Advancing Nuclear Energy

Evaluating Deployment, Investment, and Impact in America's Clean Energy Future

-

-

Share

-

Share via Twitter -

Share via Facebook -

Share via Email

-

Executive Summary

Leadership in new nuclear technologies will powerfully benefit America’s energy future. Advanced nuclear reactors are versatile, reliable, long-lasting, land-efficient, resource-efficient, geopolitically secure, and scalable sources of clean energy. Bold investments in advanced nuclear technologies in the United States will advance technological innovation, secure US leadership in international nuclear markets, and support national energy security and electricity grid resilience, all while improving environmental health and accelerating US climate action.

However, forging a promising future for the domestic advanced nuclear sector will require increasing investment and policy support. Such efforts will generate far-reaching national benefits in both the near-term and long-term.

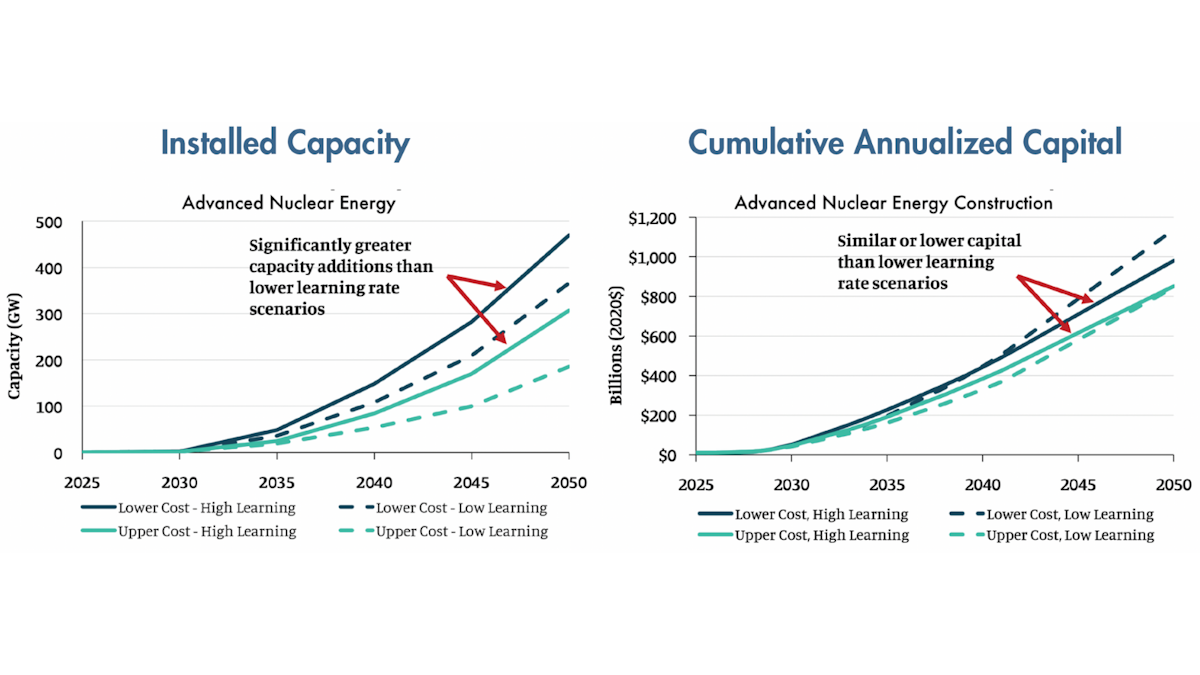

This report uses a high-resolution nationwide model of the United States electricity sector to demonstrate how advanced nuclear reactors might play a major role in a least-cost plan to transition the power grid entirely to clean energy sources by 2050, assuming that the first advanced reactors are available for deployment by 2030. A range of input assumptions were developed to encompass uncertainty in cost and learning rates to estimate the outer bounds of potential future deployment. Across these scenarios, the model chooses to deploy a large quantity of advanced nuclear power plants (Figure ES-1). Even in the case that first-of-a-kind advanced reactors are deployed at the high end of current cost estimates and benefit from very little technological learning as additional units are deployed, advanced nuclear captures a significant share of future electricity generation. This finding indicates that advanced nuclear energy technology provides important and extremely valuable benefits to the electricity system.

In particular, advanced nuclear reactors efficiently complement other clean energy technologies like wind and solar power, balancing out variations in generation over time to reliably meet US electricity demand. The flexibility of advanced nuclear power can produce long-term cost savings as America transitions to a clean energy system.

Advanced Nuclear Deployment and Capital Investment:

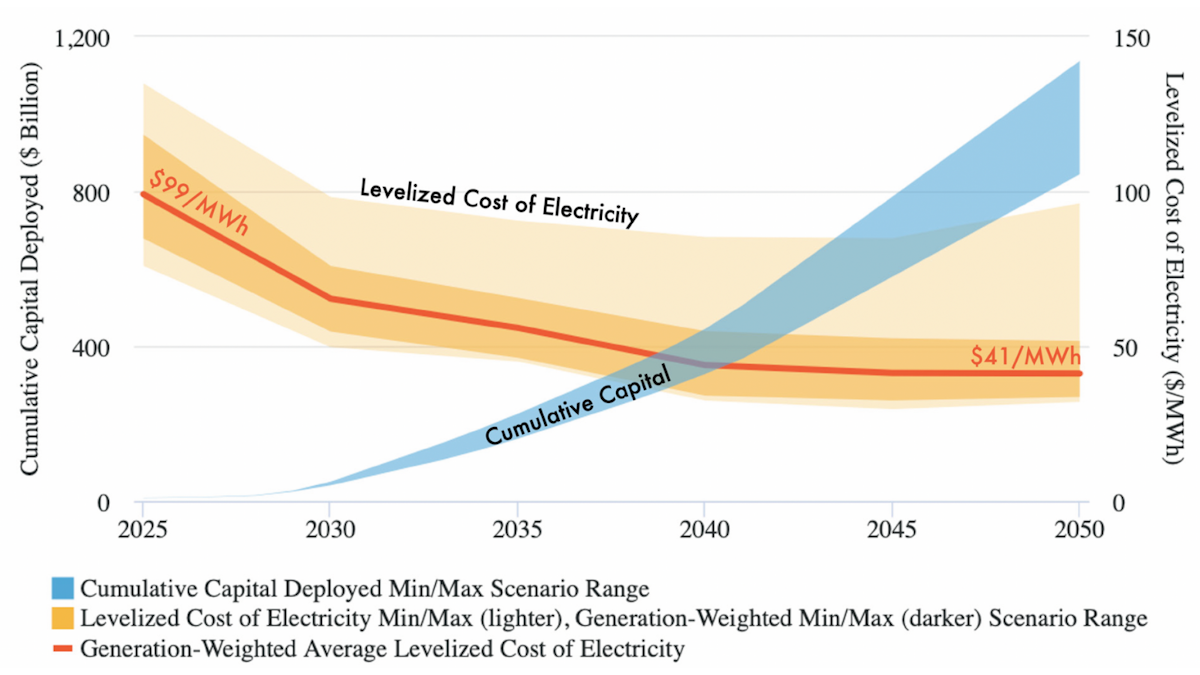

This modeling study shows that a US clean energy transition incorporating advanced nuclear energy could require cumulative capital investment for advanced nuclear power plant construction on the order of $150 to $220 billion by 2035, growing to a total of $830 billion to $1.1 trillion by 2050 (Figure ES-2). Early capital investment and learning-by-doing lead to substantial reductions in project costs and levelized electricity costs for advanced nuclear technologies, resulting in the large-scale nationwide deployment of new reactors.

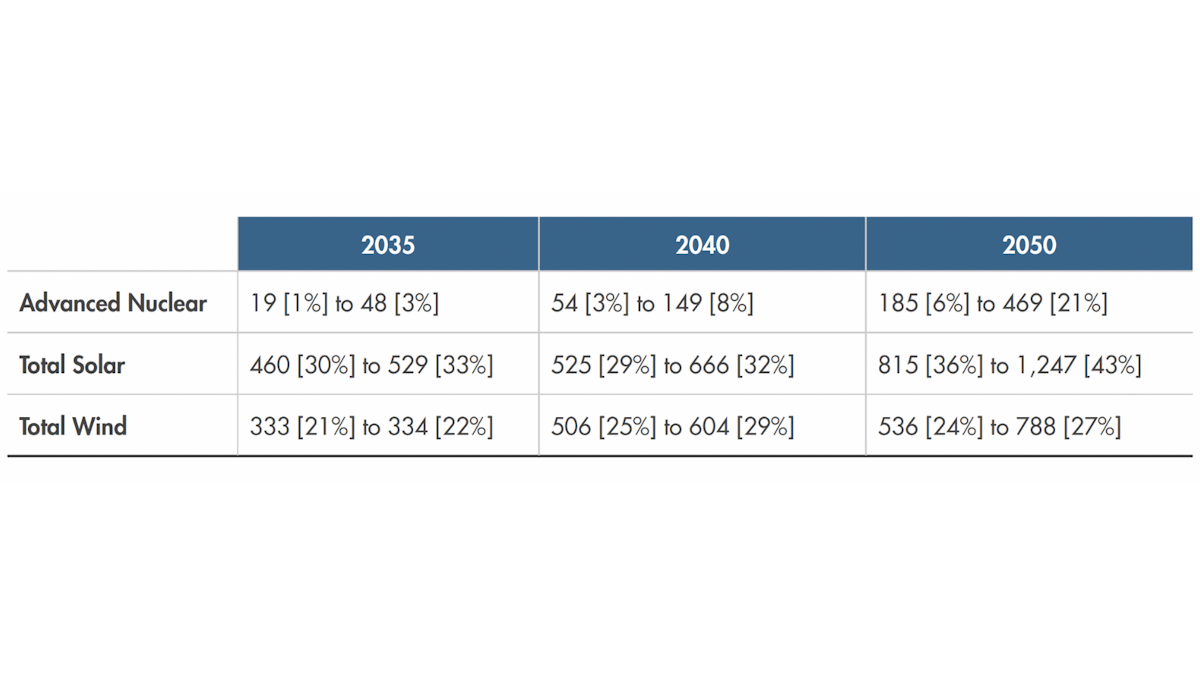

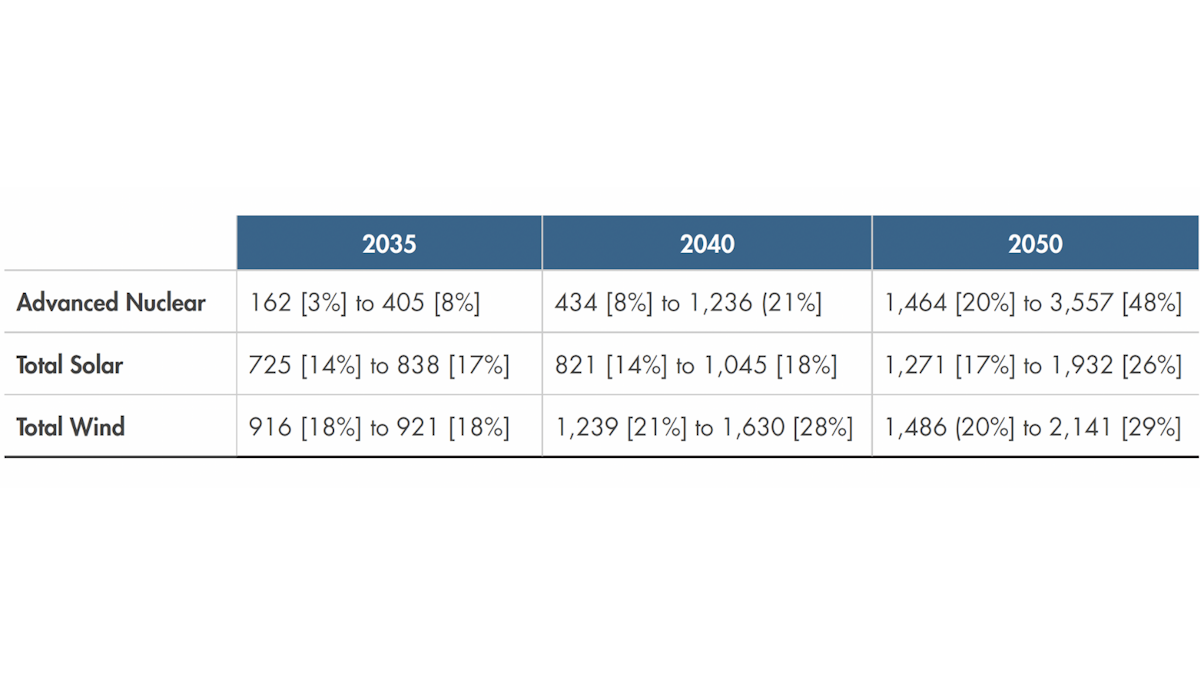

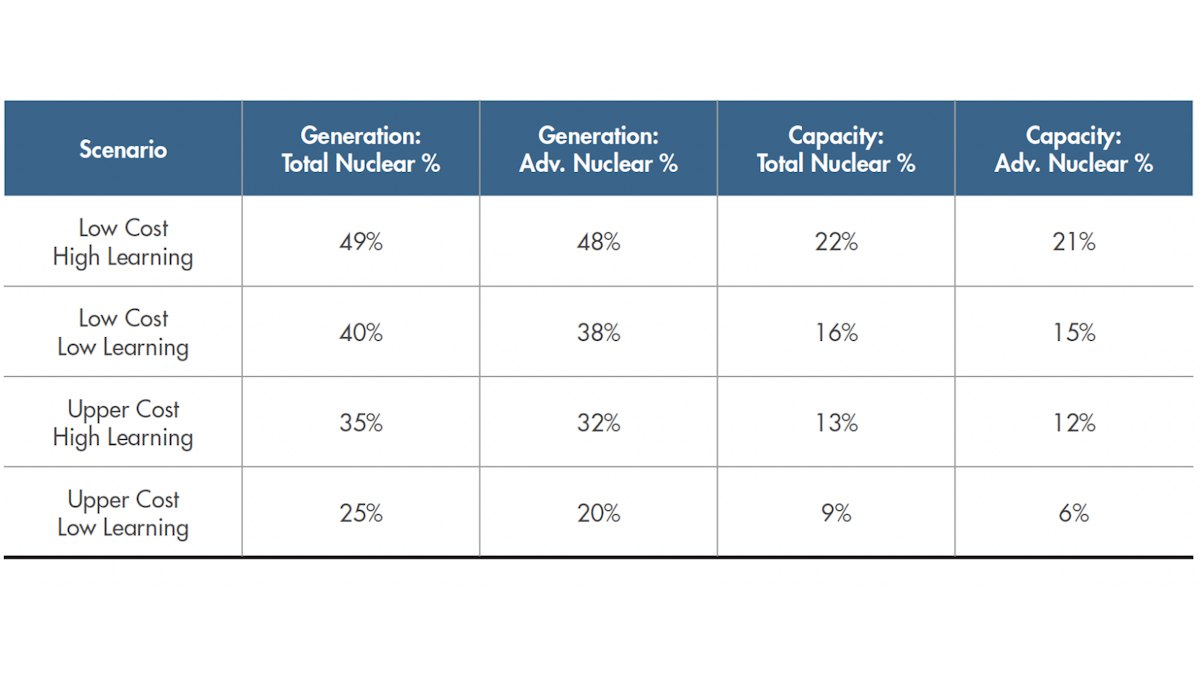

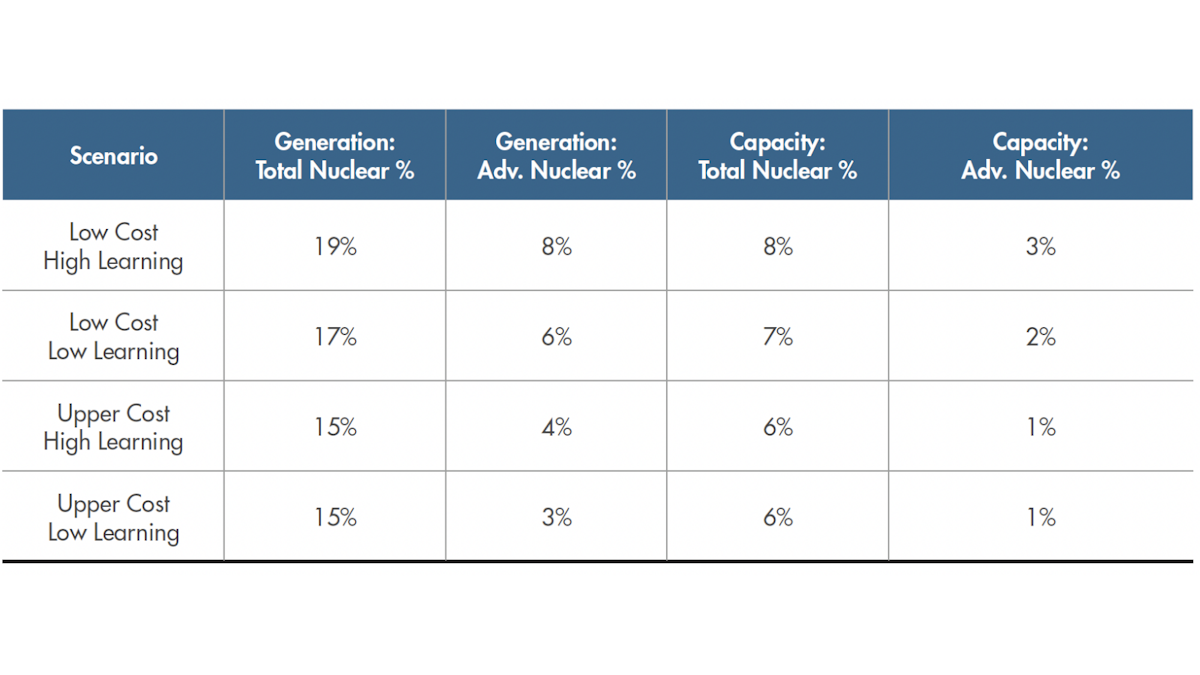

Widespread commercial deployment of advanced reactors in this study starts in the early-2030s and rapidly accelerates as the electricity sector grows over time, potentially supplying around 20-48 percent of domestic clean electricity generation in 2050, which would be 1,400 to 3,600 terawatt-hours per year (TWh/yr). Total domestic deployed advanced nuclear capacity reaches 19 to 48 gigawatts-electric (GWe) in 2035, reaches 54 to 150 GWe in 2040, and grows to 190 to 470 GWe by 2050.

Economic and climate benefits of advanced nuclear energy deployment potentially include the following:

- A United States clean energy transition pathway that incorporates advanced nuclear power can help reduce the costs of a future national clean energy system.

- Low-emissions heat and steam from advanced nuclear plants can supply reliable, clean energy for hard-to-decarbonize sectors such as heavy industry and chemicals.

- Clean advanced nuclear reactors can repower fossil-fuel power plants using readily available infrastructure, increasing economic investment, and promoting a just transition for local communities.

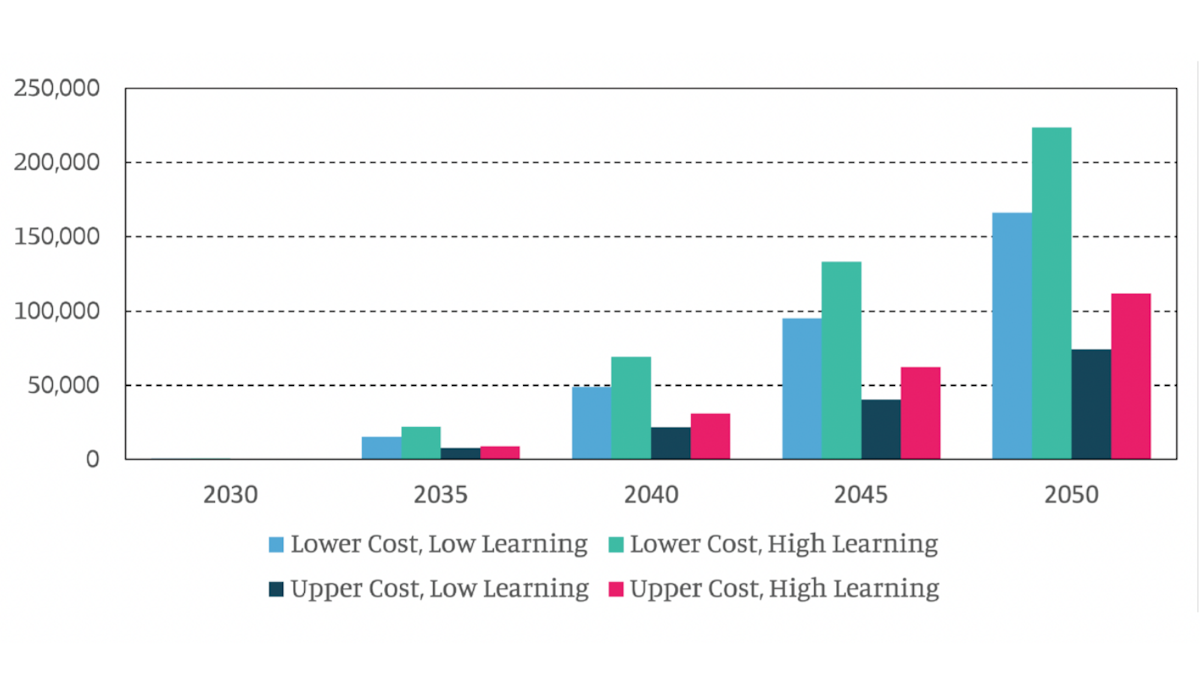

- A successful future nuclear sector will produce new job opportunities in the manufacturing, construction, operation, and maintenance of nuclear plants, creating between 74,000 and 223,000 permanent jobs in operations and maintenance by 2050 alone.

- Successful demonstration and commercialization of advanced nuclear power will competitively position the United States as a clean technology leader at a critical moment in the global clean energy transition.

Barriers to advanced nuclear energy deployment can potentially be overcome through the following:

- Immediate capital investment can enhance the potential for cost reductions and the total domestic market opportunity.

- Avoiding cost overruns on early projects and making cost improvements over time will increase the speed and magnitude of advanced nuclear deployment.

- Developing supply chains for fuel and component manufacturing is essential for the broad deployment of advanced nuclear reactors.

- New federal regulatory frameworks currently being formulated, and streamlining of existing rules, will be key to ensuring timely licensing and construction of new advanced nuclear projects.

- Lifting state-level moratoria and restrictions on nuclear projects will expand market opportunities and attract new capital investment to states that reform existing legislation.

Opportunities for public policy support include the following:

- Federal loan guarantees.

- Environmental impact pre-qualification and feasibility studies.

- Regulatory licensing modernization and fee reform.

- Technology-neutral clean energy tax credits.

- Inclusion of nuclear energy in state clean energy portfolio standards.

- Support for export of advanced nuclear projects.

Future Outlook:

Advanced nuclear reactors can play a key role in cost-effective decarbonization of the national power sector, reliably supporting a high-renewables energy system. Updated, realistic cost assumptions and accurate operational characteristics reveal that advanced nuclear technologies provide high value for a clean electricity grid and possess significant market potential. Emerging advanced nuclear technologies will ultimately compete in the marketplace based on cost, operating parameters, and the ability to meet diverse customer needs, shifting the balance among which technologies become dominant. Early advanced nuclear deployments may be most competitive or efficient for specific target markets and customers, including existing nuclear power sites, sites with retiring fossil fuel plants, remote or island communities, and military installations. As advanced reactor deployment expands, however, cost improvements over time, and the need for firm energy that provides the required operational characteristics can drive large-scale nationwide adoption in support of a wider affordable clean energy strategy.

For access to the appendix and references, please download the PDF version of the report above.

Introduction

We currently live in an era of rapid technological innovation across all domains of the global energy sector. A vast wave of reinvention is transforming every part of the modern energy system, from long-distance transmission to energy storage, from residential heating to power grid control. The remarkable recent progress in advanced nuclear reactor designs is one of the most exciting ongoing developments in the energy world, given their potential to not only generate heat and power safely, reliably, and flexibly but also produce this energy without emitting carbon pollution.

The term “advanced nuclear reactor” refers to a broad category of fission reactor designs that boast considerable improvements relative to current-generation nuclear technologies. These innovations can result in a high degree of inherent or passive safety, high reliability, improved efficiency, lower costs, more complete utilization of nuclear fuel, lower generation of waste, enhanced resistance to nuclear proliferation, and versatile applicability for the production of non-electric co-products like hydrogen, high-quality waste heat, and desalinated water. Some of these improvements can be linked. For example, smaller reactor designs offer safety benefits thanks to smaller fuel loads and more efficient cooling characteristics while also reducing costs by facilitating factory assembly and transportation to the project site. Other factors, such as the ability to safeguard spent fuel, vary based on the specific design. This report considers the category of advanced nuclear reactors to include smaller next-generation light-water fission reactors in addition to non-light-water fission reactors.

While numerous forms of clean electricity generation like solar, wind, and hydroelectricity are already widely deployable today, nuclear power offers a number of unique advantages that help complement and support the deployment of other zero-carbon emissions technologies, thereby strongly incentivizing future advanced nuclear projects.

First, nuclear reactors produce substantially more energy relative to their land footprint than solar and wind projects, which require over 30x and 100x the land area for the same nameplate generating capacity. With nationwide land requirements for renewable energy sources under some modeled future scenarios exceeding the area of West Virginia, land use and siting constraints may increasingly favor nuclear projects. Nuclear facilities can also be located more flexibly than renewable projects that depend on sun and wind conditions. Combined with the potential ability of new microreactors and small reactors to match the needs of a range of customers from rural and island communities to remote industrial sites like mines, advanced reactors have the potential to serve a more diverse set of markets than previous generations of large, centralized nuclear power stations. Nuclear deployments, if proactively planned, could thus help reduce system-wide costs for a clean energy transition by limiting excess transmission and new grid infrastructure that extensive wind and solar installations would otherwise require.

Furthermore, many advanced reactors under development are being designed for high compatibility with variable renewable generation, with desirable operating characteristics such as accelerated ramping of generation to balance fluctuations in renewable output and even thermal energy storage capabilities. Academic research suggests that pairing reliable, clean, firm electricity from sources like nuclear power with variable renewable generation makes planned transitions to clean energy systems more affordable.

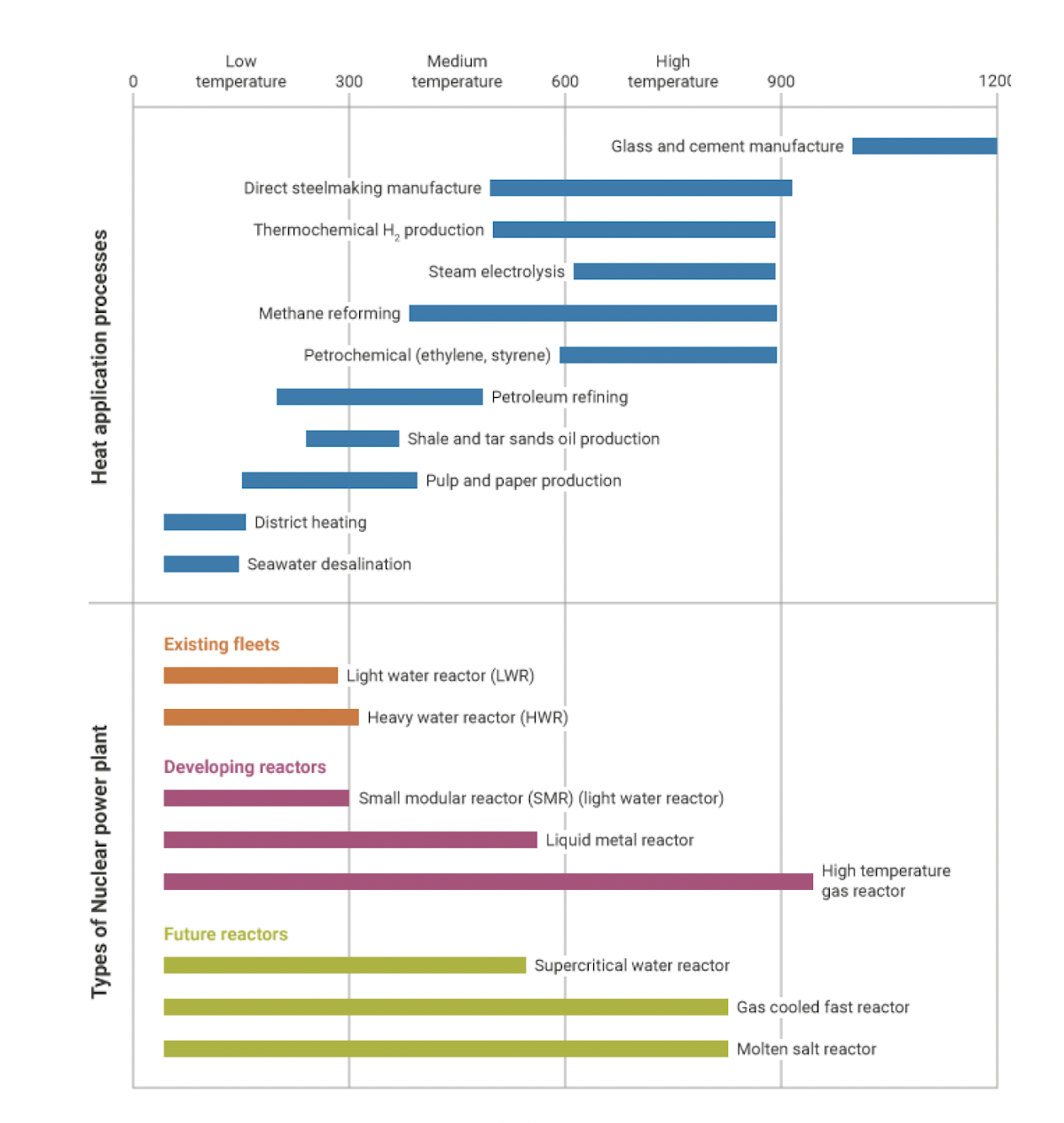

As an additional utility beyond that provided by solar and wind resources, nuclear reactors also generate useful heat and steam that can be utilized in industrial processes like desalination and hydrogen electrolysis. In comparison to traditional nuclear reactors, some advanced reactor designs can produce hotter outlet steam that can enable higher-efficiency hydrogen production from high-temperature water splitting and replace fossil fuel combustion in a wider range of industrial activities like petrochemical and cement manufacturing. Advanced reactors thus possess versatile nonelectric applications in industries well beyond the power sector.

Given the clear potential advanced nuclear technology offers, it is not surprising that numerous research groups and prospective vendors around the world are developing a range of advanced designs, with particular progress in China, Russia, the United States, Canada, and the United Kingdom. In a pair of 2020 reports, the International Atomic Energy Agency counted over 70 small advanced reactor designs and 12 advanced large water-cooled reactor designs worldwide in various stages of development. Notable small modular nuclear reactors to enter commercial operation include the two small pressurized-water 35MW KLT-40S units aboard the Russian floating nuclear power plant Akademic Lomonosov, officially commissioned in May 2020. In December 2021, the China National Nuclear Corporation commenced regular operation of the HTR-PM high-temperature gas-cooled pebble-bed reactor, a 200 megawatt-electric (MWe) unit sited in China’s Shandong province.

There are no advanced nuclear energy projects currently in operation or under construction in the United States, but several reactor designs are at various stages of licensing and regulatory approval. A growing number of initial planned projects have already been announced, including but not limited to the BWRX-300 project near Oak Ridge, Tennessee, and the Natrium project in Kemmerer, Wyoming. Estimated project completion dates typically lie in the late 2020s and early 2030s, with plans to expand deployment further upon successful demonstration.

Successful demonstrations and deployments of new advanced designs will rapidly accelerate progress towards widespread commercialization. Building a vibrant advanced nuclear industry in the United States will require sharp strategic planning. Industry stakeholders will need to proactively navigate policy obstacles, cultivate adequate fuel supply and manufacturing capacity, ensure sufficient capital investment, skillfully manage financial risks, and more. The process of recruiting, training, retaining, and growing the talent pool necessary to license, fabricate, assemble, operate and maintain next-generation reactors is both a challenge and opportunity for the advanced reactor sector.

Well-designed federal policies and programs can significantly facilitate the industry’s efforts on every front. At a time of deep division in Congress and the federal government, the deployment of new nuclear energy alternatives to fossil energy is one of the very few national priorities to enjoy appreciable bipartisan support. Consensus on Capitol Hill signals the urgency with which constituents expect their representatives and the Biden administration to reduce carbon emissions in the energy sector. To efficiently foster a domestic advanced nuclear sector, it will be essential for policymakers, investors, and industry to act in close cooperation with one another according to a rigorous, strategic plan for deployment.

This report seeks to describe, for policymakers and financiers, the key components that any successful advanced nuclear deployment plan will have to include. Using updated assumptions for advanced nuclear costs and cost improvements over time, this study modeled the evolution of the US power grid over the next three decades using the Weather-Informed energy Systems: for design, operations and markets-Planning Version (WIS:dom-P®) optimization model, developed by Vibrant Clean Energy, LLC (VCE®). The model evaluates the full energy system and designs a future net-zero CO2 power sector that meets demand at minimal cost.

This analysis finds considerable potential for advanced reactors to support future US electricity needs and climate progress. Inclusion of advanced nuclear designs among the available technology options for a clean energy transition leads to large-scale advanced reactor deployment as part of a least-cost pathway to a clean electricity future. However, the degree to which the United States can successfully develop an advanced nuclear energy sector over the next 15 years will crucially depend upon mobilizing sufficient capital investment and public policy support starting immediately from the present day.

The following chapters explain the high potential importance of advanced nuclear power to the future US energy sector and propose key investments, strategies, and policies that will help unlock the full potential of this emerging, promising, and powerful set of clean energy technologies.

Evaluating the Role of Technological Learning and Deployment for a Net-Zero Electricity Grid

1. Emerging Technologies and Technological Learning

New technologies are often expensive when first introduced, becoming increasingly cheaper, more affordable, and more competitive with time as more capacity is deployed. Indeed, one of the most encouraging clean energy triumphs of the past decade has been the rapid and dramatic reduction in the price of solar photovoltaic modules, wind turbines, and lithium-ion batteries. The cost of 1 megawatt-hour (MWh) of solar electricity or lithium-ion battery storage capacity has fallen by around 85 percent from 2010 to 2022. These shifts are already catalyzing fundamental changes in the electricity sector in many parts of the world. Worldwide solar capacity reached 707.5 gigawatts (GW) in 2020, growing 18 times relative to installed capacity at the start of the decade, while global wind capacity quadrupled over the same period.

However, full decarbonization of the power sector both globally and in the United States remains a long-term future goal that will require proactive planning and decades to achieve. A range of current and emerging clean energy sources will collectively work together in the effort to meet this objective. Clean, firm generating technologies like advanced nuclear reactors will complement wind and solar capacity, compensating for variable renewable electricity production, meeting demand in regions with low wind and solar resource potential, and alleviating other constraints such as land availability and transmission costs.

Advanced nuclear technologies will also likely experience cost improvements over the next decades as developers move from their first demonstration projects to successively larger waves of deployment. However, not all technologies necessarily become more affordable at the same rate. Researchers have long understood that, over time, costs evolve differently for different technologies based on numerous factors, and have employed concepts like learning rates and learning curves to analyze such trends.

A learning rate reflects the rate at which a technology achieves cost improvements as it becomes more established in the market. A learning rate of 5 percent for a generation technology, for instance, means that the capital cost of that technology decreases over time by 5 percent for every doubling of installed capacity. Over time, the falling cost of the technology can be graphed along a curve, referred to as a learning curve.

Technological learning rates for nuclear power have been studied extensively, with various estimates and results. A 2016 study calculated the overnight cost curve of nuclear power across time in seven countries. The costs of commercial nuclear plants increased dramatically from approximately 1965 to 1975 in the United States, and increased slightly in France from 1970 to 1990.

Whereas the increasing affordability of technologies like batteries and semiconductors has demonstrated the success of large-scale learning-by-doing, recent efforts to reduce nuclear energy costs through mass deployment have encountered setbacks. In recent decades, prominent conventional nuclear projects in Western countries like Olkiluoto-3 in Finland and Vogtle units 3 and 4 in the United States have experienced marked cost overruns and construction delays. A handful of earlier studies of the increasing nuclear construction costs in the United States and France even alleged negative learning rates for traditional nuclear plants. ,

However, escalating conventional nuclear costs may reflect poor planning, engineering, and policy frameworks rather than inherent technological factors. A comprehensive global analysis of nuclear power plant construction costs for plants built around the world between 1954 and 2015 (from which the increased costs mentioned above are drawn) found that many national nuclear programs exhibited considerable cost improvements during the early phase of nuclear deployment. Other nations like Japan experienced very limited cost escalation, with nuclear builds in South Korea even achieving cost declines. While costs of nuclear projects in China are unclear, the Chinese government has pursued an aggressive buildout of conventional nuclear over recent decades, with the majority of builds completed after 2000 requiring between five and seven years for construction.

When researchers reviewed the literature on nuclear learning rates they found estimates of learning rates that varied from -49 percent (rising costs with time) over cumulative national nuclear deployment, to +11 percent (falling costs over time) for projects constructed in series by the same firm. , All six studies that included a specification to control for the same construction firm found a positive learning rate using US data, indicating that costs of reactors from the same firm may have declined from learning, internal to the firm, even as national nuclear costs escalated. This may provide evidence that serialized and standardized construction of nuclear plants, as is often proposed by advanced nuclear developers, could lead to significant positive learning and cost declines over time.

With a new generation of nuclear technologies now poised for deployment, historical nuclear cost patterns may no longer serve as an appropriate basis for projecting the future competitiveness of nuclear power. Multiple studies have used bottom-up models to estimate potential learning rates for advanced nuclear technologies. For small modular reactors (SMRs), five of the six studies estimated positive learning rates, ranging from 3.4 percent to 16 percent across studies and scenarios. In 2022, Stewart and Shirvan estimated a 16 percent learning rate using a bottom-up model that estimates costs of factory build, labor, and materials, in addition to deriving estimates from the cost record of relevant technologies like natural gas turbines, wind turbines, and small airplanes. Their study concludes that while first-of-a-kind (FOAK) costs may be significantly higher than conventional nuclear costs, the accelerated learning that is enabled by modularization and novel technology could result in significant cost declines. Furthermore, by reducing the total hours of labor required, advanced reactors could avoid the risk of cost overruns that have been associated with labor-intensive megaprojects. Reducing the risk associated with project size and labor requirements could make advanced nuclear a more attractive investment for utilities, policymakers, and financiers.

1.1 Prospects of Advanced Nuclear for Achieving High Learning

In technical aspects, advanced reactors represent a sufficient departure from traditional light-water reactors of previous generations that they may exhibit improved learning rates. At the same time, advanced nuclear designs may be able to achieve a relatively more rapid pace of commercial deployment, enabling these technologies to benefit more quickly from cost reductions.

Broadly, the advanced nuclear industry is seeking to shift nuclear manufacturing and construction into a process more akin to building “airplanes not airports”. More modular reactor units can be more easily factory-manufactured, without as extensive requirements for expensive heavy forging of components. A smaller reactor will also reduce construction time, while enabling more standardization and simplification in balance-of-plant infrastructure. Some modular advanced nuclear designs are intended to be manufactured in a central facility, then transported to the site of installation in a “hub and spoke” production model. Units could even be returned whole to the manufacturer following retirement, simplifying the decommissioning process and reducing end-of-life costs. Smaller designs also allow advanced reactor vendors to scale projects modularly to compete in a wider array of applications, potentially increasing demand and driving faster rates of deployment and learning.

Aside from the supply chain advantages offered by moving towards reactor units a fraction the size of conventional light-water nuclear plants, advanced reactor concepts also possess inherent characteristics that may drive lower costs. For instance, advanced designs that are capable of passively self-cooling for weeks in the event of a loss of onsite power may require less backup generating infrastructure. New nuclear technologies that operate at normal atmospheric pressure may not require the specialized reactor vessels and sophisticated systems of pumps and valves needed to maintain higher pressures in, say, a traditional pressurized water reactor.

In general, modular advanced reactors feature much more streamlined design principles, with fewer complex parts and a reduced need to maintain multiple, intricate, redundant systems. Stewart and Shirvan’s study concluded that small reactor designs in particular could benefit from five factors that could lead to accelerated learning and reduced costs: 1) deployment of many units at the same site, 2) serialized factory manufacturing, 3) shortened construction time, 4) design simplification of plants, and 5) increased flexibility of deployment to maximize system value.

A 2018 study concluded that the costs of materials like concrete, steel, and nuclear fuel have not been major cost drivers of nuclear plants; instead, design, labor, and project management have been significant determinants of construction costs. In particular, high-cost plants often: do not have completed designs at the time of construction start, experience significant regulatory interventions during construction, have a FOAK design, encounter litigation between project participants, have a long construction schedule, and have high labor rates and high labor hours invested. Since many of these factors could potentially be addressed by serialized deployment of advanced nuclear technologies, we attempt to model the potential learning achievable by advanced nuclear deployment in our modeling analysis.

1.2 Approach for Modeling Advanced Nuclear Costs and Potential for Learning

This study assesses the scale of public policy support and capital deployment needed to drive the successful deployment of advanced nuclear reactors at scale in the United States, and provides insight into a least-cost energy system that incorporates advanced nuclear power to achieve a net-zero power sector.

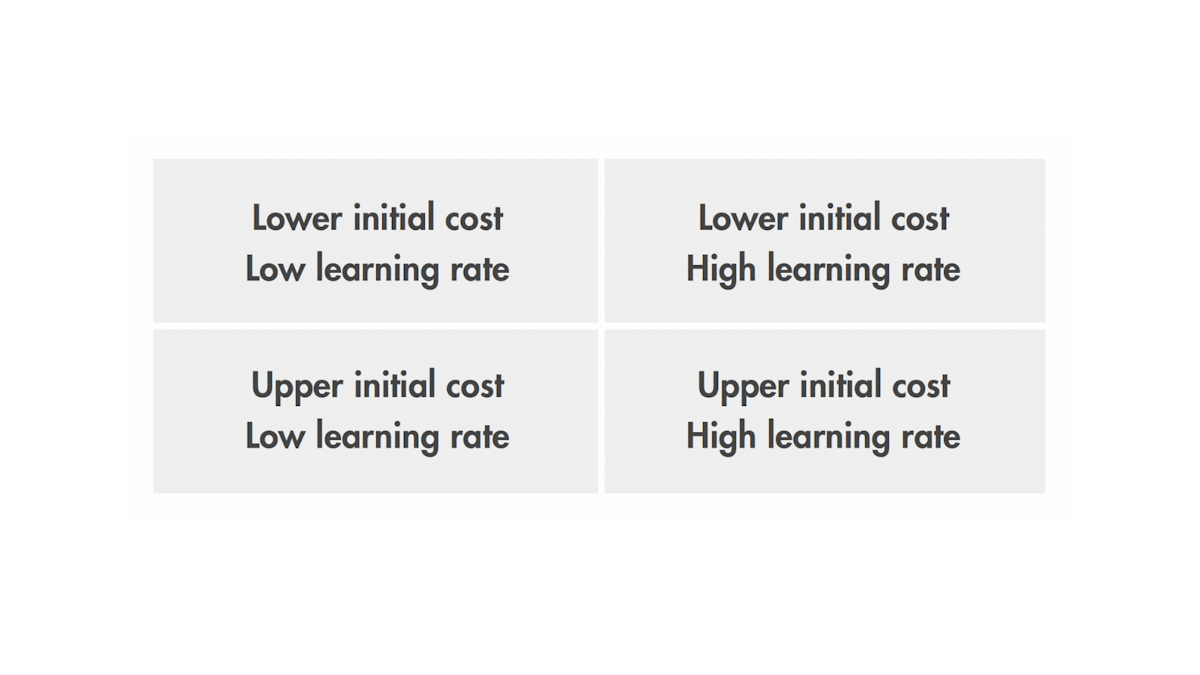

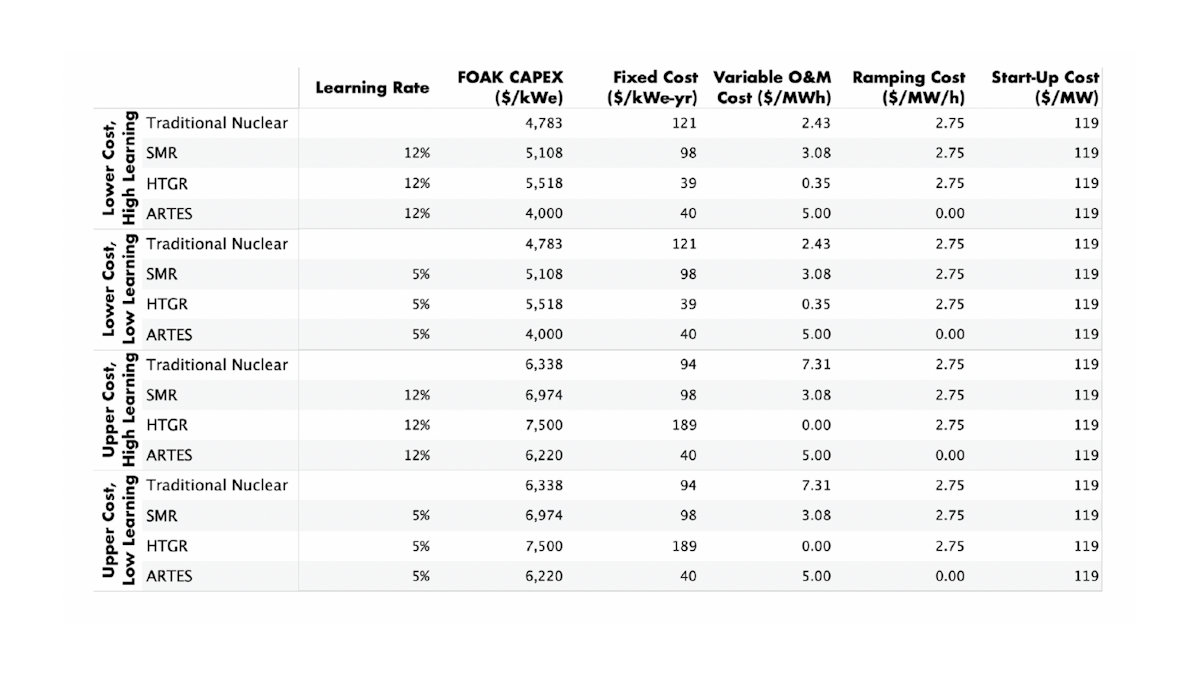

Recognizing the uncertainties around future learning rates and construction costs of advanced nuclear, we use a range of assumptions for learning rates and FOAK costs that are grounded in the literature. The four scenarios in the modeling results that follow are distinguished by “high” vs. “low” learning rates and FOAK cost inputs (Table 1-1). For a detailed summary of study assumptions and methods, see Appendices A and B, respectively.

Cost Reduction Due to Learning

To reflect learning over time, other studies have generally incorporated pre-determined cost reductions over time for energy technologies like solar photovoltaic (PV), wind, nuclear, natural gas with carbon capture and storage (CCS), and other clean energy sources. Improving over this prescribed approach, our study utilized a dynamic endogenous approach to modeling advanced nuclear reactor deployment costs. This approach updates the capital costs of advanced nuclear technologies based on a scenario-specific learning rate to reflect improvements as the model independently deploys reactors over time. Further discussion of learning calculations is included in the methods section in Appendix C.

An imposed capital cost floor for all three advanced nuclear technologies was set at $1,800 per kilowatt-electric (kWe). In addition, we initialize learning in the model by hard-coding a set of advanced nuclear demonstration projects already announced, funded, or otherwise planned. The projects include demonstrations of all technology types, and the model is restricted from building any non-demonstration advanced nuclear projects before the end of 2028.

Learning Rate Selection for Scenario Development

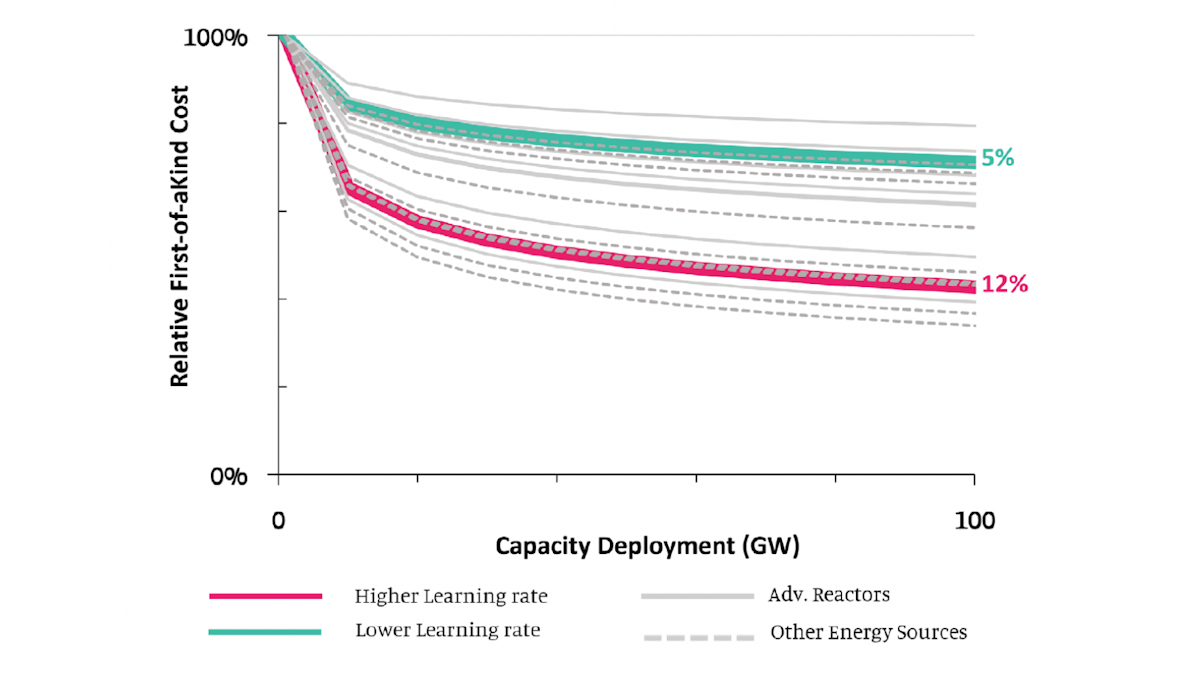

This study uses learning rates of 5 percent (Low Learning) and 12 percent (High Learning) based on the estimates of advanced nuclear learning discussed above to effectively provide bounds on the potential impact of learning (Figure 1-1). For comparison to other energy technologies (see Appendix B), a learning rate of 5 percent approximates the empirical learning rate of coal-fired power plants, while a learning rate of 12 percent approximates the empirical learning rate of wind power installations.

Costs for First-of-a-Kind Projects

Estimates of FOAK capital costs for advanced nuclear technologies were collected from the academic literature, national laboratory studies, and proprietary private sector estimates. For the purposes of this study, we examined three technological categories of advanced nuclear reactors: light-water SMRs, high-temperature gas-cooled reactors (HTGRs), and advanced reactors with thermal energy storage (ARTESs). These three categories of advanced reactors are not comprehensive, but reflect many of the design types slated for deployment over the next decade in the United States. Input values are derived from multiple sources to represent the technology class and do not reflect a single design. As used in this report, the ARTES design has many of the characteristics of liquid-metal or molten-salt fast reactors, but thermal storage can be used with most nuclear reactor types.

Certain fixed and variable costs—which remain static throughout the duration of the model—were also adjusted across the two Upper Cost and Lower Cost scenarios. Importantly, conventional nuclear does not undergo endogenous learning in this model as it is a well-established technology. Instead, in Lower Cost scenarios, an assumed lower bound capital cost for conventional nuclear plants is held static over the course of the model. Meanwhile, in Upper Cost scenarios, a prescribed cost reduction for conventional nuclear power is assumed in accordance with the National Renewable Energy Laboratory (NREL) moderate Annual Technology Baseline (ATB) projection. NREL ATB 2021 is the most recent version available and is used in this study. Table 1-2 summarizes the input cost assumptions and assumed learning rate regimes for advanced and conventional nuclear energy in all four modeled scenarios. Further details regarding model settings and assumptions appear in Appendix A.

Nuclear Technology Input and Learning Assumptions Across Scenarios

1.3 Operational Characteristics

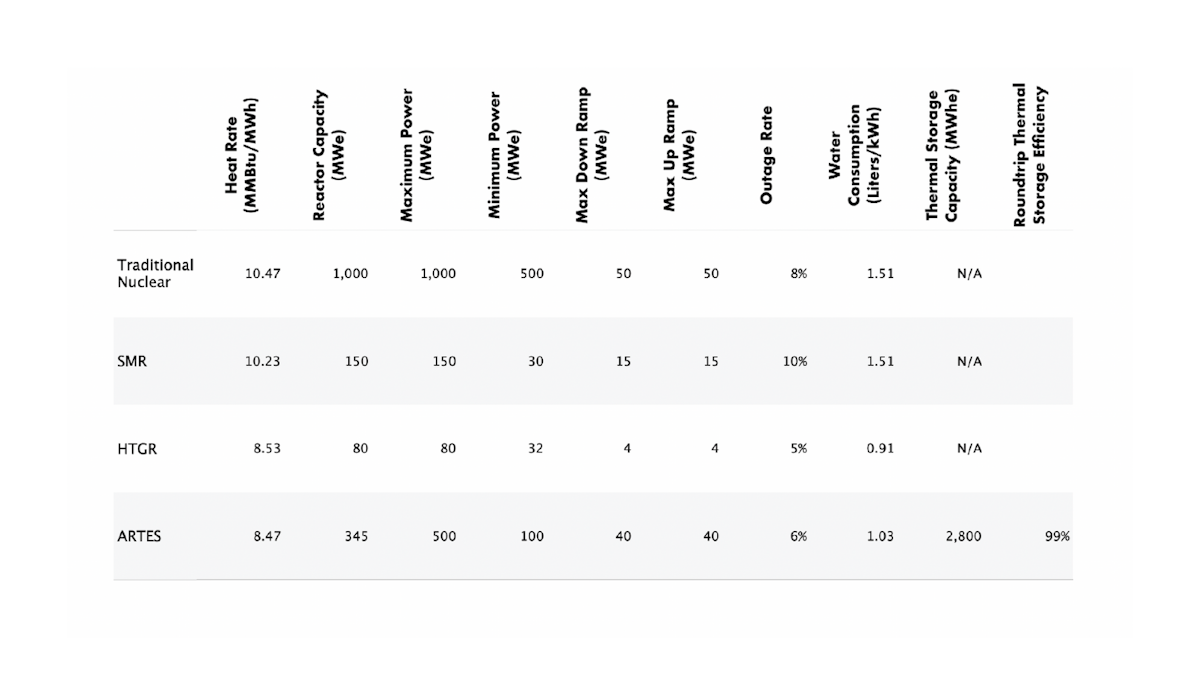

In addition to initializing FOAK capital costs and gathering fixed and variable nuclear cost assumptions, this study applies technology-specific operational characteristics that affect grid service capabilities, siting, and more. Table 1-3 presents these input characteristics, including heat rate, template reactor capacity size, maximum power output to the grid, minimum operational power output, maximum up and down ramping capabilities, liters of water consumption per kilowatt-hour (kWh) of electric energy generated, and, for ARTES, the electric energy equivalent of thermal storage capacity and roundtrip thermal storage energy efficiency. Maximum output is considered to be the same as reactor capacity except for ARTES.

Nuclear Technology Input and Learning Assumptions Across Scenarios

These detailed operational characteristics for advanced nuclear reactors alongside the above mentioned input cost and learning assumptions served as inputs to the WIS:dom-P model to investigate how the United States electricity sector changes in order to achieve decarbonization by 2050 at the lowest feasible cost for the utility-scale power sector. These operational data and bounding cost and learning assumptions reflect the latest literature and do not inherently favor advanced nuclear technologies over other clean technology options. At the same time, this approach represents a progression relative to other energy system studies that typically only rely on specifications and future cost projections for large light-water conventional reactors to model nuclear power.

Establishing a cautiously bounded playing field for emerging nuclear technologies allows the range of roles that advanced nuclear power might play in tomorrow’s clean electricity grid to be fairly assessed. The next section summarizes this modeling study’s key findings and discusses their implications for the future US energy system.

2. A National Clean Electricity Grid by 2050

This study uses multiple input scenarios to model a future electricity system that reaches 99 percent decarbonization by 2050. The multiple input scenarios result in a range of energy source mix and structure.

2.1 Power Sector Mix and Structure

Capacity Expansion Modeling Results

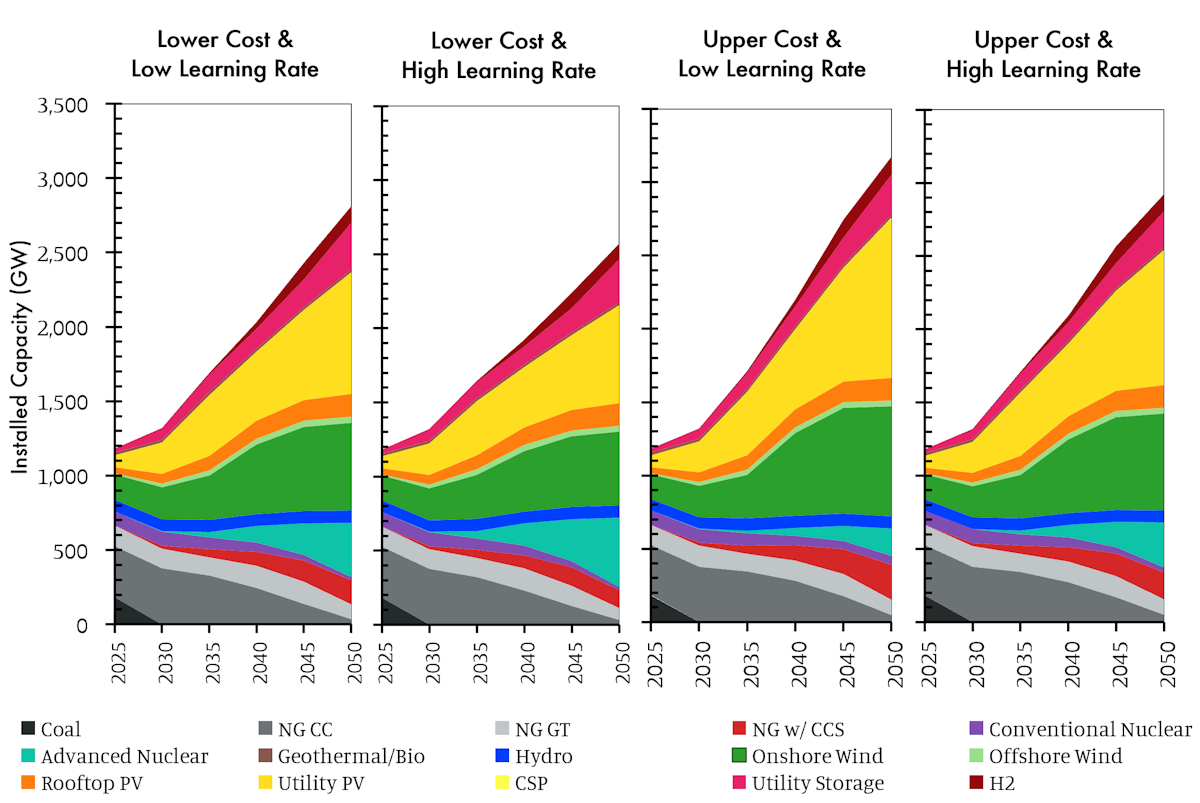

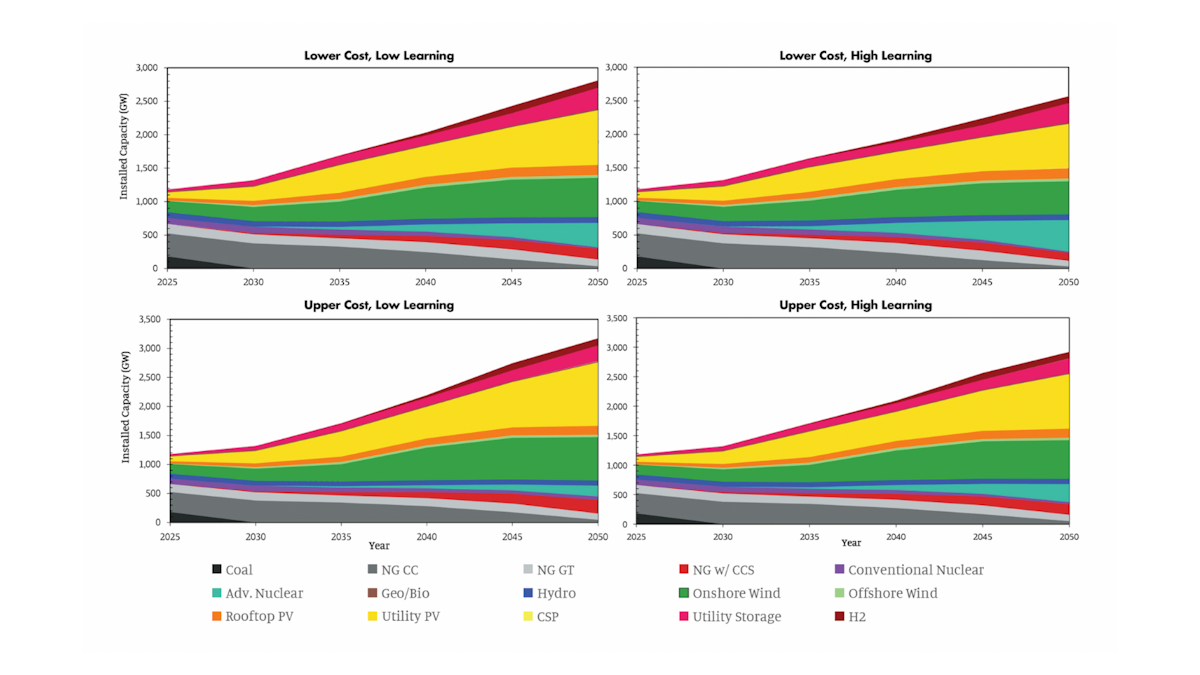

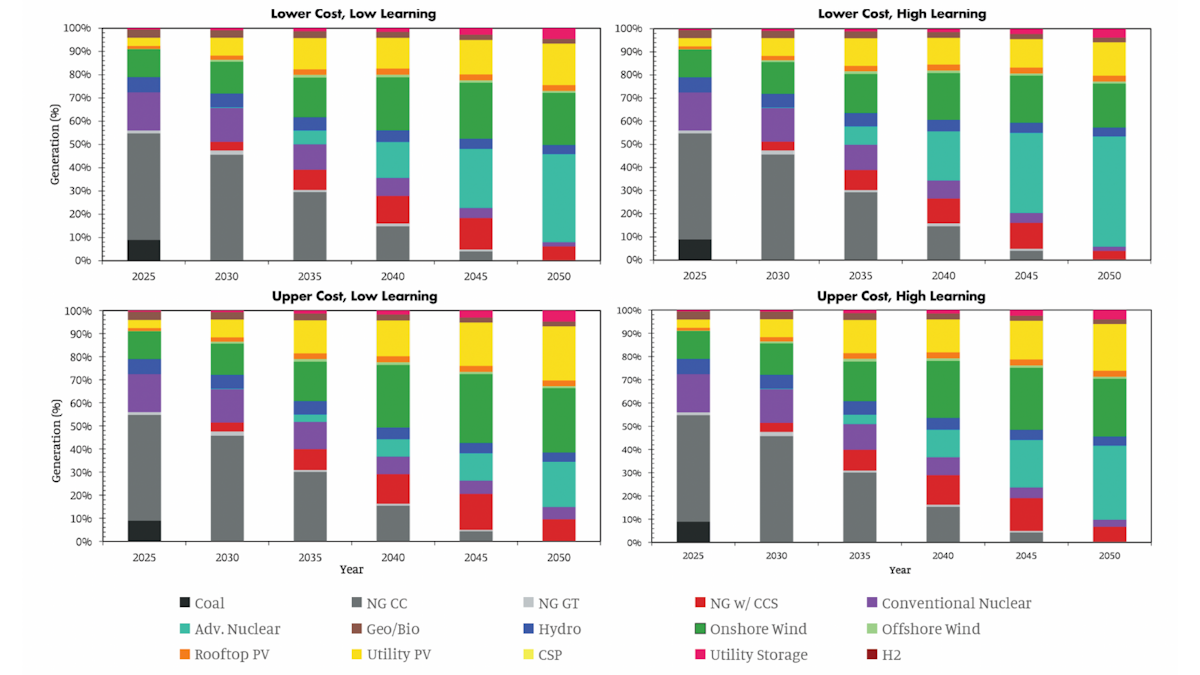

By 2050, the US power sector landscape primarily consists of renewable and nuclear technologies in these model runs (Figures 2-1 and 2-2). Both installed generation capacity and total generation grow considerably in the next three decades over the course of the four scenarios. Installed capacity more than doubles, increasing to around 2,500 to 3,000 GWe by 2050. Total nationwide generation grows from 3,900 TWh in model year 2020 to 7,400 TWh in 2050.

Installed Capacity

Renewable energy grows across all scenarios, dominated by onshore wind and utility-scale solar photovoltaic (UPV) installations. The shift to low-carbon technologies results in the retirement of coal generation by 2030 in all models, as well as the gradual diminution of natural gas generation and capacity. Ultimately, only natural gas combined cycle plants with carbon capture and storage (NGCC+CCS) are in operation by 2050.

Advanced nuclear technologies increase across all scenarios, with significant deployment beginning in 2035. By 2050, advanced nuclear power annually generates a comparable amount of electricity to utility-scale solar farms in the Upper Cost scenarios. In the scenarios with lower initial advanced nuclear capital costs, advanced nuclear plants produce a comparable amount of national electricity as utility-scale solar and onshore wind installations combined.

Utility-scale electricity storage and distributed rooftop solar PV capacity both increase steadily throughout the next three decades. Meanwhile, the proportion of US electricity generation from hydroelectric stations declines modestly. Traditional nuclear power also plays a progressively smaller role in the energy mix through 2050 due to high capital and operational costs and plant retirements.

Electricity Generation

Only late in the Upper Cost, Low Learning scenario does conventional nuclear exhibit a total net increase in nationwide capacity, expanding from 57 GWe in 2045 to 62 GWe in 2050. This deployment is driven by the combination of higher capital costs for advanced nuclear (this scenario represents the most conservative bounding scenario for advanced nuclear capital costs and cost reductions) and the constraining requirement that the model decarbonizes by 2050. In the two Upper Cost scenarios, especially in the Upper Cost, Low Learning scenario, traditional nuclear sees an uptick in new deployment in several states.

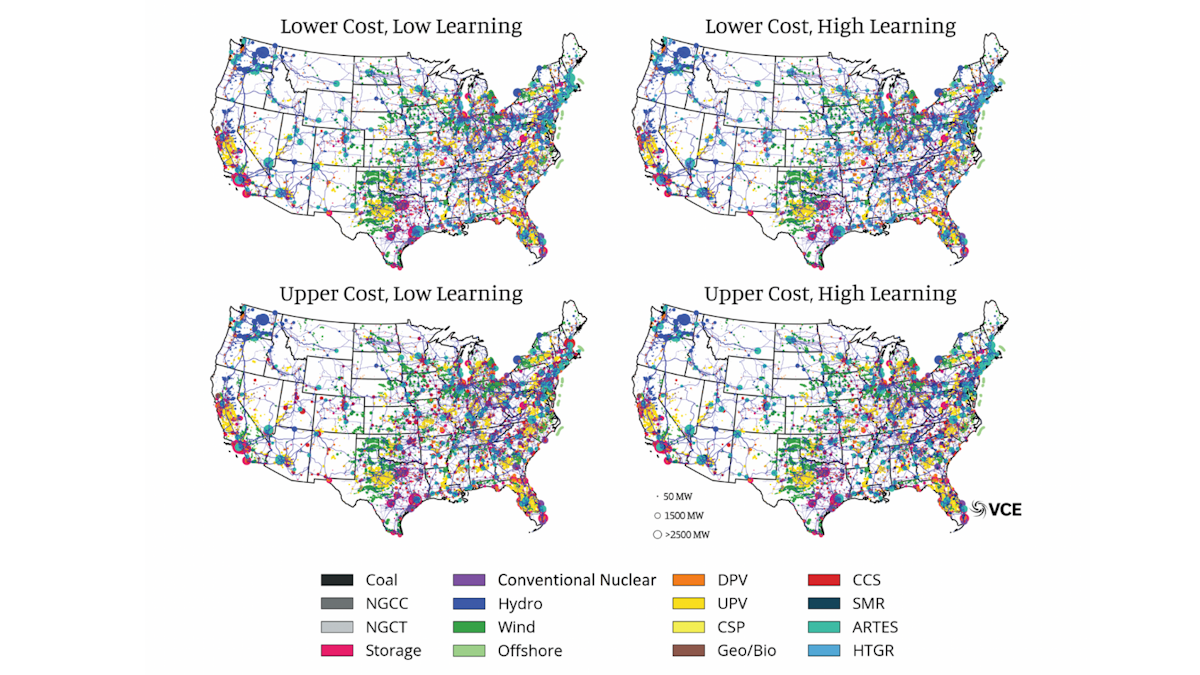

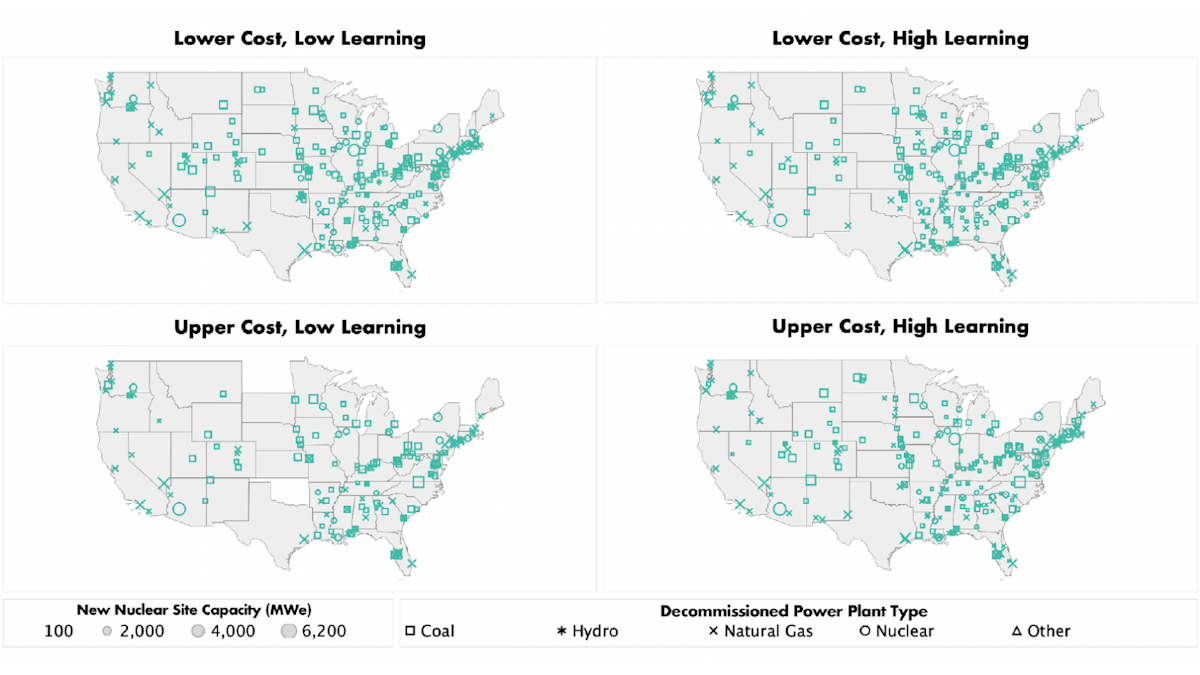

Geographic Distribution of Capacity

The WIS:dom-P model deploys new power sector infrastructure at specific geographic sites with county-level granularity at minimum, based on factors such as competing land uses, renewable resource quality, cooling water availability, and existing transmission networks. Some differences in siting decisions occur between the four scenarios due to differences in advanced nuclear capital costs and cost improvements over time. Overall, however, patterns of capacity installation over the next three decades are geographically similar for all scenarios.

Across the four model scenarios, by 2050, a cumulative land area of 17,500 to 28,800 square kilometers (1.75-2.88 million hectares) nationwide is directly occupied by wind turbines and utility-scale solar projects, as well as associated roads and infrastructure. This direct land usage ranges between the combined area of Connecticut and Rhode Island and the total area of Massachusetts. When indirect land use including the land surface surrounding solar modules and wind turbines is taken into account, a total cumulative land area of 182,000 to 277,000 square kilometers (18.2 - 27.7 million hectares) nationwide is occupied by wind and solar farms.

New advanced reactor projects are distributed broadly across the continental United States by 2050 (Figure 2-3). Large facilities are generally concentrated near major load centers such as across the eastern coastal states between Washington, DC, and Boston, the Great Lakes region, and the Pacific Northwest. Sizable advanced nuclear power stations are also situated near Houston, Los Angeles, Las Vegas, and Phoenix.

Utility-scale solar and onshore wind farms are numerous throughout the country. Particularly sizable concentrations of utility solar PV generation are deployed in California and Texas and throughout much of the midwest, southeast, and mid-Atlantic regions. Onshore wind capacity is prevalent across the Great Plains, the Midwest, and Texas. Moderate amounts of offshore wind capacity are installed along the Atlantic coast between North Carolina and Massachusetts.

Installed Capacity in 2050

Interestingly, across all scenarios, traditional nuclear sees a modest resurgence of new deployment in Florida between 2040 and 2050. The Pacific Northwest continues to generate a large proportion of regional electricity from hydropower. Finally, large utility-scale energy storage facilities follow a siting pattern somewhat similar to advanced nuclear plants, with sizable deployments in urban areas of California, Texas, Florida, and the Eastern seaboard.

Load Profiles and Grid Dispatch

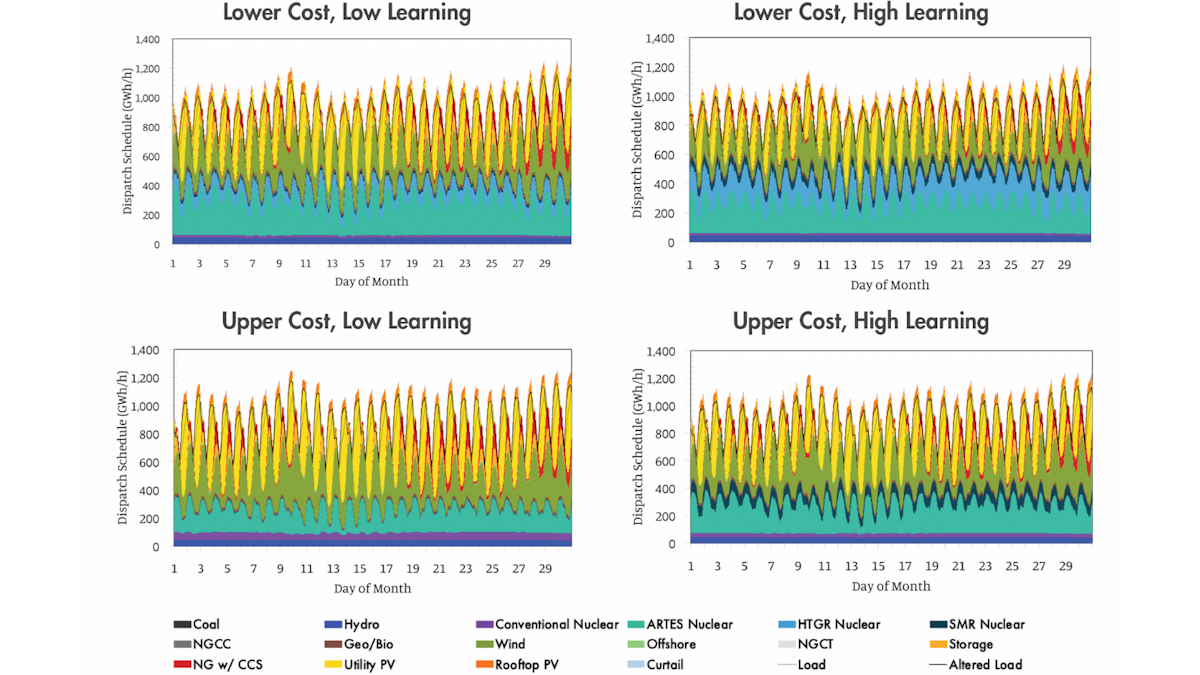

A distinguishing aspect of this study and a powerful feature of the WIS:dom-P model is its exceptional level of temporal detail in assessing grid dispatch, at up to five-minute intervals. Importantly, this enhanced temporal resolution provides additional advantages compared to modeling dispatch at a coarser hourly interval. This feature allows for a high confidence that available grid supply consistently meets demand and ensures continued reliability even as variable renewable energy generation expands.

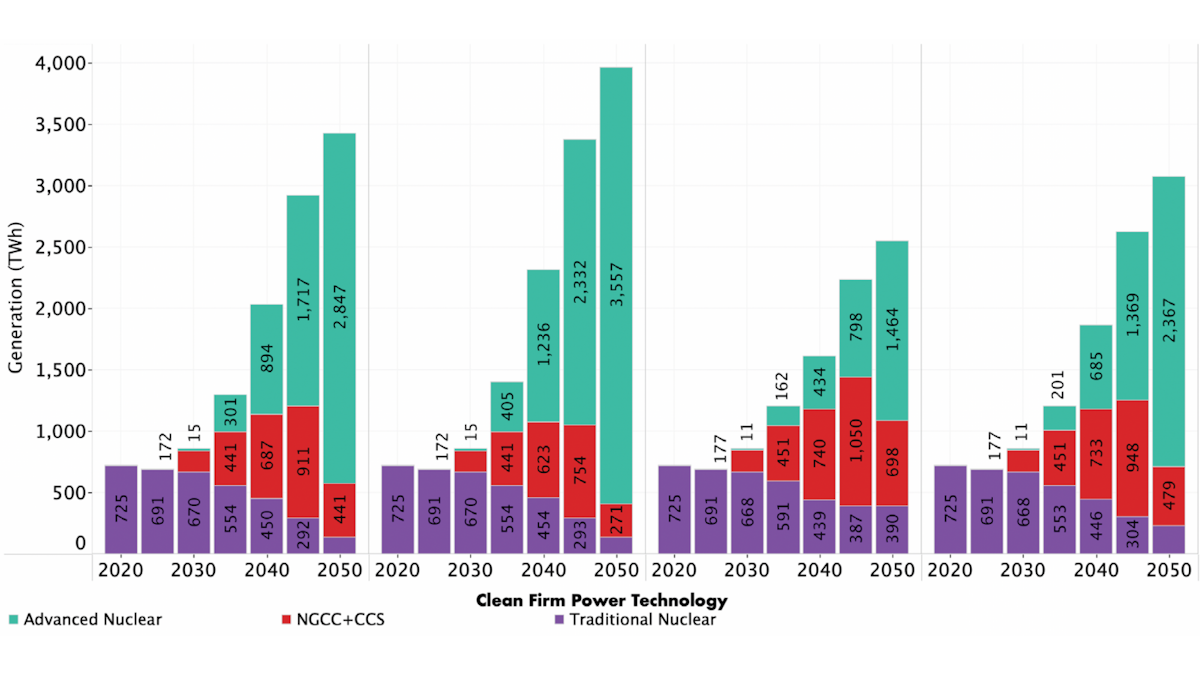

In general, advanced nuclear designs can ramp generation output at rates faster than traditional nuclear technology. ARTES technologies possess the particularly attractive ability to store energy in thermal energy storage systems and increase power output later, allowing for effective load and price following while maintaining very high reactor capacity factors. The flexibility of advanced nuclear manifests in sharp ramping to meet peaks and valleys in generation from low-cost, fuel-saving variable renewables. Figure 2-4 illustrates this ramping behavior within a net-zero electricity grid for all four scenarios during a simulated summer in 2050.

Example Summer Grid Dispatch in 2050

2.2 Advanced Nuclear Deployment

Advanced nuclear power plays a prominent role in achieving a net-zero electricity grid, with 185 to 469 GWe of advanced nuclear capacity providing around 20 percent to 48 percent of total electricity generation in 2050 (Table 2-1 and Table 2-2). Since this model features endogenous learning, advanced nuclear technology deployment and cost reductions go hand in hand. As the model independently elects to build advanced nuclear alongside other clean energy technologies as part of a least-cost energy system solution, nuclear technology overnight costs decline over time due to endogenous learning. Using accurate advanced nuclear operational characteristics and employing a bounding analysis of four different sets of initial overnight cost assumptions and learning rates, the WIS:dom-P model deploys a large amount of advanced nuclear capacity throughout the contiguous United States over the next three decades.

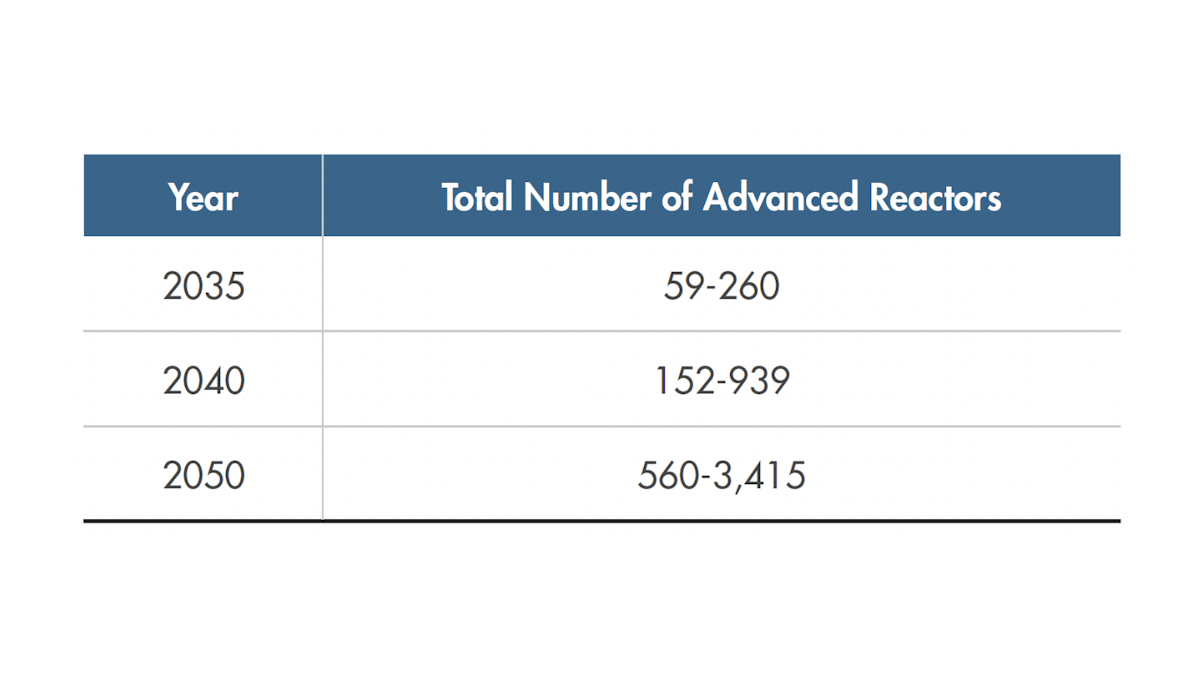

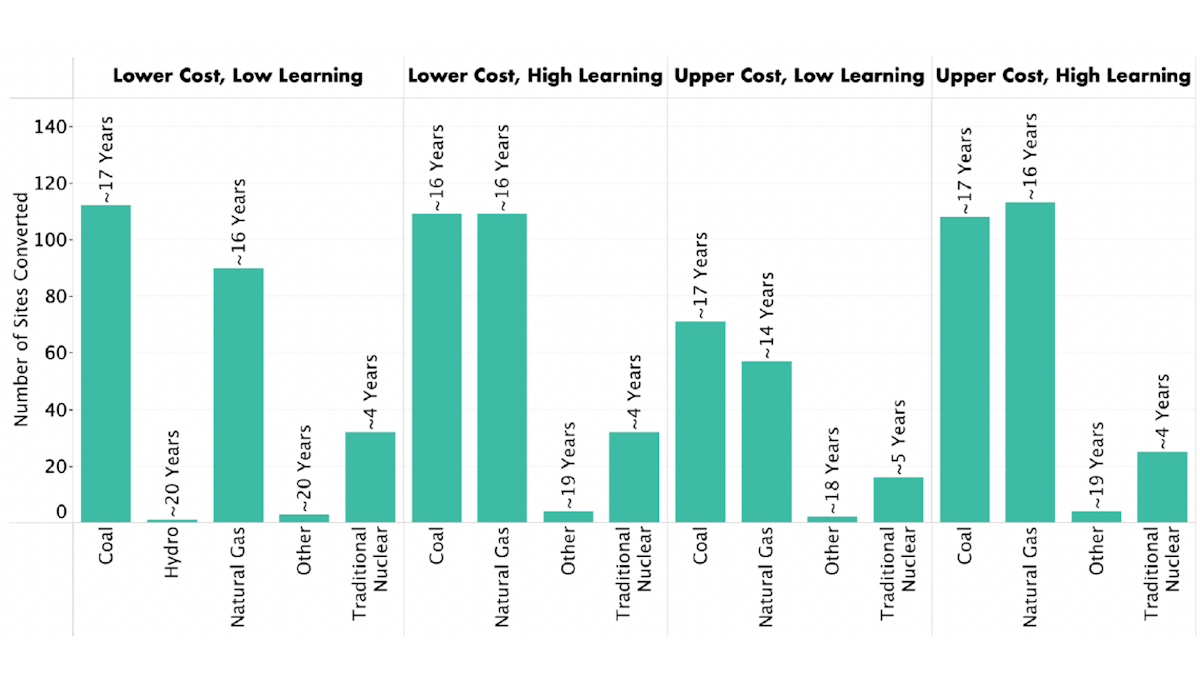

This result corresponds to the following number cumulative total of advanced nuclear reactor units across the three modeled technologies and reactor sizes, shown in Table 2-3.

Unsurprisingly, the highest values for capacity and generation occur under the Lower Cost, High Learning scenario in which advanced reactor designs are initially demonstrated at a more affordable cost and experience faster learning by doing, eventually driving substantial cost reductions over time.

Both traditional and advanced nuclear power compete against NGCC+CCS in the model in terms of capacity expansion and energy dispatch, yielding insights into capacity factors and levelized costs of energy for different clean firm power resources. The advanced nuclear power plants generally exhibit high capacity factors of >80 percent nationwide, indicating high utilization and good market competitiveness. Figure 2-5 shows temporal trends in total electricity generation and average capacity factor for different clean firm technologies that see significant deployment in the capacity expansion model.

Temporal Generation for Clean Firm Power Across Scenarios

A notable conclusion from this study is that as the model approaches 2050, it utilizes NGCC+CCS less, primarily leveraging fossil gas generation with CCS for ancillary firming purposes as opposed to large-scale energy generation. In contrast, nuclear energy generation is generally used at a high capacity factor, outcompeting NGCC+CCS in the modeled electricity market.

Deployment and overnight cost reductions due to learning

Over the next 30 years, advanced nuclear overnight cost (OC) reductions from endogenous learning encourage further deployment and drive continued cost declines in the WIS:dom-P model. This virtuous cycle can be expressed as a function of the number of deployed reactors, as this study’s endogenous learning is calculated using cumulative capacity, normalized to technology-specific template reactor capacity sizes.

In particular, reactor capacity sizes are 1,000 MWe for traditional nuclear, 150 MWe for SMRs, 345 MWe for ARTES (with a capability to ramp up to 500 MWe for 5.6 hours at a time), and 80 MWe for HTGRs. The inclusion of thermal energy storage results in unique and more sophisticated modeling constraints and capabilities.

Traditional nuclear power does not experience endogenous learning in this study. Instead, in the two Lower Cost scenarios, a static $4,783/kWe OC is assumed; and in the two Upper Cost scenarios, we adopt the NREL moderate ATB cost projections. More information is available in the Appendices.

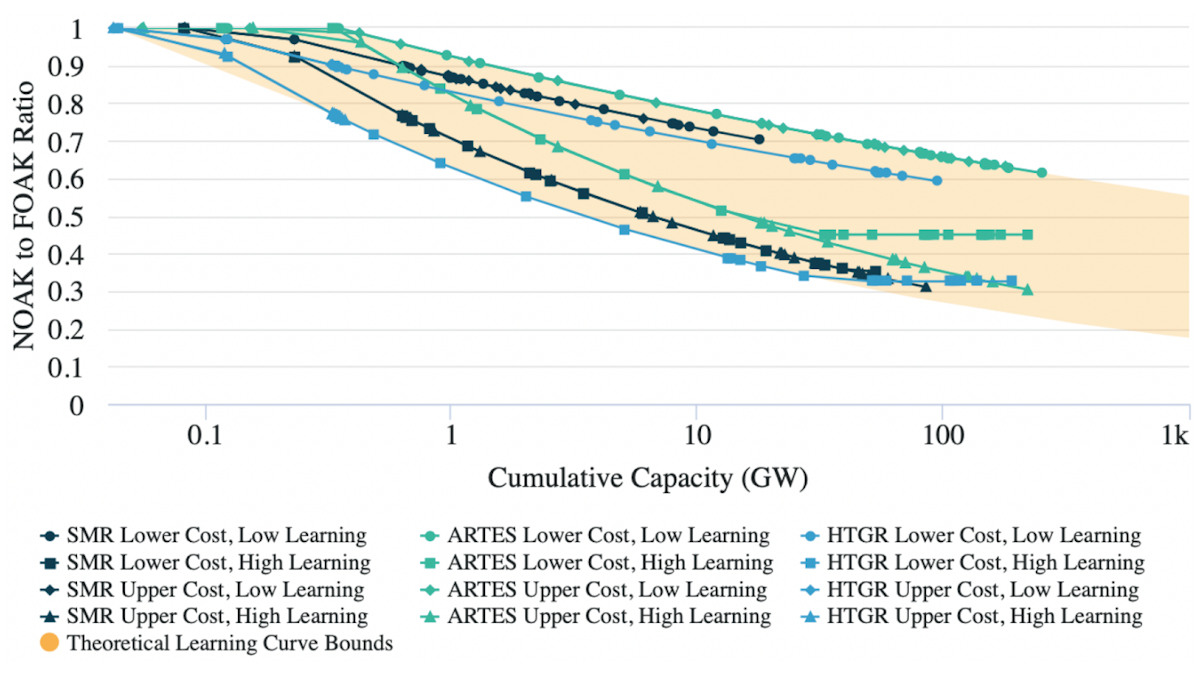

This study ultimately produces significant advanced nuclear deployment, driving substantial OC cost reductions. Assessing these OC reductions as a ratio of nth-of-a-kind (NOAK) to FOAK capital costs contributes valuable insights into how far advanced nuclear progresses down the learning curve in the simulations. Figure 2-6 illustrates this learning curve progress for the three modeled advanced nuclear technologies across the four FOAK and learning rate scenarios.

Advanced Nuclear Overnight Cost NOAK to FOAK Ratio Learning Curve Progress Across Scenarios

Figure 2-6 follows a classical learning curve where cost improvements continue with growing cumulative capacity deployment. However, an important feature of advanced nuclear technologies—and, in particular, those that employ standardized and modular manufacture—is that learning is better described as a function of reactor deployment, thereby benefiting technologies that can be sited more flexibly. The WIS:dom-P model used in this study attempts to deploy capacity in discrete increments as reactors, but also maintains the capability to flexibly site capacity deployment at a county-wide scale in increments that differ from reactor sizes.

Here, cumulative capacity deployment (GWe) and overnight cost ($/kWe) data in Figure 2-6 are exponentially interpolated to annual data from five-year cumulative data, where the incremental increase in each five-year period is annualized in years one through five. Exponential interpolation is used in favor of linear interpolation because this method is in line with the modeled five-year period cumulative capacity deployment data. Details on the exponential interpolation methods used for incremental annualized data are briefly discussed in the methods section in Appendix B.

2.3 Limitations

Ultimately, not even sophisticated national energy system models are capable of confidently predicting the clean energy future with certainty. As is the case for any study of this scale, the results described throughout this report are sensitive to numerous factors, from the range of assumptions considered to the technical and design constraints of the selected modeling approach. A number of the more important limitations are discussed in this section.

This report is confined to the continental United States and therefore does not account for advanced nuclear deployment that could benefit overall learning rates due to projects built in Alaska, Hawai’i, the US Territories, or internationally via nuclear export projects. This analysis also only considers advanced nuclear deployment in support of the US electricity sector and therefore does not directly account for nuclear deployment in service of non-electric markets, such as the market for high-heat applications. Advanced nuclear projects that help meet industrial process heat demand might, for example, accelerate the deployment of HTGRs beyond those deployed for the power sector alone.

This modeling study also does not address some market factors that could influence the competitiveness of advanced nuclear designs with one another and with other energy sources. In reality, one class of reactors may achieve a low FOAK cost while another category is built at a high FOAK cost. Additionally, advanced nuclear technologies are likely to undergo learning at different rates. Various market factors will determine the relative competitiveness of different technologies, from the availability of high-assay low-enriched uranium (HALEU) fuel for initial projects to the varying success of vendors in securing business deals and pre-orders, to the efficiency with which upstream manufacturing capabilities are established, and more.

These findings are likely sensitive to such considerations, but fully exploring this solution space would have required an order of magnitude higher number of scenarios. In addition, assigning high or low FOAK costs to different technologies effectively picks winners and losers at the model parameterization stage. Given such considerations, this study aims to provide a bounding analysis that can constrain the high and low range of future costs and deployment of advanced nuclear reactors as a group, based on a high-resolution capacity expansion model.

New future non-nuclear clean technologies may also emerge, changing the trajectory of the domestic clean energy buildout. For instance, enhanced geothermal energy could also see more widespread commercialization this decade, an outcome the WIS:dom-P model has not accounted for in the set of scenarios. The costs of offshore wind deployments might fall more rapidly than anticipated at the same time that offshore wind capabilities increase. Alternatively, new forms of cheap or long-duration energy storage could enable even wider deployment of wind, solar, and storage capacity beyond anticipated levels.

The future of the US energy system is complex and continually changing. There is no guarantee that advanced nuclear power will grow to the extent envisioned in these models. These results highlight how advanced reactors, when modeled realistically, have the potential to make a major contribution toward national energy production and progress in climate change mitigation.

Required Investment, Strategic Thinking About Early Deployment, and Versatile Applications

3. Capital Investment for Early Advanced Nuclear Deployment

In the previous chapter, the results highlight how advanced nuclear power can grow to become a large component of the future energy system in the United States even under pessimistic cost and learning assumptions. However, this outcome assumes sufficient availability of capital. The magnitude of capital investment implied by the deployment timeline across these model scenarios demonstrates the scale of future investment needed for a successful advanced nuclear sector. In today’s world, the complex processes of technology development and product commercialization are inextricably intertwined with government policy and market interactions.

3.1 Capital Investment

Capital formation is the process of acquiring the necessary pool of capital for an investment or project. That capital can be in the form of financed debt or equity. Capital costs are generally expressed as overnight costs (OC). Nuclear construction projects occur over multiple years, with capital expenditure required both before and throughout the construction process. This modeling study produced estimates of capital expenditure for advanced nuclear projects over the next 30 years across four scenarios. In Figure 3-1, we show capital costs annualized over an assumed three-year construction period, which is consistent with stated NOAK construction timelines for most advanced reactor developers.

Capital must be available to enable initial advanced reactor projects and develop the necessary supply chain. Critically, early investment in advanced nuclear energy drives early learning and catalyzes the development of supporting services like manufacturing, construction, fuel supply, and more. Early planning for and incorporation of firm, clean, dispatchable generating capacity like nuclear can reduce total system-wide power sector costs for decarbonization scenarios, relative to inefficient retroactive deployment in response to emerging system needs.

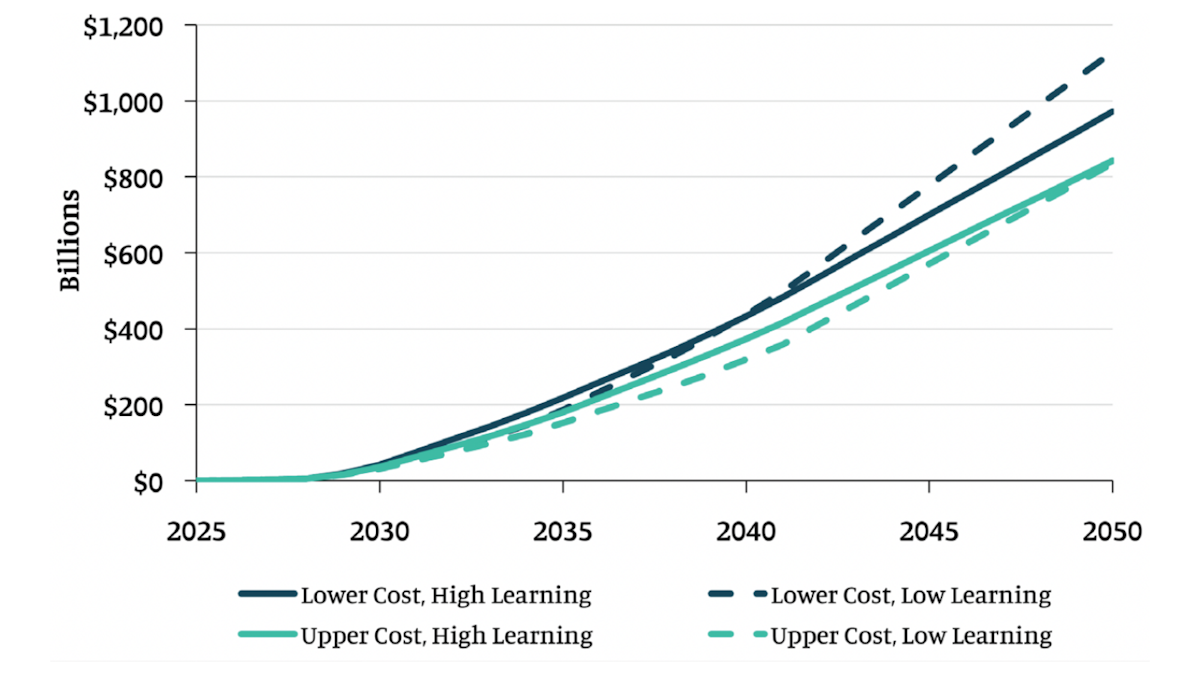

Realizing the potential of advanced nuclear energy to help power the United States energy transition could require cumulative capital formation for power plant construction on the order of $150 to $220 billion investment by 2035, growing to a total of $830 billion to $1.1 trillion by 2050. For context, the same range of capital investment is required to deploy utility-scale solar and onshore wind across the model scenarios.

Cumulative Annualized Capital

The following sections discuss various factors that will likely differentiate the financing and construction of advanced nuclear power plants from previous generations of traditional nuclear reactors. These considerations will ultimately determine the degree to which advanced nuclear designs are able to achieve cost improvements and more easily secure capital investment and financing.

3.2 Deployment and Capital Availability

To achieve cost reductions in key areas for advanced nuclear power, the industry will need to successfully develop a factory-scale construction program. Smaller reactors forgo some cost reductions achieved with the economies of scale provided by conventional large reactors. Instead of pursuing economies of scale, modular designs can achieve potentially significant cost reductions through the production of multiple reactors of a standardized design.

Achieving the scale of mass production necessary to unlock major cost improvements will not be possible if just a single demonstration project is completed and operated for years before subsequently scaling up deployment. An unsuccessful demonstration program or delays in the first wave of advanced nuclear demonstrations and subsequent early-stage projects will impede cost reduction from technological learning and restrict the potential for advanced nuclear to help meet US climate goals.

Given the importance of sufficient capital availability for early reactor builds, capital formation in both the public and private sectors is a necessary condition to achieve sustainable, cost-effective advanced nuclear energy deployment. However, under-investment in technology development and commercialization is typical, especially when large capital investments are required. The consequence is that new technology is often under-deployed. This is particularly true for innovations linked to the “public good”, such as addressing climate change, which is not fully valued in the market, making it difficult for private firms to capture sufficient benefits to make deployment financially attractive.

Cost reductions achieved through sufficient early investment and deployment of advanced nuclear power reduce the overall investment required (Figure 3-2). This results in a greater market opportunity by making the technology cost-effective enough to compete without the need to consider the unpriced public benefits.

The clean firm power landscape is likely to be competitive starting in the near future. Other emerging clean firm power technologies such as NGCC+CCS, advanced geothermal, or run-of-river hydropower, may be able to fill the need for clean firm power on a decarbonizing grid, potentially competing with advanced nuclear reactors in some applications and contexts. Dispatchable utility-scale or distributed energy storage can also increase grid flexibility. However, each of these technologies has its own drawbacks, as does advanced nuclear. For example, this study assumes an optimistic CCS capability of 95 percent, which may be lower in practice. Enhanced geothermal increases the geographic options for siting geothermal power, but siting potential for enhanced geothermal systems remains somewhat restricted. Similar considerations apply to run-of-river hydropower, which is subject to even more limited siting constraints. High reliance on grid-scale storage to help match the daily generation profile to demand may substantially increase system costs. It is also assumed that there are no restrictions on HALEU fuel production, an assumption that will require active federal policy efforts to realize.

More broadly, increasing the available portfolio of clean firm power sources and encouraging competition among technologies will be important for decarbonizing not only the power sector but also the rest of the economy. Advanced nuclear, for instance, may play an important role in unlocking low-carbon solutions in other economic sectors, such as powering industrial processes and supplying residential and commercial heat (see Section 5).

3.3 Financing

Financing is expected to be easier for advanced reactors than for large conventional reactors because of their lower absolute cost, reduced construction timelines, and lower construction risks due to factory production. Although initial financing conditions (e.g., the cost of capital) are expected to be higher for the first advanced reactor unit, successful construction and operation of initial builds will likely improve conditions for financing subsequent projects. Such staged increases in capacity should reduce the financial risk associated with long-lead-time, capital-intensive projects.

Project structure and management could also help reduce capital costs per kWe for advanced nuclear. In traditional nuclear construction projects, the “stacking” or “pancaking” of contract contingencies and profit margins across a fragmented supply chain has escalated project costs over time. The increase in average capital costs per MWh for conventional light-water reactors in the last decade is mostly due to vendor/supplier agreements and risk management (increasing the cost by 70 percent), rising commodity prices (adding another 25 percent), and growing owners’ costs (about 17.5 percent). Together, these factors more than doubled the costs of traditional nuclear reactors between 2004 and 2011.

In contrast, advanced reactors are expected to rely on a more integrated supply chain and fewer subcontractors organized in fewer layers. Such improved organizational and management efficiencies have the potential to reduce the multiplication and stacking of contingencies.

3.4 Discount Rate

The discount rate is the opportunity cost of capital (as a percentage of the value of the capital). The opportunity cost of capital is the return on investments forgone elsewhere by committing capital to the investment under consideration. Higher discount rates negatively impact capital-intensive projects by increasing overall project cost and levelized cost of electricity (LCOE). Large nuclear energy projects have historically had higher discount rates compared to other technologies. Conventional nuclear power has been considered a higher investment risk than other conventional technology due, in large part, to past delays and cost overruns for nuclear projects. This additional risk is reflected in higher discount rates. Reductions in the discount rate are usually expected after multiple projects meet the expected cost and construction timeline, demonstrating their future potential for success.

Municipal or government-backed projects generally have a lower discount rate than investor-owned projects, reducing the overall project cost. Municipal projects usually have a higher credit rating than investor-owned entities, allowing them to secure lower interest rates. Further, they do not pay taxes or have to consider the return on equity.

Advanced reactor projects reduce investment risk compared to that of conventional reactors. Sequenced construction exposes less capital to loss due to cancellation at any given point in the project. Sequenced reactor projects are completed more quickly, enabling faster learning and reducing project risk. Multiple reactor developers are following an iterative innovation approach that reduces design and manufacturing risk before a full-scale design is available. Some developers plan to own and operate the reactors and sell the electricity directly on a contract.

3.5 Project Planning

Project design can significantly affect many investment parameters. Recent nuclear projects have experienced cost overruns during the construction phase, caused in part by project management inefficiencies. Nuclear energy projects are not alone, however; many large projects experience delays. , Moving to a standardized factory construction model with smaller units shifts project design to a smaller project paradigm, avoiding many of the challenges with larger projects.

Multiple Reactor Sites

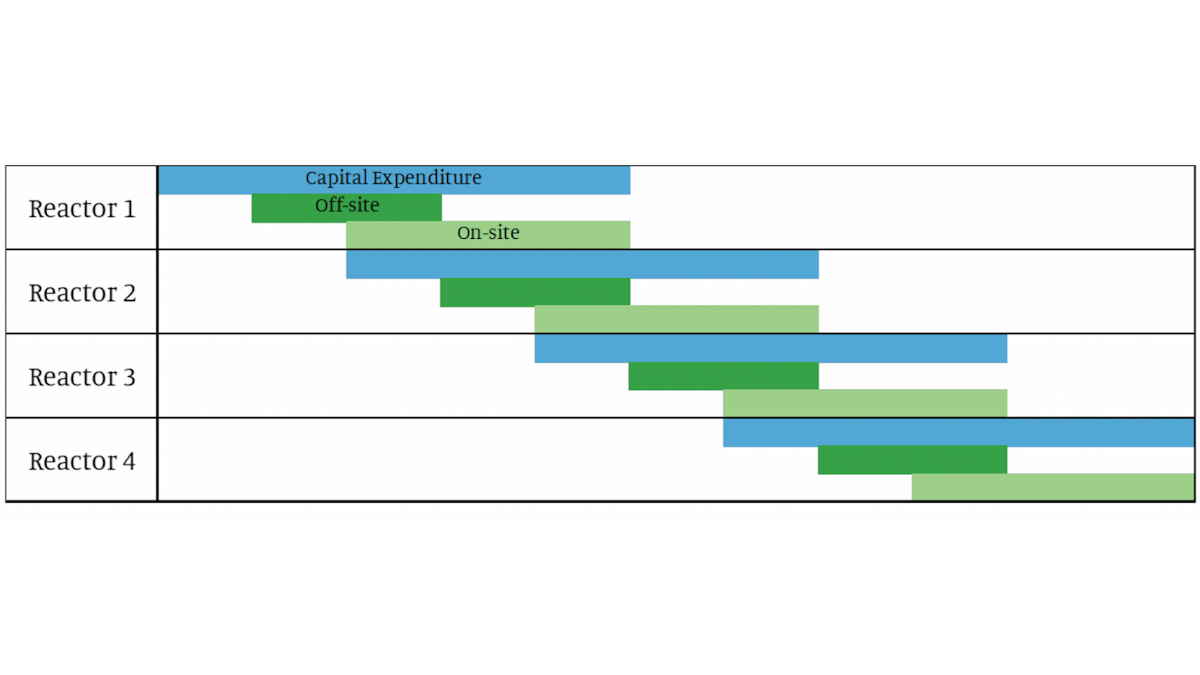

Lower capital costs per reactor can be more readily financed. Sequenced construction also allows for a more distributed pattern of capital expenditure (Figure 3-3). This facilitates the capital formation and potentially enables access to capital at a lower discount rate for smaller utilities or customers with less capital on hand or limited ability to carry debt.

A more sequenced approach to construction can use construction resources more efficiently. The total site workforce can be reduced, moving from one reactor to the next as tasks are completed. Projects will also require a reduced pool of construction assets and equipment. If delays occur in the process of building one reactor unit, construction can begin or continue on the next module. This strategy presents numerous advantages over building a single large light-water project, in which a construction issue would force a larger group of workers to delay work until the issue is resolved.

Multiple reactors at a site allow for additional cost savings from shared infrastructure, such as transmission, operations, facilities, and workforce. This advantage is well understood with existing large conventional power plants, and multi-reactor sites have remained more economical than single-unit sites.

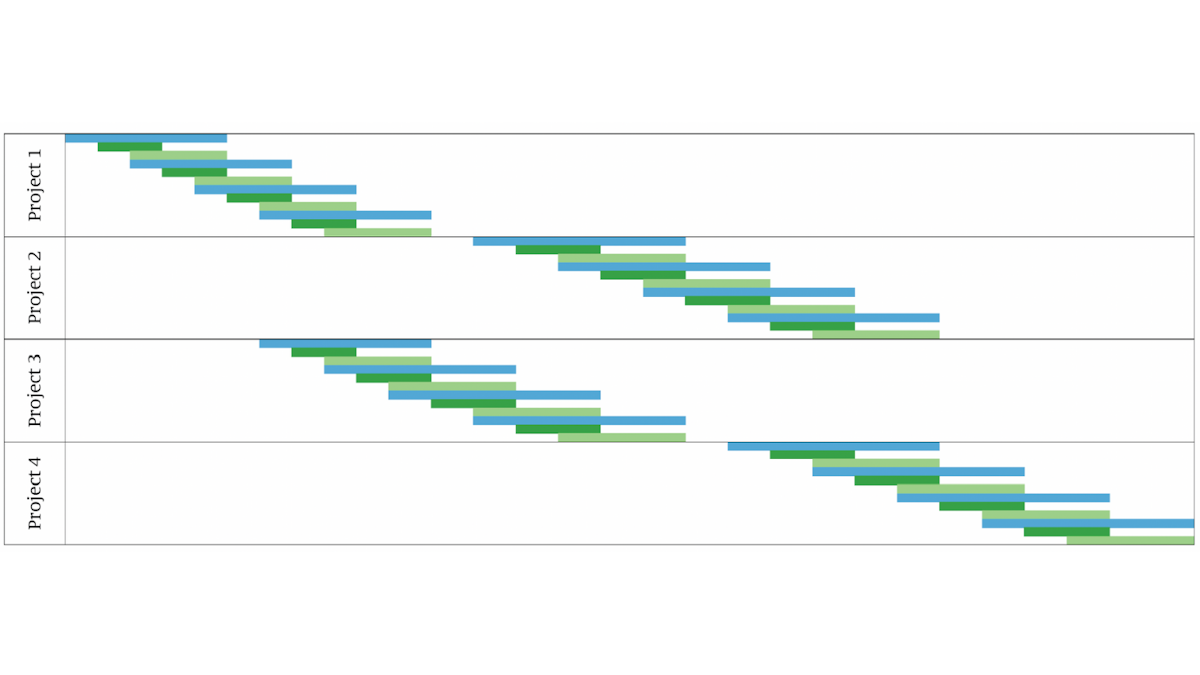

Another important consideration for the advanced nuclear sector will be the appropriate scaling of upstream factory manufacturing capacity. Factories can operate more efficiently and cost-effectively when optimally designed to meet the needed level of demand from the industry at large. While a sequenced reactor construction approach can reduce project-level risk, parallel projects reduce the risk of lag or downtime (Figure 3-4).

Orders for long-lead projects or limited manufacturing capacity are typically made far in advance, creating a queue or backlog. Backlogs are common in industries that specialize in large and complex products. The commercial aircraft industry provides several parallels to small modular reactor manufacture. Airliners are very complex, expensive, and safety-critical products that are constructed and assembled in a factory. Orders are commonly placed years in advance, and manufacturers carry a backlog of several thousand units.

A backlog of orders is useful to define the scope and initial priorities for manufacturing capacity, while also allowing for pre-planning of efficient manufacturing capacity expansion in the future. The backlog also provides a buffer to maintain steady production 一 even if order volume periodically drops. Sustainable backlogs are a positive indicator to investors. However, excessive backlogs signal the need to expand capacity to meet customer demand and maintain customer confidence that the order will be filled.

Early demand and orders for reactors will send a strong demand signal to prospective suppliers. A backlog of orders for reactors will provide justification for significant investment by companies that supply fuel and component manufacturing capabilities.

3.6 Economic Metrics

This study evaluates the costs of various energy technologies as a function of either deployment-driven capital cost improvements or projected capital cost curves, along with the costs of providing energy generation to meet grid dispatch requirements. The capital, fixed, and variable costs can be assessed together as the levelized cost required to produce a unit of electricity. Importantly, levelized costs decline both from capital cost reductions and capacity factor rates. Two levelized cost metrics are used to highlight how different clean firm power technologies provide value to the grid and how costs are expected to evolve over time.

Overnight costs

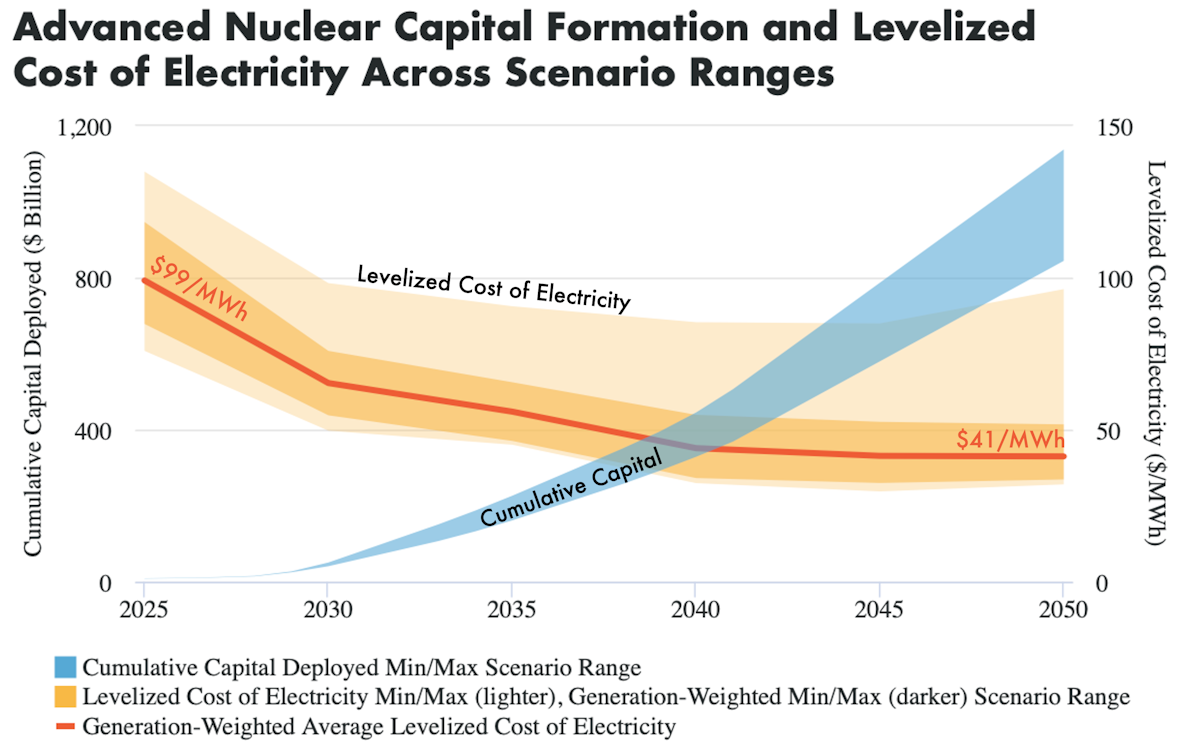

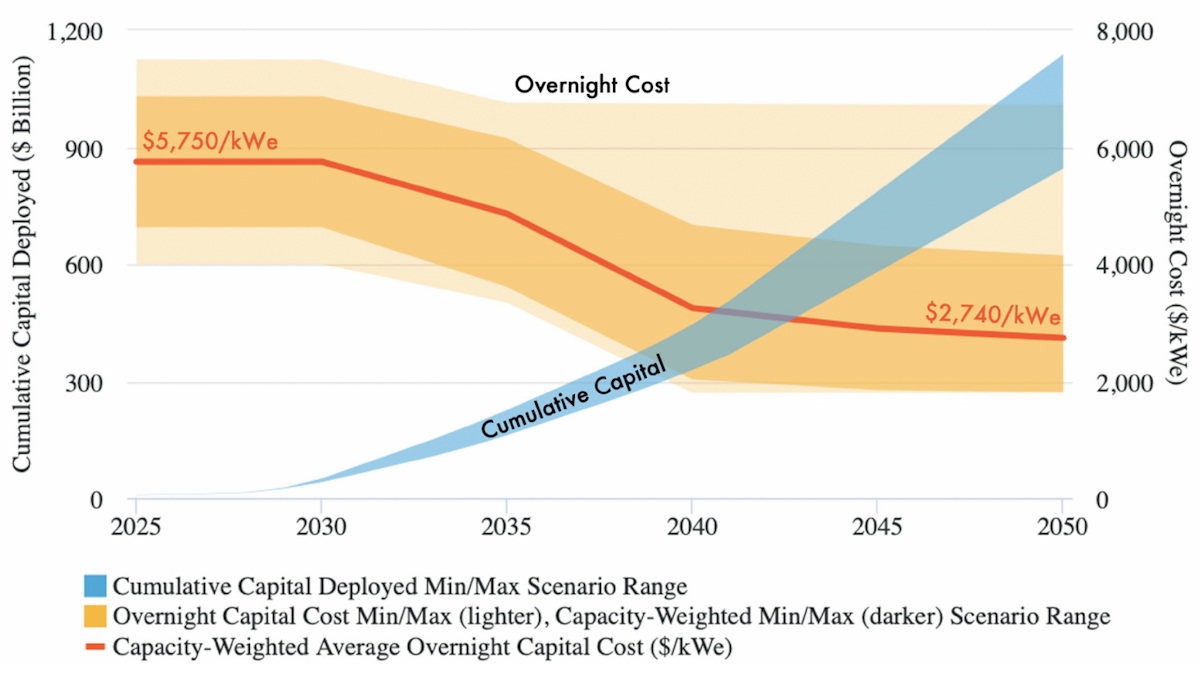

Reductions in OC from learning-by-doing can only be achieved if sufficient capital is mobilized and is done so in a timely fashion. Figure 3-5 shows the cumulative invested capital, translated from the modeled advanced nuclear deployment rates, needed to facilitate OC reductions and achieve a net-zero power sector by 2050. Importantly, the plotted capital formation considers capital deployment only for project builds. Supporting and ancillary advanced nuclear service industries, such as HALEU fuel production, require capital deployment well before power plant project capital mobilization. Capital formation needs to begin today, growing to around $30 to $40 billion of cumulative deployed capital by 2030 and $150 to $220 billion by 2035 in order to drive sufficient commercialization of advanced reactors to achieve necessary cost improvements. These investments are crucial for positioning the advanced nuclear sector to accelerate the rate of capital cost declines in the late 2030s.

Advanced Nuclear Capital Formation and Overnight Cost Across Scenario Ranges

Levelized cost of electricity

OC learning manifests in substantial reductions in the LCOE for advanced nuclear power. Similar to Figure 3-5, Figure 3-6 plots improvements in the LCOE for advanced nuclear energy versus capital formation. The difference is that in Figure 3-6, LCOE (a generation-based metric) is plotted instead of OC (capacity-based), and as such, all weighted averages are weighted using generation instead of capacity.

Advanced Nuclear Capital Formation and Levelized Cost of Electricity Across Scenario Ranges

With advanced nuclear becoming a major component of the modeled US power grid by 2050, the cost of advanced nuclear power strongly influences the overall retail cost of electricity. The two Lower FOAK Cost model scenarios yield overall national average retail electricity prices of $59/MWh to $65/MWh in 2050, while the two scenarios with Upper FOAK Cost result in retail electricity rates of $76/MWh to $81/MWh.

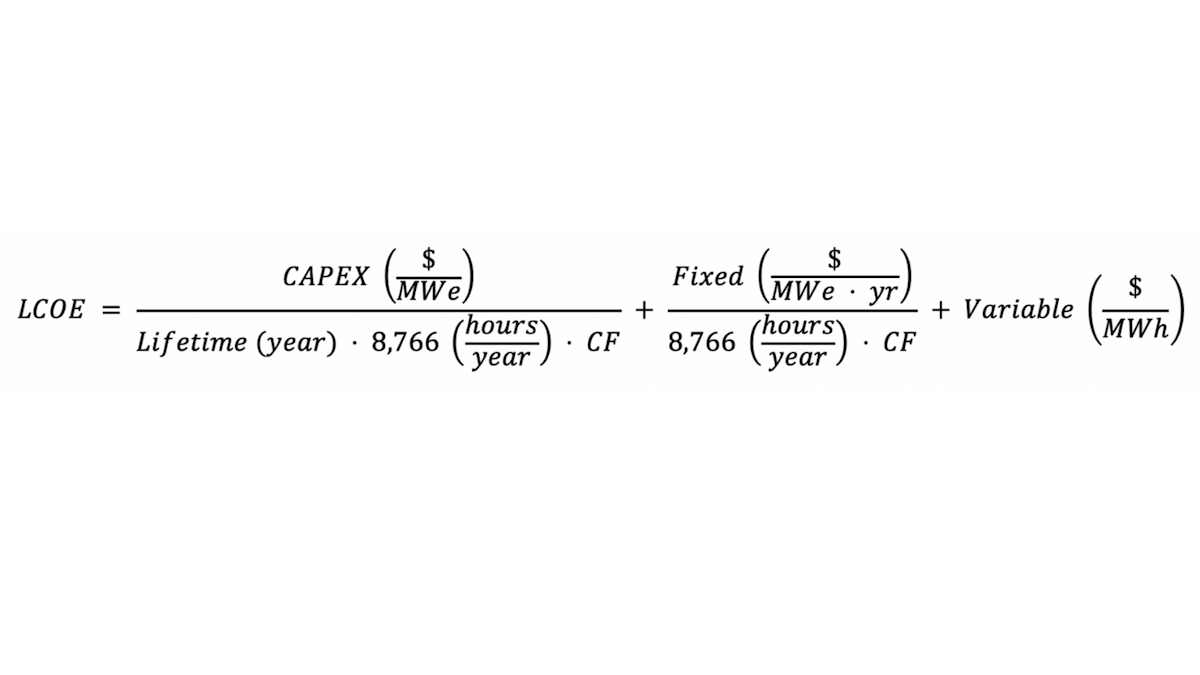

While LCOE is an important metric for ascertaining the total cost of generation, it is by its nature significantly influenced by the average technology capacity factor. In particular, LCOE is composed of three cost components: capital costs ($/kWe), fixed annual costs ($/kWe•yr), and variable costs ($/MWh). Variable costs can be further broken down into fuel costs ($/MWh) and variable operations and maintenance costs ($/MWh). Equation 1-1 expresses the formulation for LCOE, segmented by levelized capital, fixed annual, and variable costs. Importantly, the average capacity factor is used to levelize capital and fixed costs.

Evidence of the impact of capacity factor on LCOE is readily visible in Figure 3-6, where some inflections and even increases in the maximum LCOE appear despite monotonic, long-term reductions in capital and fuel costs. These variations are primarily driven by capacity factor changes as the grid decarbonizes and the utilization rate of different generating technologies shifts. We probe this phenomenon further in Figure 3-7.

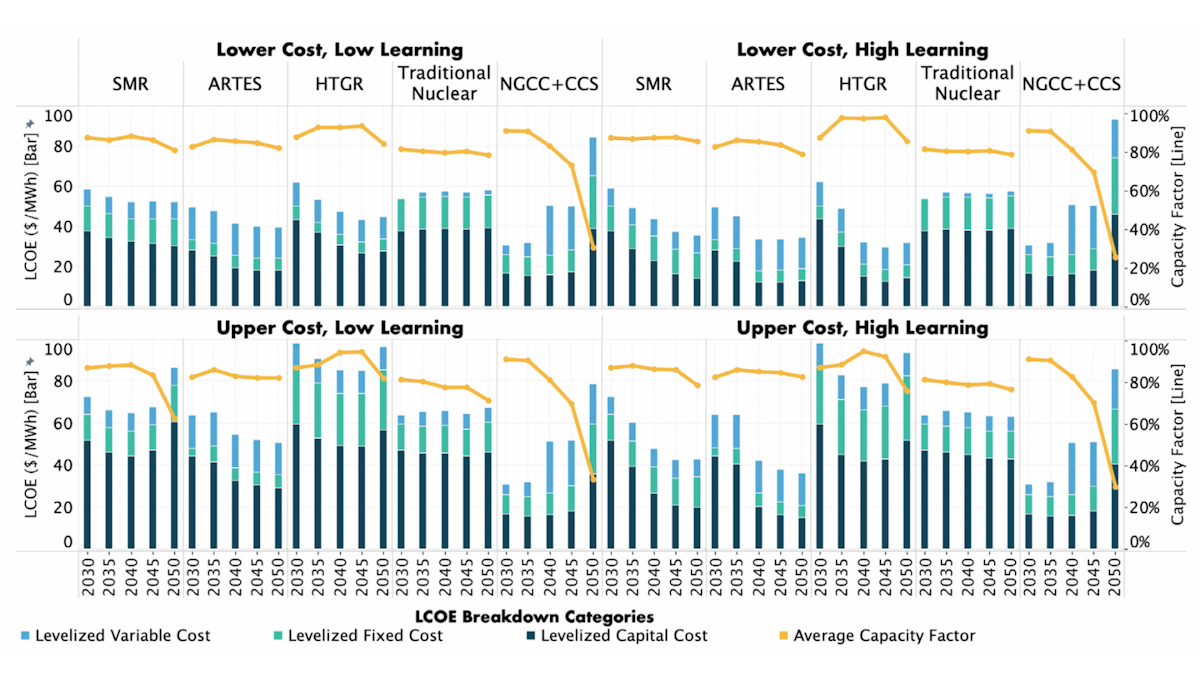

The key takeaways from Figure 3-7 are threefold. First, nuclear power LCOE is generally dominated by levelized capital costs, followed by levelized fixed and variable costs. And with the exception of ARTES reactors, levelized variable electricity costs represent a fairly minor contribution to LCOE for nuclear technologies. Second, advanced nuclear technologies typically achieve LCOE cost parity with NGCC+CCS by 2040. Third, the capacity factor substantially influences the LCOE. Despite OC reductions, levelized capital costs actually increase in certain situations as absolute OC learning begins to plateau and capacity factors dip. Importantly, the learning rate remains constant, but the successive OC reductions in absolute dollars decrease over time. The capacity factor of some clean firm technologies begins to decline in the late 2040s. This only marginally affects advanced nuclear technologies, but seriously impacts NGCC+CCS. Precipitous declines in average NGCC+CCS capacity factor between 2045 and 2050 due to economic pressures, result in sharp increases in levelized capital and fixed costs and a transition for these plants to a backup role for the grid. This is expected since, of the three constituent costs in the LCOE (Equation 1-1), the average capacity factor is only used to levelize capital and fixed annual costs, and these cost components are inversely proportional to generator utilization rates.

LCOE is only one instantiation of a levelized cost metric. For example, energy generation technologies can also be characterized using a capacity-based levelization method we call the levelized annual cost of capacity (LACC) [$/kWe•yr]. LACC reduces the influence of capacity factor on the levelized cost value because, unlike LCOE, its derivation includes capacity factor only to levelize variable costs.

In this way, a complete description of levelized costs for energy generation technologies should include both LCOE and LACC. And in particular, technologies with proportionally high variable costs are better characterized by LCOE because a low capacity factor does not significantly deflate overall LCOE. Similarly, energy technologies with proportionally high capital or fixed annual costs are better analyzed using LACC because a low capacity factor does not significantly diminish the contribution from capital and fixed annual costs. More details on the derivation of LACC and the application of LACC analysis to our modeled results are presented in Appendix D

4. Initial Target Markets and Customers

Over the past decade or more, researchers, policymakers, and industry have proposed a large number of potential contexts in which advanced nuclear reactors might be commercially deployed. , Such suggestions have often been speculative and warrant more careful evaluation to distinguish between viable opportunities for early deployment in the nearer term and applications that would face more substantial obstacles in terms of cost-competitiveness or other barriers.

In this section, a number of settings and contexts are theorized to offer strong market potential for future advanced microreactor or small reactor deployments and assess the advantages offered by nuclear energy production relative to competing options and to potential obstacles to deployment. Proposed initial target markets and customers are classified into two broad categories: early stage and intermediate stage. Early stage markets and customers are approximately those potentially best suited for FOAK to NOAK advanced nuclear projects during the very opening phase of technology commercialization. In contrast, intermediate stage markets and customers face additional cost, technical, regulatory, or readiness concerns that may make them better suited for a subsequent phase of deployment.

4.1 Early Stage

Existing Nuclear Sites

Suitability: Conventional and Small Reactors

Sites of existing or retiring nuclear power generation may provide favorable opportunities for initial advanced nuclear projects. A strong precedent in the United States exists for the construction of new nuclear units of a different design at existing nuclear power plants. Examples include the Peach Bottom Atomic Power Station in southeastern Pennsylvania, the Dresden Generating Station in northeastern Illinois, and the Alvin W. Vogtle Electric Generating Plant in northeastern Georgia. Existing nuclear power plants have already been proposed as candidate sites for the Advanced Reactor Demonstration Program (ARDP). Existing and retiring nuclear power plants make appealing locations for advanced reactor projects as they already meet regulatory criteria ranging from seismic stability to the siting of emergency planning zones. Furthermore, local stakeholder considerations may be facilitated by community comfort and familiarity with nuclear technology.

Replacement of Coal, Gas, and Oil-Fired Power Units

Suitability: Small Reactors

To-be-decommissioned and recently decommissioned coal-fired power plant sites and other fossil fuel generating stations represent desirable target locations for advanced reactors for several reasons. The repowering of coal and other fossil sites can help save early novel reactor deployment costs by allowing for some reuse of equipment and infrastructure. One recent academic study quantified potential savings of up to 15 percent on initial OC for an SMR sited at a decommissioned coal power plant, thanks to the ability to repurpose existing assets like cooling systems, switchyards, and grid connections. Existing road and rail connections may facilitate construction, while coal plant sites may also prove favorable for meeting regulatory siting guidelines. The Idaho National Laboratory has recently released an extensive report on the technical and economic considerations relevant to the repowering of coal-fired power plants with advanced reactors.

Repowering existing coal sites can generate continued local economic activity and employment, thereby appealing to local communities and stakeholders. The potential for retention of fossil plant workers, however, depends critically upon the time frames over which fossil plants are retired relative to the start of construction and operation of new onsite nuclear capacity. The potential scale, timing, and implications of repowering existing fossil-fired power stations nationwide with advanced nuclear reactors is discussed in Section 7.6.

Military Bases and Portable Military Applications

Suitability: Microreactors and Small Reactors

The US military could emerge as an early customer for micro- and small reactors. Two separate Department of Defense projects are already in progress. Operational considerations such as performance, reliability, security of fuel supply, and modularity can incentivize the pursuit of projects at a higher cost point than might be viable for many civil or private sector applications. Energy-dense, mobile, and reliable sources of power could also support the Department of Defense’s interest in the development and future deployment of laser and microwave weaponry with power levels ranging from 150 kWe to 1 MWe. However, any military requirements for special customization to meet specifications could complicate manufacturing and supply chain considerations.

Data Centers

Suitability: All Reactors

Electricity represents a major component of data center operating costs, and data centers also place a high value upon reliability and predictability of power supply. Some exploratory efforts are already underway to investigate connections for new data infrastructure with existing nuclear power plants. But as is the case for heavy industrial customers, data center operators are likely to prioritize electricity costs and risk reduction and may not be likely to emerge as early adopters of new advanced nuclear reactors. Given that the primary competitor in this end-use case is the price of conventional electricity, onsite nuclear could struggle to be considered for such applications.

At the same time, some large US-based technology companies such as Google and Microsoft have signaled strong interest in procuring 24/7 carbon-free electricity to power their business operations and activities as part of long-term corporate climate commitments, even if such clean electricity comes at a premium cost. As such, these and similar voluntary commitments by tech companies could potentially drive greater adoption of advanced nuclear technologies for data center applications than would otherwise occur due to cost factors alone. A preliminary agreement by advanced reactor developer Oklo to partner with a cryptocurrency firm suggests the possibility for earlier adoption in some applications.

Remote Communities

Suitability: Microreactors and Small Reactors

Many remote and island communities rely on fossil energy generation and imported fuels, facing both high energy costs and vulnerability to supply shortages. Most remote communities have power requirements of 5 MWe or less and are thus promising candidates for microreactor-sized projects, while small reactors may prove well suited for replacing fossil generation in larger towns or small cities in remote regions. Microreactors may be able to achieve cost-competitiveness with diesel power generation in remote communities even from the very outset of early deployment. , Island communities often exhibit a similar reliance on fossil generation and fuel imports, but enjoy access to maritime shipping and thus confront lower costs and risks of supply disruption. At the same time, land scarcity and the value of potential desalination via the co-generation of heat strengthen the value proposition for nuclear power over other generation technologies.

Direct Contracts

Suitability: Microreactors and Small Reactors

Direct sourced contracts and power purchase agreements are used to purchase electricity from a single supplier. These contracts are common in industrial and commercial applications where the buyer desires to reduce market cost volatility and ensure supply. Increasingly, companies are also using these contracts to directly purchase electricity specifically to meet internal goals of consuming only clean energy. Early efforts have primarily focused on solar and wind renewable energy credits. However, these sources do not generate electricity that is directly matched to consumption. Clean firm energy sources, like nuclear energy or geothermal, will be required to meet hour-matched consumption.

4.2 Intermediate stage

Off-Grid Extractive Industrial Sites

Suitability: Microreactors and Small Reactors

Remote industrial sites such as mines, logging operations, oil and gas operations, and water and wastewater facilities often face similar high energy costs and supply challenges as those of remote communities. Such customers are gaining focus as a potential area for early adoption of new nuclear technologies. For instance, the mining sector has expressed interest in the use of small reactors to decarbonize diesel generators currently used to power on-site mining equipment. Remote industrial applications would also particularly favor mobile or transportable reactor designs that could be relocated to new sites. However, industrial customers are likely to be both highly cost-conscious and risk-sensitive. Many of these industries already face considerable operational uncertainties and tight profit margins. As such, extractive sectors are likely to wait to observe the results of initial deployment efforts elsewhere before committing to adoption.

Industrial Heat, Power, and Co-Generation

Suitability: All Reactors

The heavy industrial and manufacturing sectors remain major consumers of electricity as well as fossil energy for industrial heat. For many sectors including but not limited to steel, aluminum, computer chip manufacturing, shipbuilding, and petrochemicals, energy costs represent a sizable fraction of overall costs. Particularly as some industrial commodities like steel and aluminum face the prospect of carbon border taxes that may impose trade tariffs on carbon-intensive products, major industries are increasingly prioritizing innovative ways to reduce carbon intensity. Small reactors are often proposed as an appealing solution to meet clean energy requirements for many industrial activities. Co-production of heat can also serve a versatile array of industrial applications including hydrogen and ammonia production. Yet despite the potential value of nuclear energy for industrial customers, cost considerations and uncertainty regarding unproven technology are likely to dissuade industrial customers from early adoption. Pilot programs with public sector support, such as a recent $10 million US Department of Energy award to Xcel Energy to explore nuclear hydrogen production, could accelerate the pace of adoption.

Transportable Designs

Suitability: Microreactors and Small Reactors.

In addition to the military and off-site industrial applications mentioned above, some have suggested that mobile advanced reactor designs could also provide long-term power to small communities or could be designed for rapid-response deployment during emergencies or natural disasters. However, the commercialization of mobile, transportable reactors will critically depend on the development of new regulations to govern this category of nuclear technology—an unpredictable process that may take many years. This factor complicates any potential for the near-term commercialization of transportable reactors intended for highly flexible siting and operation.