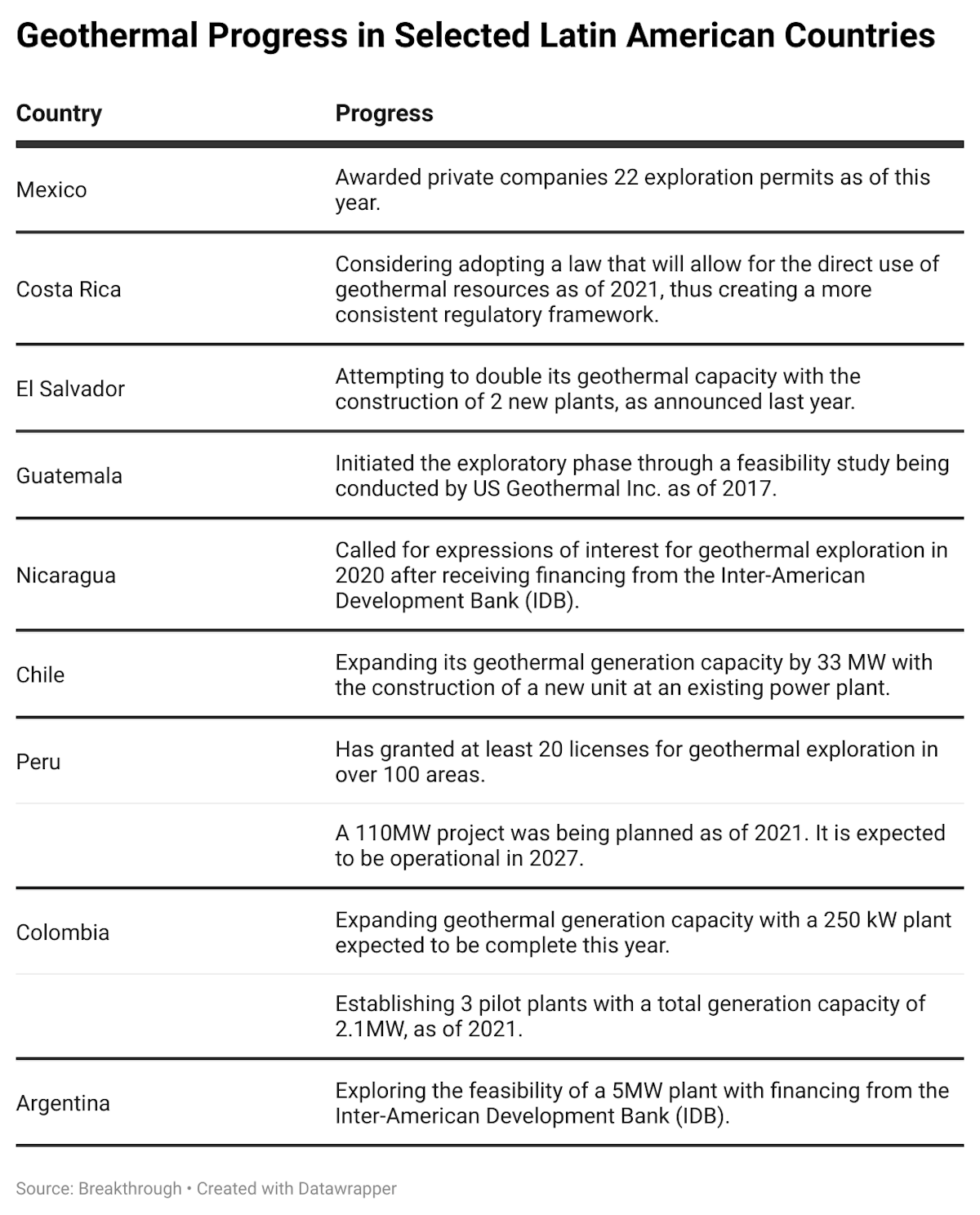

Mexico, for instance, is the leader in geothermal expansion in Latin America and ranks fourth in worldwide geothermal electricity production, yet it still taps only about 4-20% of its estimated geothermal potential (5000 - 25000 MW). Argentina, whose Renewable Energy Auction (RenovAr) program, a renewable energy program to encourage bidding companies to undertake clean energy projects at competitive prices, enjoyed great success, has yet to tap its geothermal resources, estimated at about 1.6 GW. Chile may possess one of the largest untapped geothermal reserves in the world at an estimated potential of 16 GW, but developers confront a lack of supporting public policy.

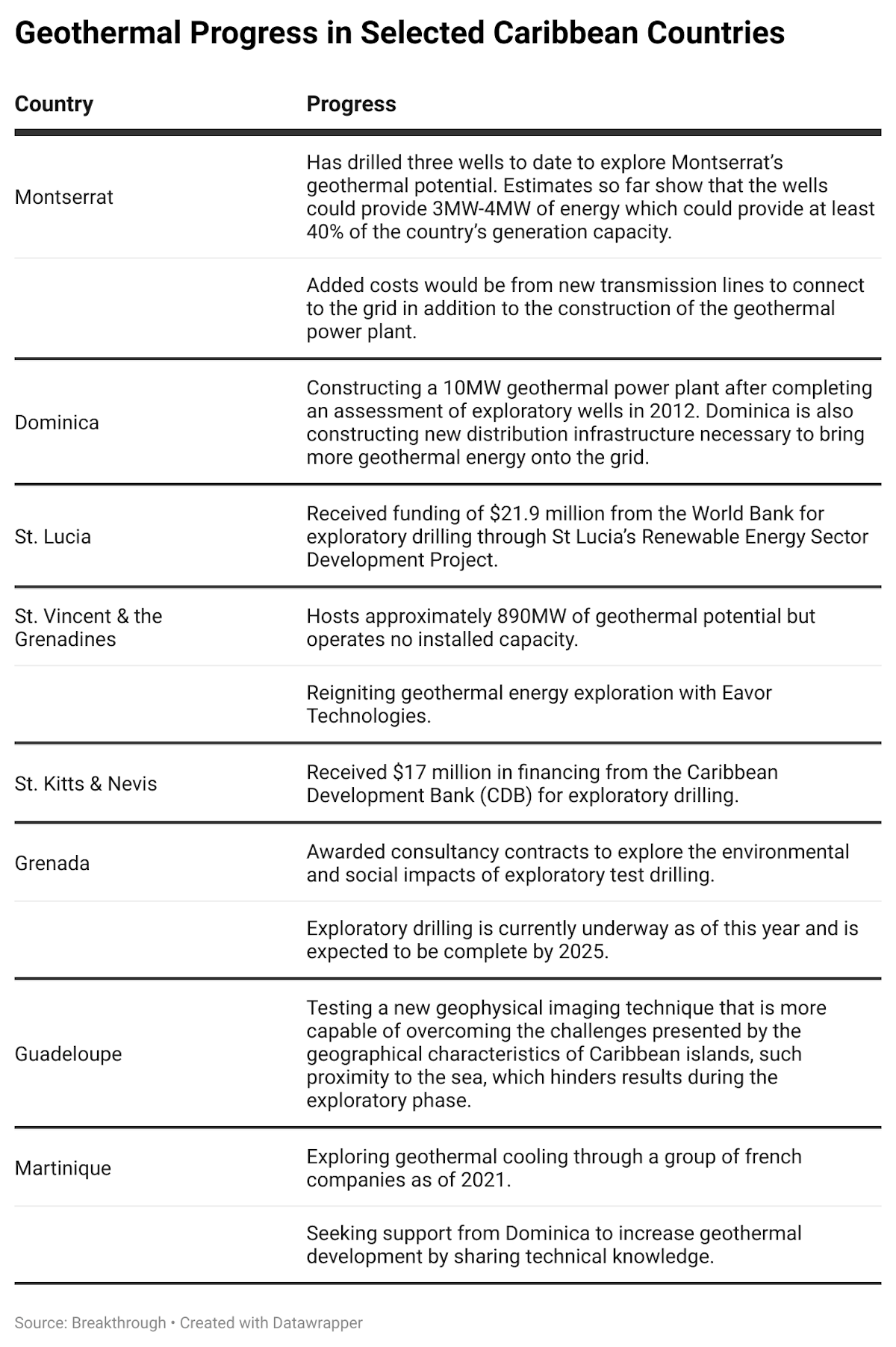

Meanwhile, Guadeloupe is home to the only operating geothermal plant in the Caribbean and will likely play a key regional role in sharing operational expertise with neighboring islands, especially as it seeks to take full advantage of its own geothermal potential with future expansions. Montserrat has already completed its exploratory drilling and is now exploring design and construction options for a 2.5-3.5 MW plant. St Kitts and St Lucia are in similar exploratory stages. Especially in the Eastern Caribbean, countries are in a prime position to take advantage of geothermal resources.

But none of these projects and installations is anywhere near its full potential.

To explain the relatively slow progress, geothermal industry observers generally point to the absence of policy support as a common weakness across Latin American in general, along with financial barriers that make accessing project financing difficult.

To make widespread geothermal energy adoption plausible, Caribbean nations will have to find ways to bring global and local costs down. Dominican officials have called on Trinidad and Tobago, which has decades worth of transferable skills from drilling oil and gas, to help lower the capital cost of geothermal production for Caribbean nations, potentially alleviating the need to import equipment and expertise from further corners of the globe. After the devastating effects of Hurricane Maria in 2017, Dominica is especially interested in using geothermal to build resilience against future climate impacts for its electricity grid.

Current Obstacles to Developing Geothermal Energy

For both Latin America and the Caribbean, unlocking geothermal energy regionally will depend on securing affordable capital and financing. Upfront capital costs—including expenses for the initial stages of exploration, drilling, and construction—can be massive. The overall costs for a geothermal plant can total around $1,870–$5,050/kW, with more challenging geography increasing development costs.

Another difficulty is risk for investors, with exploratory drilling requiring approximately 15% of the total investment costs upfront. Yet in the exploratory phase, there is a high degree of uncertainty that the geothermal source will be commercially viable.

To mitigate both the high upfront costs and the investment risk for governments and industrial actors, public-private partnerships represent a primary pathway toward financing geothermal energy.

Argentina’s RenovAr program is one example. It generously subsidies renewable projects then auctions those projects off to private companies with great success. But taking on so much of the risk and investment could be burdensome for countries already confronting high levels of debt, with Caribbean nations carrying debt levels averaging 90% of their GDP.

The World Bank administers a Global Geothermal Development Plan (GGDP) which has raised over $235 million in concessional funding to support upstream geothermal activities, while also offering technical assistance. Such concessional financing is essential for supporting geothermal project development in countries that may not be otherwise able to attract or subsidize low-cost investment. Already, Dominica, Nicaragua, and St. Lucia are preparing geothermal projects through the GGDP.

Next Steps for Promoting Regional Geothermal Energy Development

Latin American and Caribbean nations can promote geothermal development by developing clear supportive policy, seeking to decrease capital costs, expanding financing, and investing in a skilled regional workforce. A successful strategy will also leverage partnerships with countries that already operate successful geothermal plants.

Incentivizing Deployment of Clean, Firm Energy

Regional governments must recognize the difference between variable and firm, dispatchable clean energy sources—and the complementary roles each plays to support the other. Variable sources such as solar and wind energy can generate low-cost electricity, while firm energy sources ensure grid stability and provide long-term cost savings by facilitating the firming of variable generation.

Yet Latin American policymakers have not emphasized this distinction enough by rewarding firm, clean resources for their role in promoting a reliable grid and affordable clean energy. Nor have policymakers in the Caribbean, where governments have equated the region’s clean energy future solely with solar and wind energy. Creating policy to specifically deploy firm clean energy sources like geothermal will be key to supporting its development across both regions.

As a first step, more comprehensive electricity system modeling can quantify the total system cost savings of pairing geothermal with variable renewables and storage technology. Such research efforts could also include studies of geothermal reservoir thermal storage which could provide flexibility for meeting demand. Clearer regulatory and permitting systems can also encourage efficient progress.

Chile’s regulatory and permitting systems, for example, have several ambiguities that impede geothermal development. Charting a clear and concise regulatory pathway for development will be crucial for any country hoping to harness geothermal power. Finally, public sector incentives can encourage developers to enter the market in response to policies like tax credits and direct procurement of geothermal electricity.

Driving Down Capital Costs

Plans for geothermal expansion should include a focus on decreasing the costs associated with exploratory drilling. The development of enhanced geothermal systems (EGS) and of advanced drilling techniques can help lower costs. EGS extract geothermal heat by injecting water into rocks through their fractures and pores. The water then returns to the surface where it can be used. Advances in EGS have expanded the potential range of geographies in which geothermal projects could prove viable. Meanwhile, advanced drilling techniques have increased possible drilling depth and precision, including for horizontal and directional drilling.

Much funding for advancing geothermal over the past few years has gone toward these cost savings pathways. The U.S. Department of Energy (DOE) has recently announced that it will invest at least $15 million into projects seeking to reduce development costs by improving geothermal drilling speeds by 25%. The EU is similarly prioritizing drilling innovations as well, striving to quadruple drilling rates and reduce drilling costs by 65%. These efforts to spur innovation will undoubtedly benefit global geothermal project development over the long term, and policymakers in Latin America and the Caribbean should track future technical improvements closely.

Latin America and Caribbean governments themselves should also prioritize geothermal research efforts. Breakthroughs that enable more efficient drilling in regional geology, proactive regional surveying for commercially viable production wells, and gains from direct operational experience could drive significant cost savings over time. Participation in collaborative research initiatives such as the International Partnership for Geothermal Technology (IPGT) and the International Geothermal Association (IGA) can also allow countries to benefit from shared international expertise. Bilateral research collaborations can also prove valuable, with countries like Iceland and New Zealand having been instrumental in establishing geothermal industries overseas, including in the Philippines.

Increasing Development Financing and Risk Mitigation

Geothermal energy development will naturally require investment. Developing countries in Latin America and the Caribbean possess much less financial capacity, and may need to rely heavily on multilateral development finance institutions, like the World Bank and the Caribbean Development Bank (CDB).

Some promising efforts in this regard are underway. The World Bank is working with various stakeholders in Latin American and Caribbean countries to customize risk mitigation and financing strategies for each country.

St. Lucia, for instance, is using concessional financing for geothermal exploration in cooperation with the World Bank; the United Kingdom’s Foreign, Commonwealth, and Development Office; and the Climate Investment Fund (CIF). Last year, the CDB approved $17 million for geothermal development in Nevis. The bank also approved $27 million in financing to St. Vincent and the Grenadines to do the same. The CBD has specifically committed funds to assisting Eastern Caribbean states to develop their geothermal capacities. The Inter-American Development Bank (IDB) works together with the CDB to gather funds for geothermal financing, and it has its own dedicated financial portfolio for geothermal funding for member countries across Latin America and the Caribbean.

In countries with greater state capacity, public sector incentives can encourage investors, both domestic and foreign, to invest in domestic projects. Financial incentives could include allocated grants and investment tax credits for exploratory drilling, and production credits for geothermal plant operations. Specific incentives could target non-electric activities and co-benefits like heating and the extraction of critical minerals such as lithium. In particular, the potential for the extraction of critical minerals from geothermal fluid to reduce mining-related environmental impacts is increasingly gaining attention, with the United States, the United Kingdom and other developed nations seeking to develop direct lithium extraction technology for use in the global electric vehicle battery sector. Governments could also research the feasibility of retrofitting formerly operational oil wells for geothermal power production, which could save costs when constructing geothermal plants in former oil and gas producing regions.

Investing in a Skilled Regional Workforce

Governments must build up the domestic human resources and expertise needed to develop and maintain geothermal power plants. Doing so will involve investing in educational and training programs and leveraging existing human capital, including workers and techniques from the oil and gas industries.

The International Geothermal Association (IGA) has developed guidance on how best to apply knowledge from the fossil fuel industry to geothermal processes. Countries could also consider sending staff overseas to gain expertise and training from countries with a history of successful geothermal project development. For instance, the Philippines sent industry staff to geothermal training programs in Iceland to develop domestic expertise.

It is also essential to train public sector staff in navigating the legal and regulatory processes for funding geothermal development through multilateral donors. Knowledgeable and efficient staffers can help increase the ease with which countries can secure investment in geothermal development projects.